For anyone new to markets, prices drop when asset owners sell and buyers don’t bid, even at small volumes (important point).

Sellers exit only because they think their forward gains are below their required rate of return.

Buyers don’t bid because they think valuations are as high as to prevent them from realizing their expected IRR.

If is just a bunch of people wanting out simply because they want to materialize gains, the rest of the market has enough cash to buy that volume if valuations are where they would like them to be and for sure they would not let something they think is fairly valued 40% before bidding.

Point being, markets drop if valuations are too high, not because people/institutions sell to materialize paper gains.

Never heard Dalio say anything interesting or not stupid.

We are out of this one.

We got interested because:

- Easy to understand business

- Strategic sector for national security

- LLMs make it hard to identify resilient software businesses, other hardware we are familiar with is priced high enough and so we are attracted by hard to disrupt businesses at a good price

- 50% of revenue from a market leading product protected by patents and incumbency effects with only 3.6% penetration, incoming (starting to hit in 2027/28) US drug manufacturing reshoring supports an acceleration in system sales

- 50% of revenue is recurring and derives from the revenues above (which means it’ll grow)

- Should grow topline (easily) at a 20% CAGR through 2030

- Fully ramped Gross Margins of 50%+ is very high in hardware

What we didn’t like:

- Cash burn is too high. Cash break even should be around 2029, at best. Unless we assume 2/3x system sales each of the next 4 years. And we are not comfortable doing that. This means they’ll probably dilute holders again, and that’s after $48M+ of SBC through 2030 on a market cap of $100M

- Management not credible with targets. From late 2024 through mid 2025 indicated a GM of 50% was achievable exiting 2027, breakeven would occur in 27 too, and no new financing needed. Instead, they pushed the GM and breakeven target to 2028 and issued $45M in debt at 11% interest last summer.

If they start catching big orders and system placements go in the 50-60s this and next year, then it could easily 3x. But we are not talking in hindsight here.

This whole process took us less than a week. We buy before we complete our due diligence, which can last 2-3 weeks. As soon as we have enough to get out, we do. We do this because waiting too long before buying, may mean that the stock runs up too much, and we don’t mind taking an occasional 5-6% loss if it means not losing plays that go up 70% in 8 months.

Currently up 14.7% for the year, with 31.3% in cash.

@jiahanjimliu@StockAnalystPro There is literally nothing there other than a summary of what they do that doesn’t mean anything to anyone that doesn’t know much about SpaceX (99% of people, including me).

There is a world where $NBIS and $CRWV catch a very bad hand.

$DOCN (to our knowledge) is the only public cloud player that wouldn’t be affected (and would actually benefit) if OAI or Anthropic or Google got their maths wrong in terms of compute needs and it becomes a disaster.

Not sure how you can touch those 2 when clearly any hyperscale contract they have is just temporary, $AMZN $MSFT $GOOG $META just need them for the time being.

3 (and maybe Meta too) of them have big incentives to literally destroy $NBIS and $CRWV.

Why didn’t they take any equity stakes? 🤔

Hm.

There is a world where $NBIS and $CRWV catch a very bad hand.

$DOCN (to our knowledge) is the only public cloud player that wouldn’t be affected (and would actually benefit) if OAI or Anthropic or Google got their maths wrong in terms of compute needs and it becomes a disaster.

Not sure how you can touch those 2 when clearly any hyperscale contract they have is just temporary, $AMZN $MSFT $GOOG $META just need them for the time being.

3 (and maybe Meta too) of them have big incentives to literally destroy $NBIS and $CRWV.

Why didn’t they take any equity stakes? 🤔

Hm.

It’s a good metric, yes. But can be lumpy so wouldn’t read too much into slowing customer count growth, especially QoQ. There is a lot of compute needed to fill current (3-4x, per Q1 mgmt comms) and future (10x+ by 2030?) demand for current customers.

We would like to see them add MWs and signal improving ARR/MW.

Nobody has the customer breadth and platform depth that $DOCN has in the neoclouds space. Only mature Hyperscale clouds do, and even their concentration is skewed towards the most expensive model providers.

+, for $DOCN, only a couple of new hundred MW of capacity needed for it to be on a $5B ARR.

Which means is worth $50B+ at that point.

