@CiroDeSiena It's important to note that the last few years the market was really really good, and since you can't tell the future, it's typically a very very bad idea to invest borrowed money.

@CiroDeSiena It's a simple question to answer: Was the total market return greater than the interest rate on the loan. Nothing else matters.

The global ETF I use, based on the FTSE all world index returned 18.5% over the last 3 years. The average car loan was +- 12%, so yes, investing won.

@MuloiwaThendo I once owned 3 houses, now I own none.

Buying is only better when you have a crystal ball and can see what will happen in the future, or if you're a terrible saver and owning a house forces you to save.

If you can save and invest you'll end up way ahead renting.

@EMukumbo@francgroup Every asset type has a purpose. Of course if the market crashed the pictures would have looked completely different.

Now that I'm no longer earning a salary I have some fixed income assets in my portfolio for the first time. Just enough to survive a few really bad years!

The rest of the world always knew this, it was literally only the Americans who thought their stock markets reach was enough to consider it globally diversified.

There have been many top economic powers in the past, it's foolish to think there won't be new ones in future.

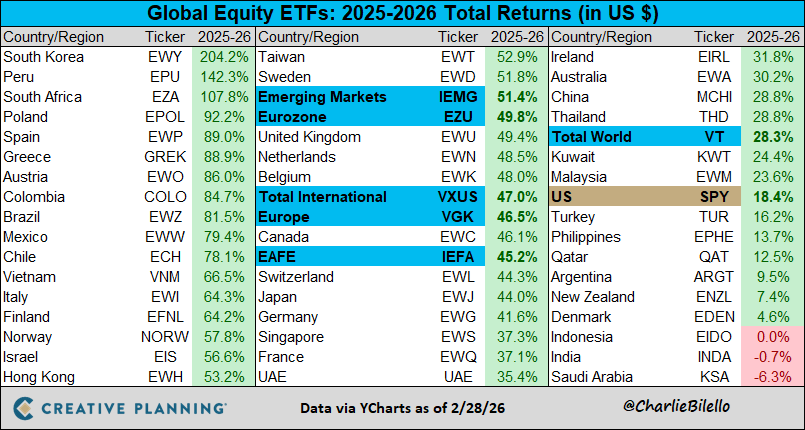

Start of 2025: ‘Why should I own anything outside of the US?’

14 months later: South Korea +204%, Peru +143%, South Africa +108% … S&P 500 +18%.

The future is unknown. That’s why you diversify.

Really good to see this! In my opinion a TFSA is the best investment you can make as a South African. I rank it above an RA. https://t.co/aLXvuSkopl via @Moneyweb

@mayaonmoney I know but run the numbers long term. You're front loading your taxes which get paid outside of the TFSA wrapper.

You end up with a R500k investment you'll never have to pay tax on again in your life. I believe if you do this early enough, the long term tax saving is worth it!

@iamkoshiek I once owned 3 properties, my home and two rentals. Being a landlord is at best a part time job, one where the stress to income levels don't add up.

I now own ETFs instead of properties, make significantly more from them and they cause zero stress!

@RamonJThomasMBA@EasyEquities To be fair, the Rand usually depreciates faster than the dollar, so under normal circumstances you'll see gains as that happens, on top of any gains in the S&P500.

Personally I've only ever held offshore ETFs in my TFSA, and been very glad I did.

For the last three years my wife and I have lives on our boat in the Med. I've just added up the budget, and it turns out it's actually cheaper to live in paradise than in a big noisy city. Here's the breakdown: https://t.co/yZ7EnW4kIj

Rule of thumb for globally diversified ETF investments:

1. If price drops, just hold

2. If price goes up, just hold

Then smile knowing that your returns will be better than practically all the experts out there 🙂

Rule of thumb for investment in fundamentally solid stocks:

1. If price drops 10%, just hold

2. If price drops 20%, add 10%

3. If price drops 30%, add 30%

4. If price goes up 10%, just hold

5. If price goes up 20%, still hold

6. If price goes up 30%, sell 10%

7. If price goes up 40%, sell 20%

8. If price goes up 50%, sell 30%

9. If price goes up 60%, sell 40%

10. If price goes up 100%, sell all

And now for the fun part.

Four years ago I bought a very old boat. Over the internet. Without seeing it or having it inspected. That’s textbook for how not to buy a boat.

The engines were toast. Every wire a death trap. Every valve a sinking waiting to happen.

It feels great to be okay, but I also feel guilt.

Why couldn’t I get my colleagues on the same path years ago?

Did I try hard enough? Should I have done more?

I hope they’ll be okay. They deserve to be.

I was preparing for FIRE long before my office closed.

So when it did, work didn’t disappear. It became optional.

That is the ultimate FU money.

Not fancy cars.

Not expensive watches.

Not a big house.

Freedom.