SPIVA: about 85% of active fund managers underperformed their benchmark indices in a 10 year period.

In what other field can an amateur with no education or training outperform 85% of professionals with fine titles and high salaries?

This is the biggest joke in modern society.

In fact, since essentially all of these companies are spending all of their operating cash flows on capex spending, they are simultaneously having to issue debt to raise capital.

Again however, you won’t see MSFT on this list.

Hyperscalers have issued $350B in debt since 2025 to fund AI capex, while Microsoft has issued none.

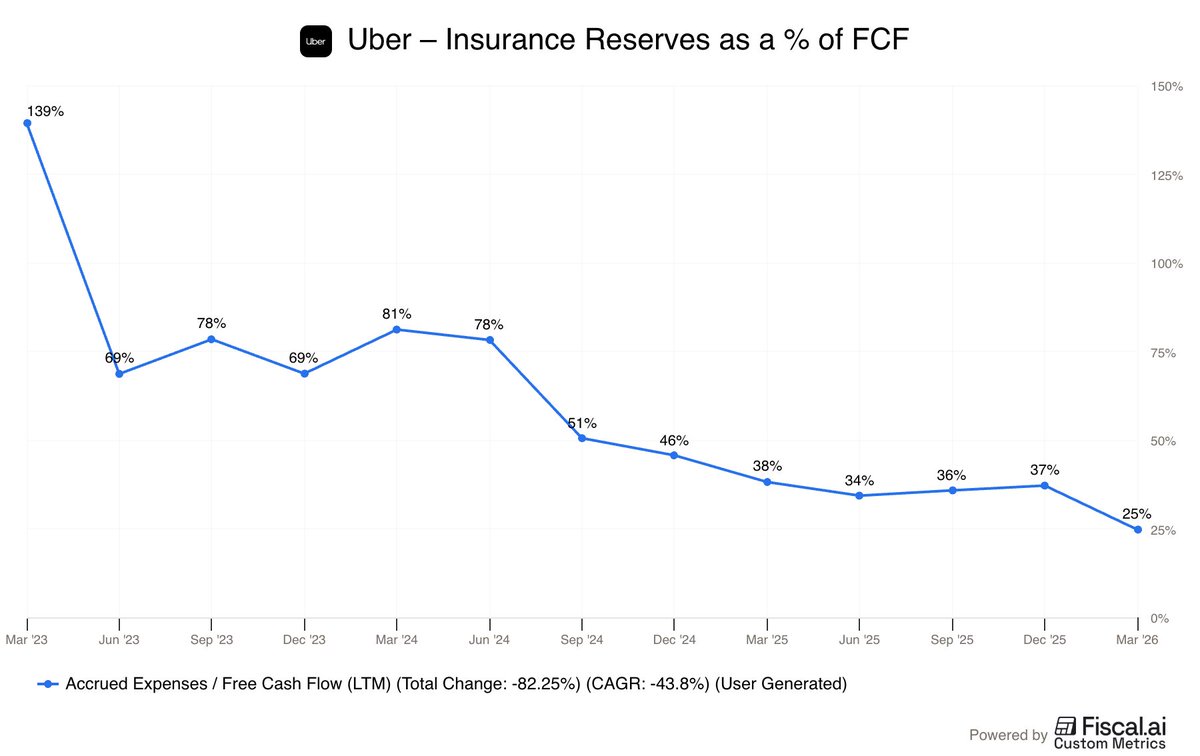

A common complaint against $UBER over the last few years is that "their FCF is fake" or otherwise overstated

This is due to $UBER's insurance reserves which is cash they DO earn interest on, but can't use towards day to day operations -- putting it in this weird limbo

That said, accrued expenses (majority insurance reserves) as a % of FCF have continuously ticked down over the last few years and now only make up 25% of FCF

Ethan - Respectfully, you are entirely wrong in your conclusions. Uber is investing more than any other company to advance the progress of AVs globally (see: https://t.co/UkJZfGBOpy)

We are responding to misguided legislation that had NO path of succeeding and would have resulted in NO AVs. In NJ, the bill under consideration before Uber's advocacy would have banned BOTH Tesla and Zoox. In DC, it would have banned hybrid networks ENTIRELY.

