Everyone with a 30 year mortgage will end up forking over tens of thousands of dollars in interest directly to the bankers.

Chances are, you probably don’t know the real numbers. It could be almost half your loan amount, even if your interest rate is only 3%.

The front-loaded interest schedule that sends most of your first decade of payments straight to the bank costs a lot more than avocado toast. But nobody talks about that part. Easier to just stop eating apparently 🤷🏻

FDR invented the 30yr mortgage to bail out the banks after the Depression, but the boomers and millennials are still pointing fingers at each other

@Diogenesfailed I know, I’m such a spoiled millennial. How DARE I expect to be able to afford the same amenities my parents had at my age for the same income level 😭🤣

It’s a little of both honestly but neither one is the root problem. Politics have always been a distraction from what the banks have been doing the entire time.

(Extracting wealth generation after generation through front-loaded interest aka usury)

Boomers bought houses when a single income could qualify for a mortgage without selling a kidney. That window closed. The banks made sure of it. There’s a way around it nobody is talking about

@Mr_T____1776@anannoyedtexan The people who want to buy can’t qualify. The people who can qualify don’t want to overpay. Nobody wins except the bank collecting interest on whatever does eventually sell. Good ole usury

Bootstrap boomers have a lot to say about the cumulative cost of hypothetical avocado toast but nothing to say about paying more in interest than the house even costs. Why is nobody talking about that?

So can we stop with the “boot straps” narrative claiming it’s the avocado toast or Starbucks (both of which I sadly had to cut long ago but didn’t help me afford my house)?

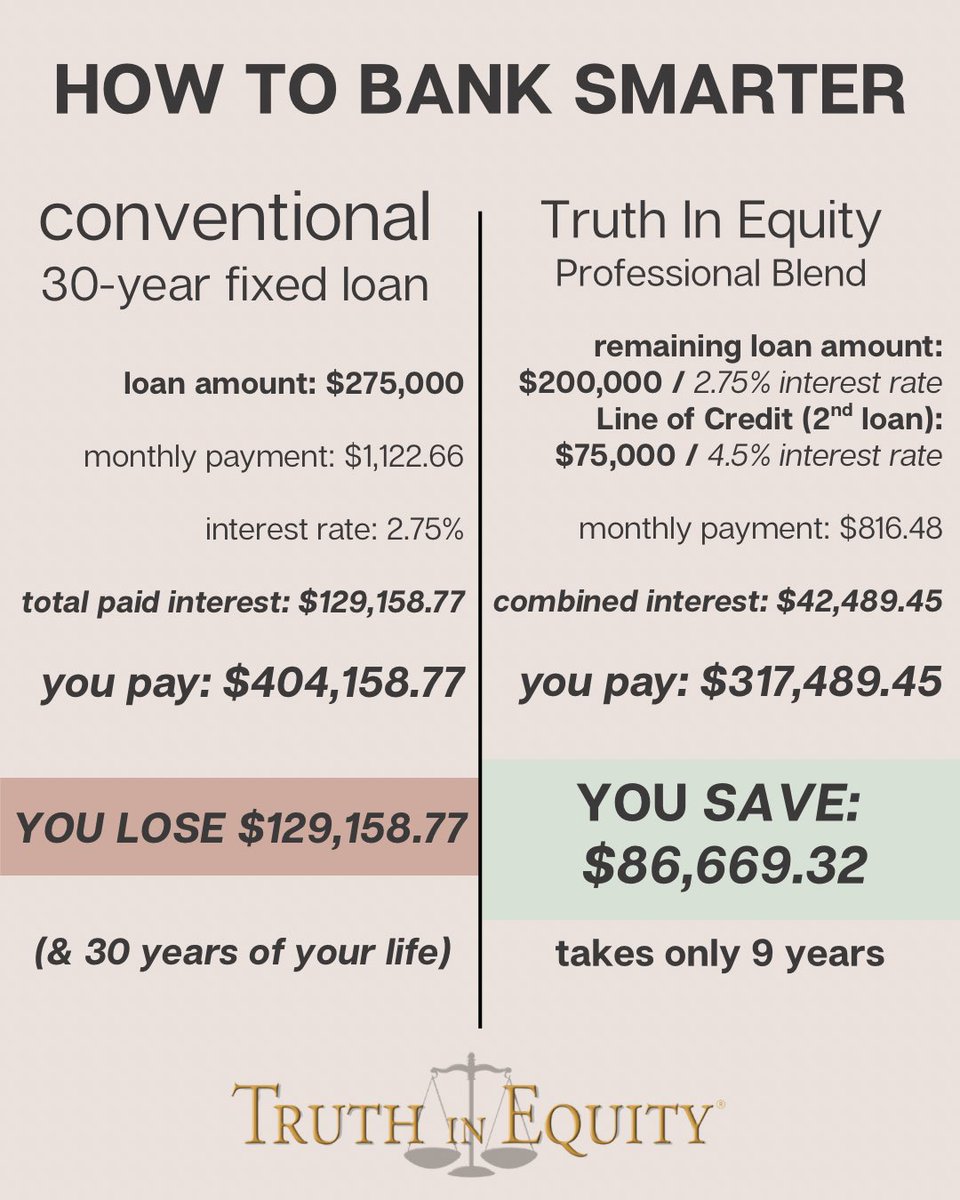

@basedbtc_@texasrunnerDFW You might be in a much better position than a lot of people especially if you locked in a good rate in 2021. But you can make your interest rate almost irrelevant by using a a HELOC to pay off your house in 7ish years. Same income. No refinancing. What’s your current balance?