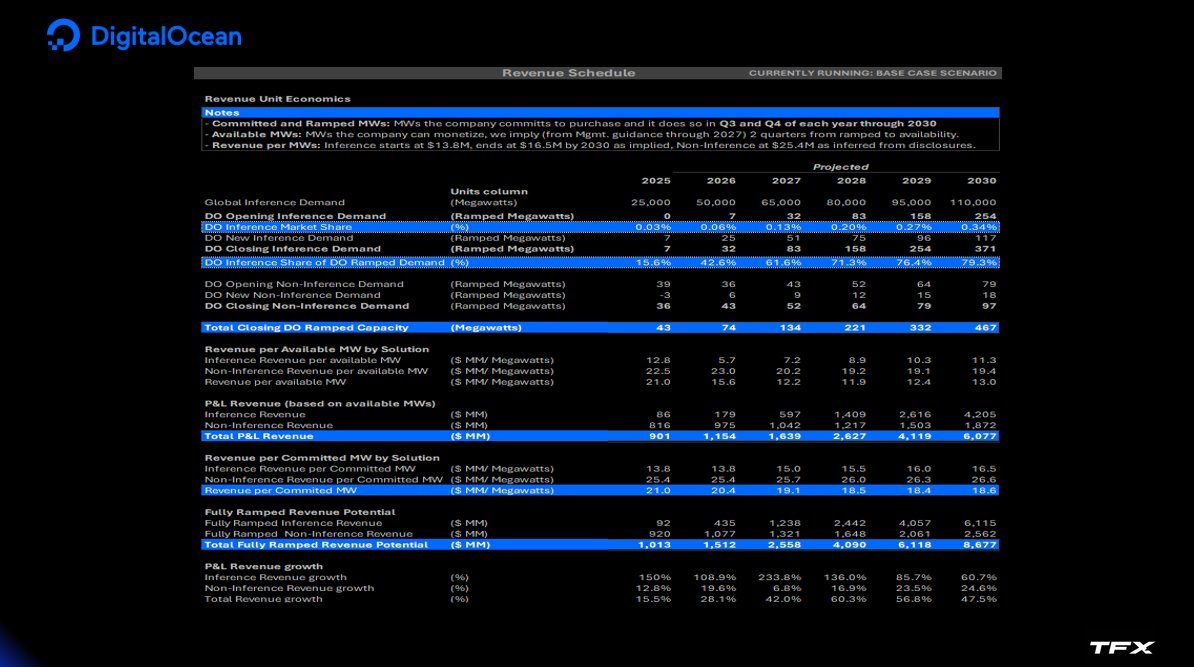

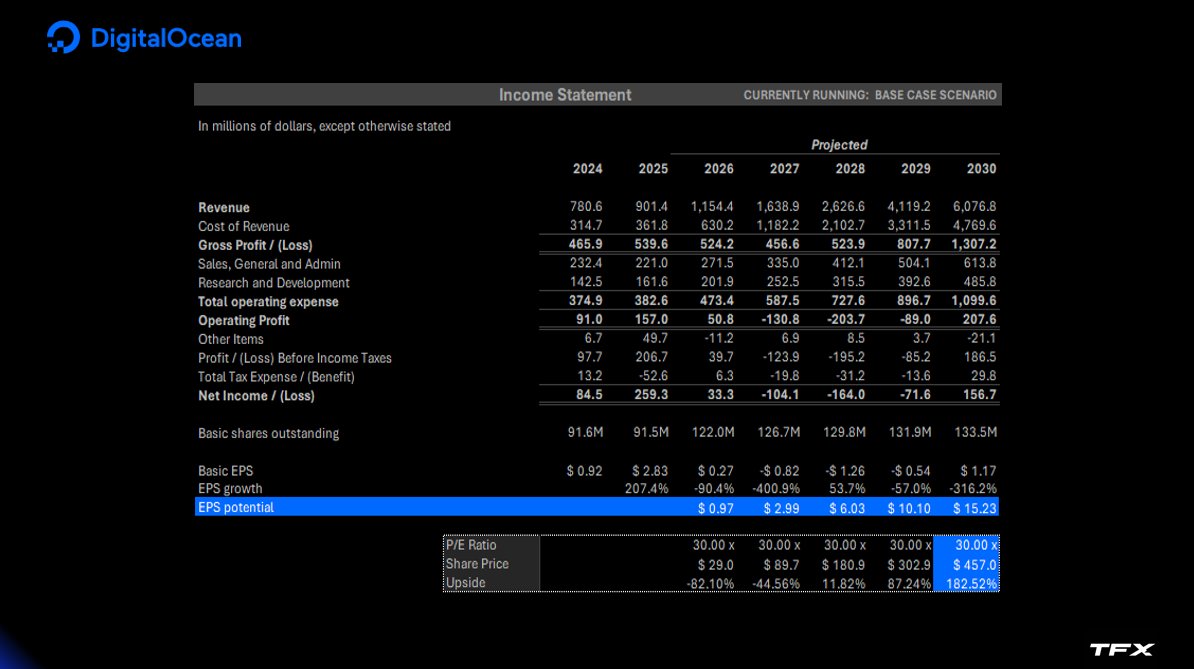

$DOCN update - 2030 Price Target at $457.

Key changes vs Q4 2025

- Higher Revenue/MW, from better platform pull-through (80% of total vs 70% in Q4'25)

- CapEx/MW will increase but was already modeled

- Added Cursor + other prominent wrappers

- Indicated that demand is 3-4x higher vs today's capacity

- Guided to 50% revenue growth for 2027 ($1.7B+)

- 80% of revenues (vs 70% in Q4) from non-bare metal

Other important notes:

Proven ability to attract and retain large customers

+ Product velocity accelerating

+ Focus on automated routing

+ Ahead of schedule 6MW ramp

= Increased platform stickiness, supported by flawless ramp executions creates abundant market trust to be rewarded for raising capital to capture higher demand from a source comprising of 10x new startups by 2030, with 15x more compute intense web traffic from agentic activity

Implications:

- Minimum of 467 MWs of sold capacity by 2030 is highly likely

- 2030 Exit revenue growth rate of 48%

- 2030 ARR of $8.7B based on inference running at $16.5M/MW by 2030 vs $13.8M today

- GMs of 41%

- OpEx of $1.1B including almost 2x headcount vs '26

- $133.5M S/Os (assumes $1.7B further equity raises)

- EPS of $15.2

- Exit PE of 30x

- Target Price of $457

DO has lowest customer concentration, 50-80% better economics vs neoclouds thanks to its holistic approach to cloud, much lower starting base (closing with 74MWs of capacity in 2026), has decade long experience competing vs hyperscalers, enjoys the widest community of developers and will be the primary beneficiary if the number of startups does 10x in 4 years.

$NOW CFO: “when seats end up being lower because AI is driving such incredible productivity, well, the only reason why they're able to lower seats is because they're using the AI. Well, we monetize the AI.”

