$ASTS

THE FCC JUST TOLD YOU WHO THE REAL DIRECT-TO-DEVICE PLAYERS ARE

Today’s FCC release was not subtle. The regulator explicitly framed America’s future in direct-to-device connectivity around only a handful of serious infrastructure players, and @AST_SpaceMobile was named directly alongside SpaceX in the agency’s own messaging.

Read the language carefully.

The FCC states it already approved AST’s “competitive 248-satellite D2D system” and tied that approval directly to America’s “global leadership in next-gen D2D offerings.” That is extraordinary regulatory positioning for a company many retail investors still treat like a speculative science project.

Meanwhile, Brendan Carr is openly talking about a future with “at least three facilities-based providers” in D2D. Not dozens. Not unlimited competition. A small number of national-scale infrastructure winners. And AST is specifically being elevated into that conversation by the FCC Chairman himself.

What casual investors are missing is that this FCC document effectively confirms several things simultaneously:

• AST now has authorization for a 248-satellite commercial constellation in the United States.

• The FCC repeatedly emphasizes “competition” because regulators do not want a single-player monopoly in space-based cellular broadband.

• AST is integrated with AT&T, Verizon, and FirstNet using actual carrier spectrum and carrier core infrastructure.

• The FCC is signaling long-term regulatory support for D2D as strategic national infrastructure.

• The agency is creating clarity around exclusive-use spectrum rights and buildout expectations so companies can invest at massive scale.

This is the part the market still does not fully grasp:

AST is no longer being discussed as an experimental satellite company. The FCC is discussing it as part of the future architecture of American wireless infrastructure.

That changes valuation frameworks completely.

The government is openly talking about ubiquitous smartphone connectivity from space, rural coverage, public safety integration, competition policy, spectrum policy, and next generation industrial leadership. Those are trillion-dollar infrastructure themes, not niche themes.

And look at the players orbiting this ecosystem now:

AT&T.

Verizon.

FirstNet.

Google relationships.

Defense implications.

National infrastructure implications.

Potentially exclusive spectrum structures emerging around D2D.

The FCC itself is now effectively validating that direct-to-device broadband from orbit is becoming a permanent layer of the communications stack.

Retail still thinks this is a meme stock.

The regulators are talking about national strategic infrastructure.

FCC Chairman just approved $40 billion in D2D spectrum deals.

Named $ASTS and @SpaceX as the two companies leading America's D2D future.

Everyone is debating if this is good or bad for ASTS.

Simple version for retailers:

@SpaceX bought their own highway -- 65 MHz of owned spectrum. ASTS rents lanes on AT&T and Verizon's highway -- 700/800 MHz already in every phone on Earth.

Different models. Both work. SpaceX sells direct to consumers.

ASTS sells through carriers. Like how wireless has both Verizon (retail) and American Tower (infrastructure). Both are $100B+ companies.

What bears are missing:

AT&T and Verizon don't want to depend on SpaceX -- a competing wireless network -- for satellite connectivity. They want an independent partner they control. That's why they're equity investors in $ASTS and NOT in SpaceX D2D.

Also buried in today's news: AT&T acquired 50 MHz of new spectrum including 600 MHz low-band -- same family as the 700/800 MHz ASTS uses.

A stronger AT&T = a stronger $ASTS .

Now the valuation that should stop you scrolling:

SpaceX paid ~$25-30B for 65 MHz of D2D spectrum. Just the spectrum. No satellites for it. No service until 2028.

$ASTS entire market cap: ~$27B.

For the same price as SpaceX paid for a piece of paper, you get:

6 satellites in orbit, 33 in production, 98.9 Mbps proven, 248-satellite FCC authorization, 60 carrier partners, $3.5B cash, 3,900 patents, three new government contracts, factory at scale, and a mid-June launch on Falcon 9.

SpaceX paid $27B for future spectrum. $ASTS IS the future -- for $27B.

The FCC just told you both will coexist. The valuation says one is mispriced.

$ASTS

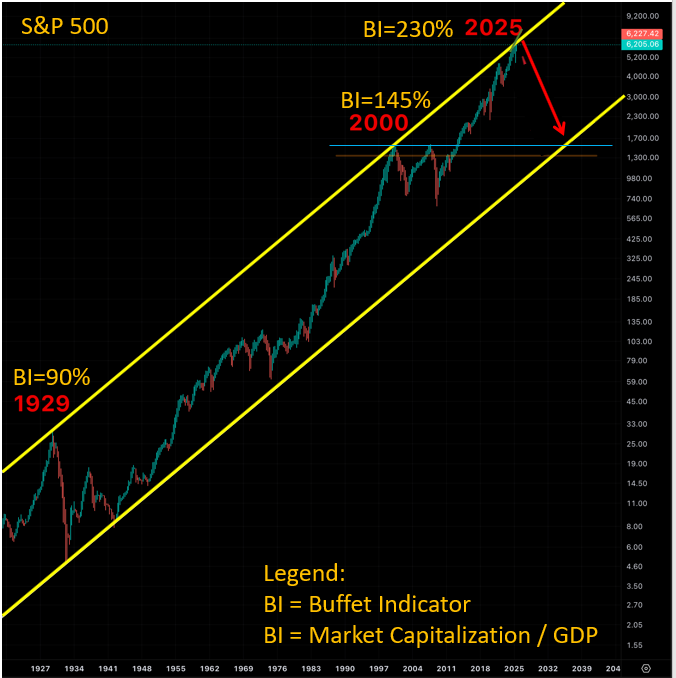

S&P 500: 100-Year Record Valuation

I shared this 100-year SPX channel chart several months ago.

Many laughed. Many claimed it was breaking out into a brand new bull market.

Still laughing?