#MKA

My two cents

List $MKAR which we are all quite excited about, then become a pure play NdFeB magnet company

Boston Dynamics is going to likely IPO in 2028, this will be our SpaceX moment

By that time we will be producing magnets in 3x continents, perhaps four

We will be the greenest, cheapest, most downside protected NdFeB magnet producer on the planet, ready for a growing circular economy

If between now and then we can prove our tech can recycle ‘robotics’ (which is highly likely) then we will be front and centre, a direct supplier and cost eliminator

It’s also likely AI will be screaming out for robotic entities to showcase its talents by then also

$CTH @CoTecCorp and $MKA.NE to considerably skyrocket in due course!

After the filing of the Form F-4 with the SEC, it is now pretty much a given that Mkango $MKA #MKA will list its subsidiary - Mkango Rare Earths $MKAR - on NASDAQ in the coming months, at a valuation of circa $500 million.

MKA's circa 79% stake will be worth ~$400m at the listing price of $10.

Using the current exchange rate of 1.34 and the existing total voting rights of 387.1 million, that equates to a value per MKA share at listing of 77.5p.

As of right now, MKA's share price is 46.5p / $241m mkt cap- a 40% discount to the value of its MKAR shares at the NASDAQ listing price.

Some might argue that UK stocks that have held shares in companies that have gone on to list on NASDAQ, have performed poorly.

MKA / MKAR is a very different situation. It will have complete control over the listed subsidiary (c.79% equity interest), and MKA's two key founding directors will also be the key executives at MKAR. Moreover, as most are now aware, the valuations of even early-stage development rare earth companies listed in the US and Australia are sky high.

So it's actually reasonably likely that we see MKAR push possibly significantly above its listing valuation, in those first few weeks post listing.

......

MKA is trading at a 40% discount to the value of its shares in MKAR; which means we're looking at a 67% increase from 46.5p, just for MKA to be trading at the value of those MKAR shares.

But then what about MKA's downstream and - most would argue - more valuable businesses? Its various magnet recycling and manufacturing operations?

Mkango now possesses in its downstream portfolio:

Three fully constructed and commissioned NdFeB magnet recycling / remanufacturing plants (two short-loop, one medium-loop), with a combined capacity of 1,200 tonnes per annum of associated NdFeB products. The two short-loop HyProMag plants could be expanded (with additional capex) by a further combined 1,050 tpa, bringing European capacity across the three plants to 2,250 tpa.

In the US, the three plants under development (combined nameplate totaling just shy of 4,700 tpa) boast a combined NPV of circa $2.2 billion. Management is talking of ultimately building at least seven of these plants in the US.

Mkango / HyProMag is also looking to roll out its unique recycling / remanufacturing plants in Japan, South Korea, Canada and elsewhere.

Given the 40% discount that Mkango is presently trading at to its soon-to-be-listed MKAR shares, Mkango's entire magnet business is essentially being valued by the market at LESS THAN NOTHING.

I have been petty vocal over the past year about the UK investment community. It is poor, weak, unadventurous - in short, the LSE is a dying exchange. It is the much more optimistic (and wealthier!) US investors looking across the pond at tragically mispriced UK-listed entities that have been driving the high volume reratings witnessed in recent months (e.g. Invinity #IES today and in the coming sessions!).

With NdFeB magnets playing such a critical role in so many hyper-growth industry verticals in the coming years, I think it inevitable that Mkango starts receiving that US investor attention in the near future.

Hannam & Partners recently initiated with a 2026 year-end 240p target price. Given how much the REE industry (driven by geopolitics) has heated up over the past few days, I suspect that could be broken with ease.

https://t.co/WTwRoqfV6D

#MKA bought a rare earth recycling business for €8m but the feedstock stockpile alone could be worth $1.5m-$6m+ 👀

300+ tonnes of NdFeB magnet scrap sitting there before you even value the plant, team & IP!!