@joshstrength@texasrunnerDFW Here’s something uplifting: There’s a way to pay off that unaffordable mortgage in 5 to 7 years on the same income you already have. No refinancing or extra payments. Run your own numbers here: https://t.co/TgK5LauHKJ

@MagnusFratus@msilva12000@texasrunnerDFW What’s your equity situation now? We’d love to show you how to pay it off fast and save a ton in interest without paying more monthly. It’s pretty easy, they do it in the UK and Australia but few people even know about it here because the banks are a bit more aggressive

Ok, so let's run the actual numbers.

$300K home, 20% down = $240K loan at 7%.

You'll pay $330K+ in interest over 30 years.

Your home tripling to $900K sounds great until you realize:

→ You paid $330K in interest to access that gain

→ The mortgage deduction saves the average homeowner ~$2,000/yr max

→ That's $60K over 30 years — still leaves $270K in pure interest cost

And appreciation? You don't control that. The bank's interest? You do.

Credit Line Banking on that same $240K loan with modest surplus income eliminates the mortgage in under 10 years — capturing the full appreciation WITHOUT paying 30 years of interest.

Why wait 30 years to build equity when you can own it in 10?

Respect the math on those 16 payments — but let's run the same $785K loan through Credit Line Banking: https://t.co/KwUlueMcgd

$6,575/mo surplus. $354/mo credit line cost. Net attack on principal: $6,651/mo.

16 extra payments gets you out in 15 years, 9 months. Saves $529K.

CLB gets you out in ~9 years, 10 months. On the same loan. Same income.

That's nearly 6 fewer years of payments — and roughly $290K more in interest savings.

@JanisTreem23413@OwenShroyer1776 “Interest is a huge problem BUT you can ask the government for some of those nickels and dimes back after the bank takes all the dollars.”

@JanisTreem23413@OwenShroyer1776 On a $300K home at 7%, you pay ~$420K in interest over 30 years.

You pay $420K to access how much in equity?

Interest is a huge problem in and of itself.

That California appreciation story is real but it’s also what 2008 was built on. Pulling equity every 5 years works until it doesn’t. The people who got caught holding that strategy when the market corrected lost everything…Paying the mortgage off fast, giving less money to the banks & owning the property outright is the only version of this that has no downside scenario for buyers, landlords etc. But unless people realize that, the banks still win 90% of the time.

You’re right. Most people sign them and never look at them again. And refinancing is actually part of the problem. Every time someone refinances, the interest clock resets and the bank starts collecting from the beginning again.

The average American refinances every 5 to 7 years. That’s their business model working exactly as designed.

Property appreciation is real but equity sitting in a wall earns you nothing until you sell or borrow against it. The total interest number isn’t a lie. It’s just the number a lot of people try to ignore.

You’re right. Most people glance at it at closing, don’t fully understand what they’re looking at, and never see it again.

They know the monthly payment. They don’t know that the first decade of those payments is almost entirely interest.

And even the ones who do figure it out usually assume there’s no other way — that this is just how mortgages work.

That’s exactly the gap we’ve been filling since 2006.

There is another way and the math on it is just as clear as the amortization schedule. https://t.co/mKLjyMPels

Most people never do this math. Here’s some more math nobody has shown you yet: What if that $3,970/month started in year 6 instead of year 31?

That’s 24 years of payments staying in your pocket instead of going to the bank.

Just under $1,140,000 back in your family’s hands.

We’ve been helping people do this since before the last housing crash. Run this example through our payoff calculator:

https://t.co/KwUlueMcgd

The real price of that ranch isn’t even $785,000.

It’s closer to $1.8 million.

A $785,000 mortgage at 6.5% costs you over $1,000,000 in pure interest over 30 years.

That extra million goes directly to the bankers.

Most buyers never see that number anywhere in the paperwork. Why?

If you bought this home today with a 30 year mortgage, it would be almost 90 years old by the time you pay it off.

Who is the next buyer in 2056!?!?

This market is so ready to collapse.

Obliviousness and intent are not the same thing. Boomers caused a lot of problems but most of it is because they are/were completely unaware. They underwent brainwashing on the level of what we are seeing in today’s youth. Their values and outlook were subverted by the people who run culture and finance.