Where did I read that before 🤔

Your ultimate guide against software bears.

Bear case 1: agents demonetize seats

Either:

- Agentifiable workflows replace whole seats and software sells those agents at high margins (FTE costs saved too high for companies to worry about how much $CRM is making out of it, especially when the alternative is leaving the platform - see below)

- Or, workflows cannot/should not be agentified, and software keeps monetizing seats.

Hence, only downside for software occurs where workflows exit the platform altogether. Keep this point in mind.

Bear case 2: LLM charged coding frenzy creates more alternatives and erodes incumbents pricing power and slows revenues

- There are 1,670 CRMs out there. 10x more than 10-15 years ago. $CRM offers, by far, the most expensive seats for off the shelf capability (non custom code, already replicated many times over).

Yet, if even SMEs keep choosing $CRM for off the shelf solutions at often 2x the price we can conclude that: a. Buyers are not as price sensitive b. Tech superiority doesn’t affect vendor selection (why would they pay $CRM more for standard features also offered by thousands of competitors)

SaaS buyers (especially MNEs) price vendors of non-core, mission-critical process software, for reliability at scale. That’s why $CRM has held up GMs and revenue growth even as alternatives have emerged in droves (many of which failed).

As a result, the more small players emerge, and erratically attempt to get customers to switch from or choose them vs incumbents, the more buyers will flock to the most reliable players. Incumbents will just need to keep pace with coding innovations, and they seem very aware of that.