That’s some serious asset backing on this deal

Hey @ParadisLabs

For clarity most of my net worth is listed in these two stocks for ONE technology, HyProMag

The stock(s) are called

#MKA $MKA.V

@MkangoResourcesMkangoResources

$CTH.NE $CTH.V

@CoTecCorp

The market: NdFeB magnets for Robotics, AI, EVs (something even $TSLA can’t replace)

They also have a patented technology to extract magnets from HDD’s (AI exposure)

First let me outline ownership so you know your money is in good hands

CEO of $CTH - Julian Treger (owns ~50% of the business) mining powerhouse famous for a massive exit in the 90’s, ex Anglo Pacific CEO

Both #MKA and $CTH have

100% global ownership of HyProMag

What is HyProMag 🧲

Rare earth magnet recycling via patented HPMS technology (hydrogen processing of magnetic scrap)

Does it work? Yes, proven in January and April 2026 in the UK and Germany, both plants now producing magnets and oxides. Real output, real customers, real performance.

AISC? $30 per KG max vs $59KG spot price, note $MP have a floor of $110KG which is WAY higher than forecasts

This is the lowest cash cost on record, no competitor comes close, honestly check the market.

US Interest? $92M EXIM LOAN

last update said discussions ongoing with 2 major US banks - FID expected June 2026 for total $145m package

You couldn’t be better positioned for the rare earth bottleneck than these guys who literally have magnets being made and approved only last month by @Siemens_Energy

What’s even better is HyProMag is leading a UK project with none other than LCM who are now part of $USAR with a valuation of $15m funded by the UK Govt

The connections are UNREAL

In short, everything you could ask for is here for the RE bottleneck

Cash? $CTH raised $20m in April and #MKA raised $24m in March

Also check out this video interview below (with a famous Canadian dragons den investor who owns $2m+) who can’t get enough of HyProMag! This guy was a host on dragons den and said this is the NUMBER 1 investment in his fund!

https://t.co/uJpuDdCXQn

Finally… the kicker… you ALMOST can’t lose as each company has other assets that back the market caps alone (#MKA has a $NSDQ listing coming for it’s mine est at $400m and $CTH has MagIron $1.67bn NPV with 17% ownership)

Off the charts value, coming soon to the US as individual technologies (Q1 27)

Yours for JUST $100m and $250m!

#MKA great to see Hannam & Partners out with a very detailed (50 pages!!) broker note, and a £2.40 price target

Huge upside potential from here (c.40p), with most of the key drivers due in the next 6-9 months

I will have to make time for a read of the full note later...