There's always more to these issues than a punchline, and we know it takes a lot to meet cities in the middle, responsibly.

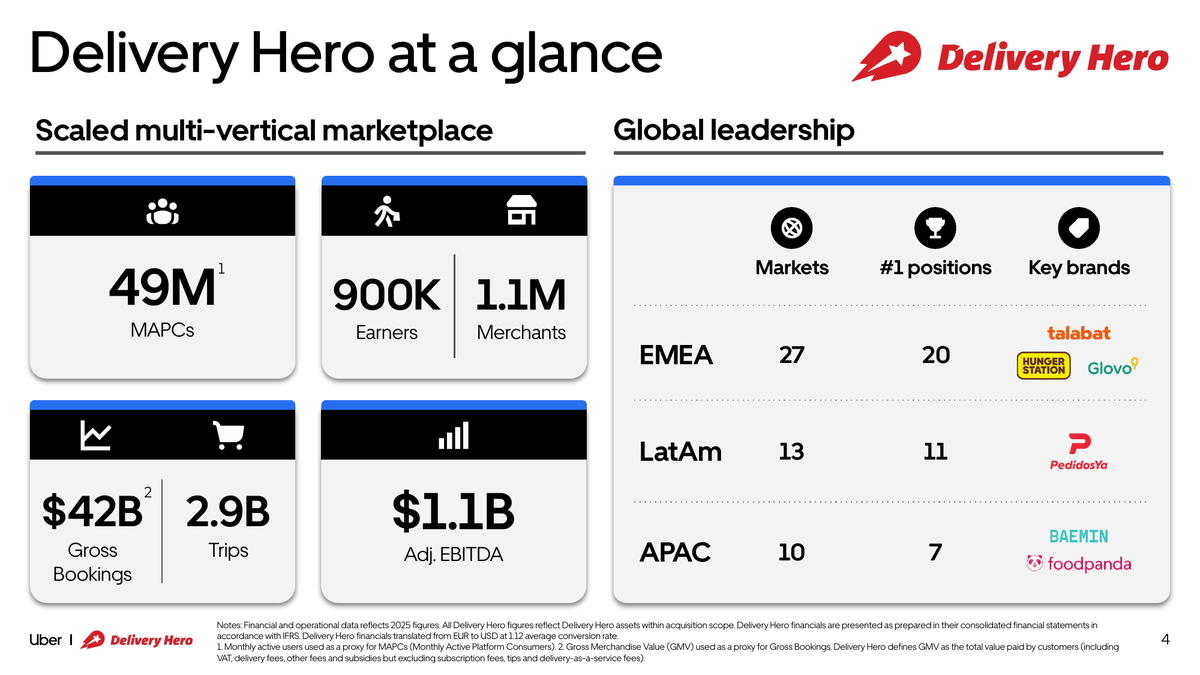

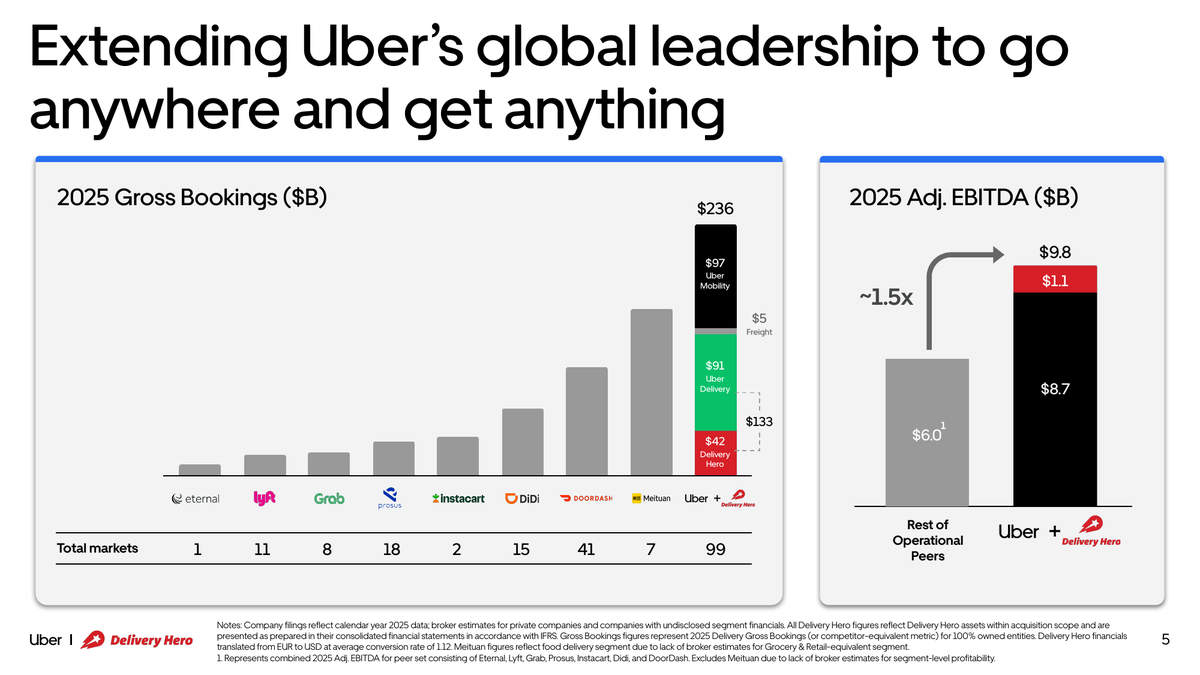

Our offer to acquire Delivery Hero exceeds the very high bar we set for M&A: a business that's ~10% of Uber's market cap, but adds ~20% to our trips and Gross Bookings and drives significant accretion post close. For Delivery, the transaction is transformational, roughly doubling our trip volumes and increasing GBs by nearly 50%.

$UBER buys $DHER for 14.8 B USD at an EV/sales <1.1. I think it's a great price.

Some european and LA parts will be sold off to SSW partners for 1.6 B USD to preempt regulatory hurdles.

In addition, they get some potential good assets in Emerging Markets: Foodpanda (Asia), Hungerstation (Saudi Arabia), Pedidosya (Latin America excl Chile&Ecuador) and Glovo (Eastern Europe excl Moldova, Poland, Portugal, Romania and Spain, as well as Africa and central Asia).

JPMorgan valued Baemin for around 5.25 B USD in may '26. This valuation is before a potential bidding war.

Baemin holds >50% markets share in South Korea and contributes to 25% of DHER total revenue. They are is indeed profitable.

I actually think mgmt did exceptionally well here on capital allocation. This transaction bypasses the potential bidding war on Bamin between $UBER, $DASH, $BABA and Naver just before the deadline in July. In addition, they get Talabat at a fair price + other potential assets.

In Uber’s existing markets, cross-platform engagement represents a highly efficient acquisition channel while also increasing engagement, with cross-platform users generating roughly 3x the Gross Bookings and profits compared to single-product users."

$UBER CEO on the $DHER acquisition.

"The transaction nearly doubles the number of markets where Uber will offer both mobility and delivery services, from 34 to 58 markets, substantially broadening the addressable base for Uber’s proven cross-platform strategy...

@joecarlsonshow "The world is not driven by greed; it's driven by envy." - Charlie Munger.

Congratz on your accomplishments. Been great to follow your journey and getting inspired.

@TheWiseIC The $DHER acquisition is prob about the middle east which is highly profitable and UBER may make it even more profitable by cross selling to UBER eats.

The rest will most likely be sold off to third party buyers.