So, if agents can run workflows, agents replace seats, but software sells agents. If agents don’t run workflows, software sells seats.

Software only loses if workflows exit the platform. Workflows exit if the value of exiting materially exceeds (at P&L level, not at cost centre level) the costs of exiting. Gross value = SaaS subscription fees (1-3% of buyers total cost base depending on size). On a net basis, that 1-3% benefit will be eroded by: data, process, and security configs migration, costs of retraining your employees and costs to retrain new entrants on software they have never seen before.

In closing.

What should $CRM be worth in 2030 once they show $60B subscription revenues growing (at least) HSDs at 35% net GAAP margins with 95% retention rates? $600? $650? $700?

Will see you there.

If OAI, Anthropic or $GOOG showed what $MSFT showed in that keynote, SaaS would go down 10%+ and those stocks would be up 20%+.

$MSFT is very compelling at $440.

What changes when agents become both a new unit of programming and an emerging new unit of human-to-machine interaction? The mission of Project Solara, a new software platform coupled with tailored hardware solutions, is to pioneer agent-first experiences that are shaped around you: your agents, your tasks, your environment, under your control. #MSBuild

What changes when agents become both a new unit of programming and an emerging new unit of human-to-machine interaction? The mission of Project Solara, a new software platform coupled with tailored hardware solutions, is to pioneer agent-first experiences that are shaped around you: your agents, your tasks, your environment, under your control. #MSBuild

@tbpn The fact that “Ferrari” and “BYD” are in the same sentence (and, for comparison purposes) says it all. It takes a special kind of loser to mess up worse than Jaguar did, and $RACE management are of that kind.

$CRM Q1 tomorrow.

Looking for traction in the following:

- Slack adoption as context for agents in key workflows (e.g. lead follow up, sales reps pre-meeting summaries)

- CCaaS push with voice agents with production grade quality guaranteed by Salesforce systems. That would confirm ethereum:0xba11d00c5f74255f56a5e366f4f77f5a186d7f55 heads-up of “very ambitious plans at Salesforce” to automate customer service calls.

Many sales and marketing workflows are probabilistic in nature which should facilitate faster adoption vs e.g. $SAP , at the same time, large companies (which is most of $CRM revenue base) have highly fragmented system landscapes, and work in geo/product silos.

Signs of AI revenue acceleration are possible to likely tomorrow, and would be rewarded. Deterioration is unlikely given that all other SaaS is reporting strength with their large customers (again, most of $CRM revenue base).

@SebJohnsonUK@LauraModiano Yeah, can’t think of anything better than getting your wrapper’s tech stack locked into a single model provider from the start.