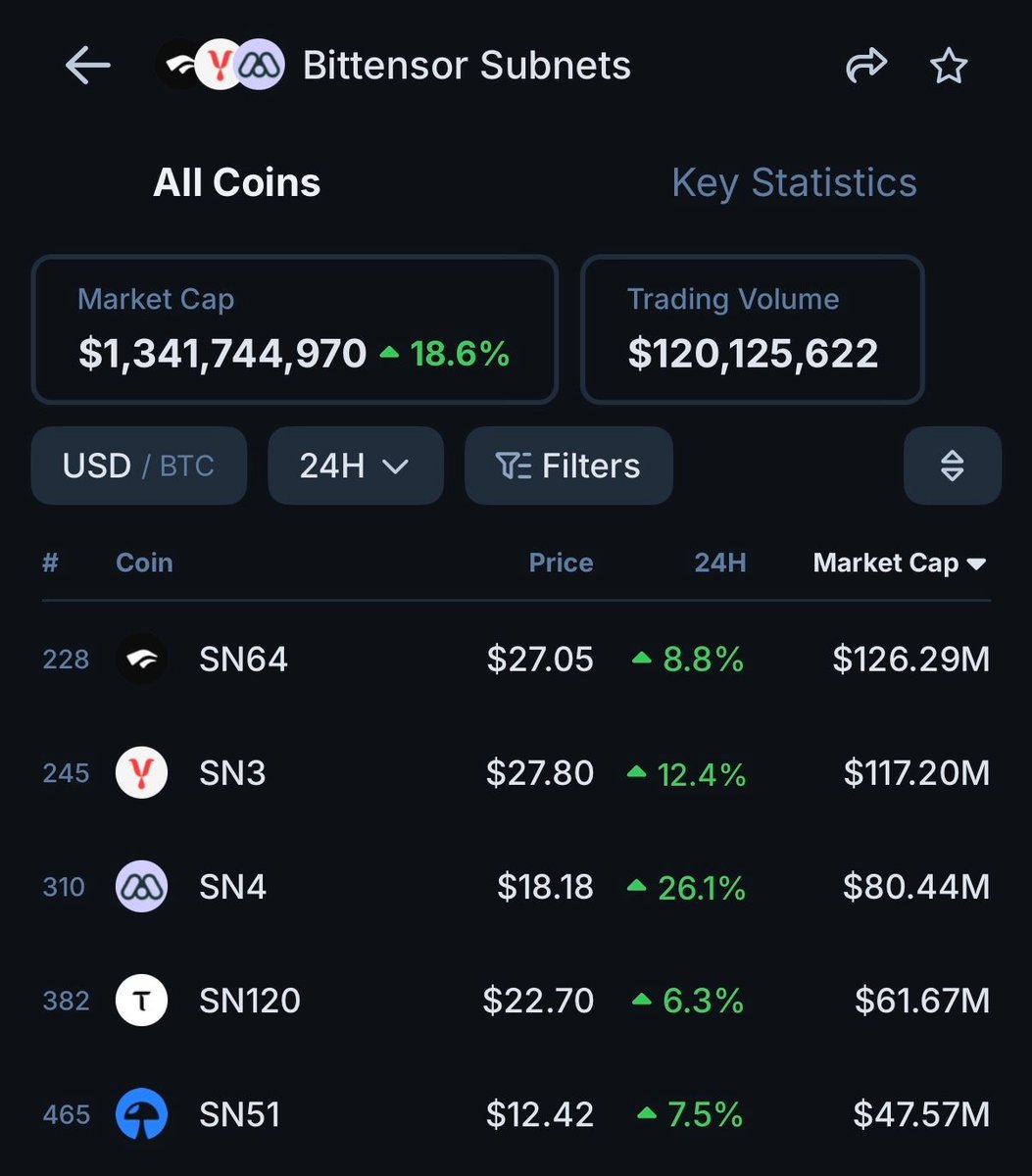

$TAO in subnets is now at 19% and it’s been a steady climb.

More capital is actively moving into subnets not just for speculation, but for real yield tied to network activity.

No other place in crypto is consistently offering 50–150%+ APY backed by actual utility, where emissions are earned through contributing compute, data and intelligence to the network.

As more people understand how Bittensor works, this trend will likely accelerate.

If you’re still sitting on the sidelines, you’re missing the phase where yields are high and barriers are low.

It's hard to ignore Bittensor right now. But most people still don't get it.

I've been deep in this rabbit hole for a while and the conversation has completely changed.

If you're just getting into $TAO and trying to figure out what subnets are actually doing, the best thing you can do is look at real data instead of just following the hype.

I've been using @taostats pretty much every day. It's where I go to check subnet activity, emissions, staking, validator performance, all of it. Once you start digging into the numbers it genuinely changes how you think about the network.

And they have their own wallet. You can check it out here: https://t.co/njyRhEIj2n

🚨BITTENSOR SUBNET BULL RUN?!

" $TAO is moving because there is actual demand for these SUBNETS!"

The highest market cap subnet is $100 Million. That is SO SMALL!

I predict a huge run for subnets like we seen with @Pumpfun & Meme coins on Solana $SOL

@opentensor

Bittensor / $TAO

If you’ve been hearing about Bittensor but still don’t fully get it, @firehustle_net just did a solid breakdown.

A lot of people are just now discovering it because of the recent AI narrative and most people on CT are talking about $TAO without really understanding how the network actually works.

This video explains it well.

MetaNova (SN 68) is doing for drug discovery what Templar is doing for AI training, replacing a billion-dollar gate keeping industry with an open, incentivized network. But it's important to note it's still early. $TAO

@JesusMartinez Great post, and he didn’t even mention the staking mechanism built in to the protocol. Price appreciation with real yield, all supporting the decentralized center of the universe for AI. It’s a beautiful thing.