After one year, I have finally published an article on @SeekingAlpha.

Bruker $BRKR is a life-sciences company that has outperformed the S&P by a wide margin for the last 15 years.

It has dropped -34% since all-time highs, so I decided to look into the business.

Link in bio!

🚀 Así Creamos un Fondo de Inversión con 24 años

Sin contactos. Desde Canarias. Desde cero.

En este episodio, te contamos todo sobre First Principles Fund:

→ Por qué tardamos año y medio en lanzarlo

→ En qué tipo de empresas invertimos

→ Por qué cobramos menos cuanto más grande es el fondo

→ ¿Bitcoin y oro en un fondo de calidad?

→ Por qué rechazamos un fondo ya hecho

→ Y una sorpresa al final que te va a hacer mejor inversor 🎁

Todo en el nuevo episodio de WorldStocks Podcast 👇🏼

(Enlace en la descripción)

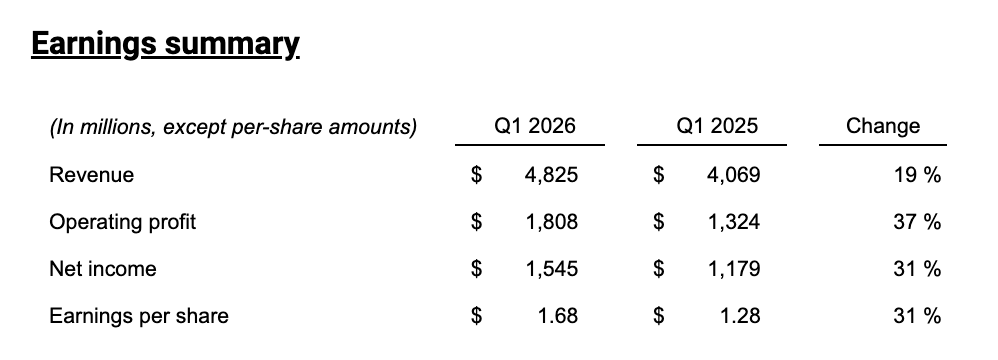

$TXN Earnings:

- Revenue of $4.83 billion, net income of $1.55 billion and earnings per share of $1.68. Earnings per share included a 5-cent benefit that was not in the company's original guidance.

- TI's second quarter outlook is for revenue in the range of $5.00 billion to $5.40 billion and earnings per share between $1.77 and $2.05.

https://t.co/h3oEqq3Qu1

🔥 ¡Nuevo episodio disponible! 🔥

Hoy charlamos con @GutierrezCap_, ex–analista de un Fondo de Inversión, y uno de los inversores más respetados de España.

💥 ¿Viene un GRAN Crash en los mercados?

💥 ¿Por qué ha vendido $META?

💥 ¿Hay burbuja en el S&P 500, la IA o NVIDIA?

💥 ¿Cómo proteger tu dinero en un mundo tan frágil?

Todo en el nuevo episodio de WorldStocks Podcast 👇🏼

$ULTA Good results. Comp growth accelerating, though at the expense of margins. Still, a lot better than expected. This turnaround feels good after suffering a -50% from ATH.

My conviction wasn’t the highest, but last months’ valuation compensated. It’s a good business, but I…

🥳 Ya está disponible la primera parte de mi tesis de inversión en Hims&Hers $HIMS

Está en abierto para todo el mundo. Ya no hay excusas para no entender qué es Hims.

📎Lo puedes encontrar en mi perfil.

Tuvimos un problema técnico con el episodio de hoy en YouTube ⚠️

Faltaban 30 minutos de contenido y preferimos retirarlo.

Mañana lo subiremos completo a las 12:00 (hora 🇪🇸).

Gracias por la paciencia y perdón por las molestias 🙏🏼

$ULTA Good results. Comp growth accelerating, though at the expense of margins. Still, a lot better than expected. This turnaround feels good after suffering a -50% from ATH.

My conviction wasn’t the highest, but last months’ valuation compensated. It’s a good business, but I…

$ULTA Earnings:

- Net sales increased 4.5% to $2.8 billion compared to $2.7 billion, primarily due to increased comparable sales and new store contribution, partially offset by a decrease in other revenue.

- Diluted earnings per share was $6.70, including a $0.01 benefit due to income tax accounting for stock-based compensation, compared to $6.47, including a $0.10 benefit due to income tax accounting for stock-based compensation.

- Net income was $305.1 million compared to $313.1 million.

- Comparable sales (sales for stores open at least 14 months and e-commerce sales) increased 2.9% compared to the first quarter of fiscal 2024, driven by a 2.3% increase in average ticket and a 0.6% increase in transactions.

https://t.co/XAkhRhmqHY

Founder-led businesses have a big edge. Founders are visionaries and strategic thinkers that fret over how to make it’s biz survive in >15 years. They’re always a step ahead (e.g. $META $NFLX).

It shows the power of incentives: protecting their precious gem (and net worth…).

After some weeks where it looked like the market would capitulate (according to “experts”), S&P is almost flat YTD.

I don’t know what’s next, but it seems that we’ve had the chance to buy high quality businesses at >20% discounts. Would be happy to have more discounts though.

Now that the market is down from yesterday lows… Yesterday I reduced my cash from 35% to 5%.

I won’t try to time the market (even politicians don’t know what’s next). We are lucky to have lots of quality businesses at attractive valuations, and I don’t want this ship to sail!

@SiemprePulpo@stonkmetal Fun fact, PPD is their largest acquisition since the merger. They spent almost $20B (13% of current Market Cap). PDD does around $8B in sales now so it’s around 20% of revs in CRO.

Experts say that they have been gaining share thanks to cross-selling.

@SiemprePulpo Being an “etf” they have relative exposure to those segments + their bioprocessing rev %, which is what is good now in LS, is low compared to other peers.

MSD+/HSD LT top-line growth + operating leverage and BB at this price and M&A makes it interesting now tbh.

@SiemprePulpo Let’s say that the overall industry pessimism, as well as the demanding previous valuation, are the main cause of the drop. Some niches are getting beaten down: CROs, academic, life science equipment… They still have Covid hangover.

Publicado el análisis detallado de Medpace $MEDP

Todo lo que uno necesita saber sobre la compañía y con las dos primeras secciones en abierto.

Comparte si te añade valor! Artículo en el siguiente post.

$EVO My take:

- Overall, deceiving results, especially in EU. It is affected by the aim to better comply with regulation. I expected this to happen but not this brutally, what has had a big impact in growth.

- EU should get back to yoy growth in 2026 (good comps don't help)

Portfolio as of today.

YTD performance (in EUR): -10.03%.

S&P YTD (in EUR): -12.72%

Bad start. Currency affected around -7%, so I still wouldn’t be positive. Lost around 3% of alpha yesterday due to the $EVO recent drop.

Huge thanks to @portseido!