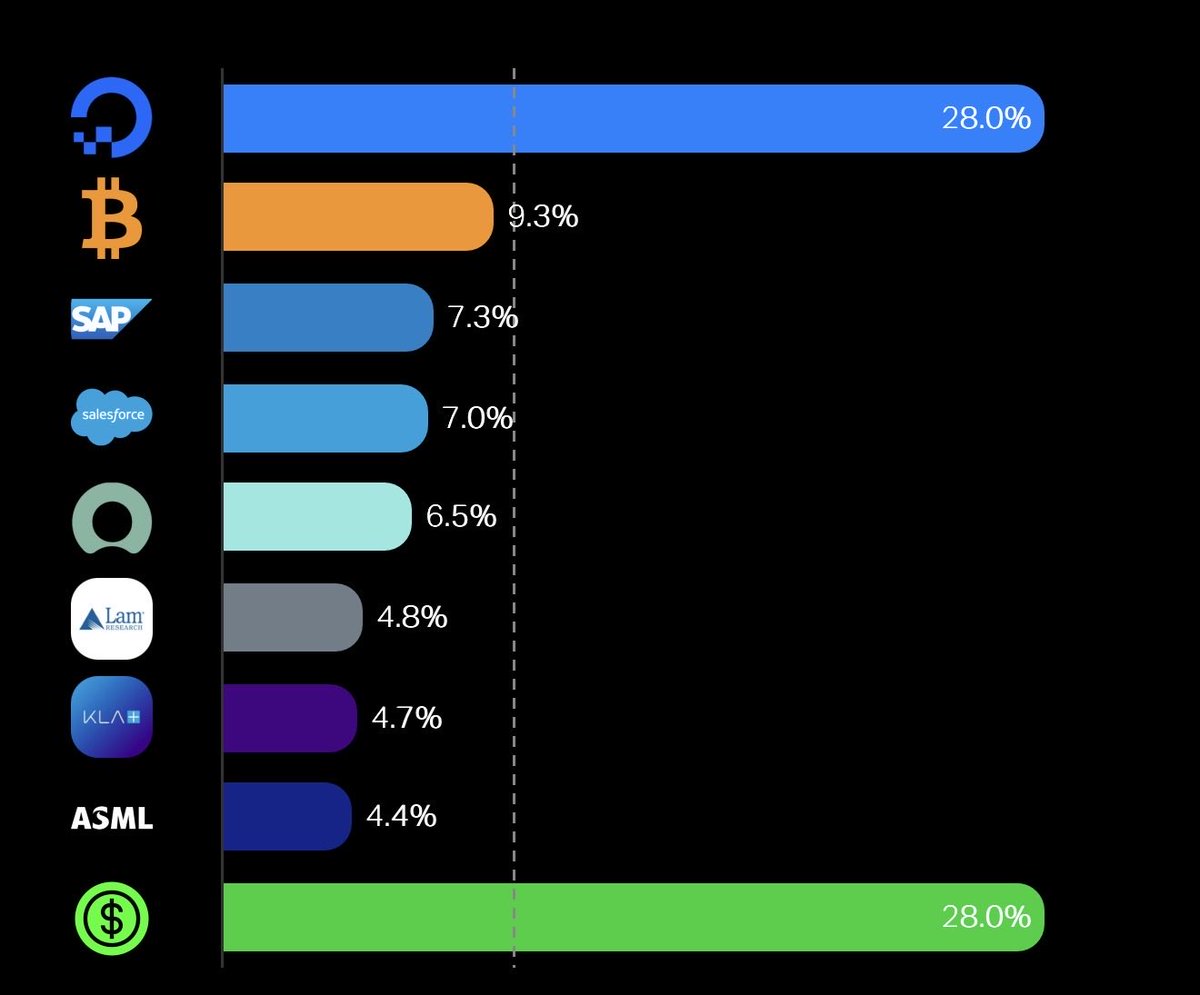

+27.3% YTD.

$DOCN drove most of the performance, Fab 4 did well too ( $ASML $LRCX $KLAC)

$BTC and SaaS ( $SAP $CRM $NOW) currently acting as a 9.2% drag on YTD growth.

Cash position still close to 30%. Will deploy on significant weakness only as bar to take more risk this year is higher given our performance and potential of the current base.

Other benchmarks YTD: Nasdaq100 up 14.7%, MAG7 up 6.6%, $GOOG (best Mag7 YTD performer) up 27.1%.

Key going forward is recovery in SaaS + $DOCN continuing to execute towards our 2030 forecast.

+13.74% YTD.

Still have a lot of cash to deploy.

Added $RPID with conviction. if any, outsized gains through 2026 will be led by this position. Will post our thesis here at some point.

$DOCN still our largest position. Focus on Katanemo’s ability to automate model routing (currently manual), and scope for Inference Revenue/MW improvement.

Our SaaS position ($SAP , $CRM , and $NOW ) is down 20% overall. But it will be fine. $CRM should report strong Slack sales. TDX outlook of “11%+ CAGR revenue growth from ‘26 to ‘30” implies $70B+ in revenues by 2030 vs $63B communicated in last earnings call.

WFE $ASML , $LRCX , $KLAC . 15.4% of our portfolio. Not selling. Too many long term catalysts and if they catch a down cycle and prices drop enough we’ll just buy more.

BofA’s sell side: “ $CRM has weakening upsell dynamics, and an underwhelming monetization pathway for its AI product, Agentforce.”

Meanwhile BofA management: “We use Salesforce Agentforce. We've rolled it out to 1,000 advisers to make those financial advisers become more productive. We've got 80,000 people on Salesforce.

So we're going to roll it out to 20,000 individuals by the end of the quarter, right?”

Sales is one of the easiest functions to drive usage up. Their “research” note won’t look good by the end of the year, if not sooner.

$CRM

BofA’s Athanasia at the RBC conference.

“We use Salesforce Agentforce. We've rolled it out to 1,000 advisers to make those financial advisers become more productive. We've got 80,000 people on Salesforce.

So we're going to roll it out to 20,000 individuals by the end of the quarter, right? If I was going to see you, we'd pull up all the information on you and break it down and allow me all that prep time goes away. Pre and post call. And there's other capabilities in it. But that's just a huge, huge time advantage, and we don't need a lot of admin sitting around creating that or the adviser to sort of spend time there. So huge productivity lifts there.”

Probably nothing.

Would rather believe $TSM Execs are telling us.

Guys like Curry and Kolanovic always miss “buying the dip” because they don’t understand much outside energy and macro stuff and P/E ratios (seems like?) and then complain of high valuations and make up things to make their arguments sound better.

Don’t care where these people (buy/sell side) worked/work, wouldn’t take any of them at their word.

Every company I worked with uses ServiceNow.

All their assets (software and hardware) get their details logged into the CMDB.

Al lot of what ITSM teams do is using those details to give/pause/terminate access to those assets.m, and resolve user issues.

Large companies, which is all $NOW deals with, only care about agents that will operate within boundaries. Boundaries means access or lack thereof to assets (entirely or in part).

As more agents move into production environments (day to day ops, not in development or testing), these will be logged into $NOW’s CMDB with every other asset. Once they are there, being the Control Tower (an orchestrator) of agentic activities is just a natural evolution for them, not something they are trying to force themselves in from scratch.

But, they will be able to monetize that control platform, easily. Veza and Armis make it even easier.

There is more to this company (e.g. NowAssist solving tickets autonomously), but the above is becoming a bigger story.

$NOW 2030 PT $215 - 258. Top reasons we own it:

Service as a Software play: most of the platform facilitates few and repetitive process steps with full view of asset IDs, customer details, approval rules, authorization checkpoints and workflow documentation centralized in the CMDB so E2E agents get deployed with minimal workflow outcome-risk.

Under-penetrated TAM: 8,800 customers only, 50,000+ companies (ex. China) available worldwide with 1,000+ employees and $100M+ in revenues.

Major data holder with embedded process logic, execution and outcome verification creates strong customer dependencies reflected in best in class retention rates.

Significant FCF margin expansion opportunity from headcount and SBC discipline.

@drugmoolah@Mindset4Money_X See, stuff like this will show up at some point. And is plausible/likely that material impacts will start in Q3/4 this year.

Running a big enterprise survey.

I'm direct:

"AI is a GOOD thing for this vendor- it makes it more valuable/important."

65 answers so far across the incumbent SW companies ( $SNOW, $NOW, $CRM, etc.)

53/65 said "Yes."

Never seen anything like this buyer/investor dissonance.

Good question.

A $150B valuation for ‘26 only occurs where there is a forceful shift in sentiment.

A forceful shift in sentiment in the short term (next 6-7 months) can only be catalyzed by a noticeable (3-5%) step up in revenue growth, on stable Gross Margins.

Otherwise, if they keep growing 20-19% a year, it would be around ‘28 ($23B Revenues, exit growth rate of 20%, 24% normalized net margin, 25x P/E) that they hit the $150 range.

You want to see/hear the below to see $150 this year:

“ We exited Q3 with 98% retention rate, accelerating NNACV, raise 2026 guidance for revenue growth by 2%, and we see 2027 revenue growth exceeding this year’s revenue growth”

“In Q4 our NNACV growth continued to accelerate driven by significant traction with our consumption based products and we are guiding 2027 revenues of $20B representing a 25% growth in cc for the year. NowAssist was $1.7B in ‘26 and we see it at $3.8B in ‘27”

Stuff like this.

Is this possible/plausible/probable?

We think is between plausible and probable as people underestimate how quickly AI adoption can scale in ITSM and CRM (a few steps, with approval rules codified and output objects within the same platforms).

That said, we hold it with a view that by 2030 the valuation should favour a satisfactory return for us even where the valuation stays low (20x P/E).

Thus we are not in a rush to see prices appreciate meaningfully in the short term.