From 2000 to 2013, the S&P 500 returned zero percent.

Thirteen years. Patience was the only thing you earned.

Buy-and-hold breaks during sideways decades. Options-income doesn't. That's the pitch in one line.

Weekly research → https://t.co/N5Y0WJRImw

In 1989~1991, I traveled the country putting deposits in mutually held S&Ls. At the time my net worth was under $10,000. I put the better part of my life savings in passbook accounts and CDs in the expectation that they would one day go public and that I would have the capital to participate in the IPOs which usually allow for investments of $250k-500k

A number of them went public during my days at Jefferies working for @HandlerRich in ‘91-‘94 allowing me to make enough (along with some generous bonuses from my employer) for my grub stake which funded the GP capital to launch Third Point on June 1, 1995. 35 + years later I have maintained all the accounts and periodically participate in the offerings to this day.

🚨 Yesterday I wrote that all four historic market risks – inflation, liquidity, tech, credit – are simultaneously present for the first time in 50 years.

Today let's zoom out further. Way out.

This chart shows 225 years of US stock prices, inflation-adjusted. It reveals something most modern investors have never seen, because the data simply isn't long enough in our living memory.

Roughly every 60 years, the market completes a full secular cycle:

– 1802 → 1857: 50-year rise, ended with US secession war and 5 years down

– 1857 → 1920: 63-year cycle, ended with WWI, post-war inflation and 11 years down

– 1920 → 1981: 61-year cycle, ended with oil shocks, Vietnam, stagflation and 13 years down

– 1981 → ?: the current cycle

If the pattern holds, the next secular top arrives around 2028. Followed by a 10-15 year inflation-driven drawdown that bottoms somewhere between 2039 and 2043.

The recipe is always the same

Each secular ending has three ingredients:

1. Persistent inflation

2. Geopolitical conflict (war, deglobalization, empire transition)

3. A speculative melt-up in the dominant sector of the era

The 1850s had railroads.

The 1910s had electrification and trusts.

The 1970s had the Nifty Fifty.

The 2020s have AI.

We're already two of three in 2026. Inflation has returned. Deglobalization is accelerating. The AI melt-up is the missing piece, and it's underway.

Why this matters

The playbook that worked from 1981 to today was defined by one regime: falling rates, globalization, passive flows, US tech dominance.

That regime ends with every 60-year cycle. Historically, the next decade rewards a completely different set of assets.

What worked in the cycle just ending:

– Long-duration growth

– Passive index investing

– US large-cap concentration

– Tech

What has worked through every secular transition since 1800:

– Cash-flowing businesses with pricing power

– Real assets and infrastructure

– Defensive, durable, boring

– Active stock selection

The uncomfortable part

Every cycle felt unique to the people living through it.

The 1920s investor was certain the new technologies of his age were different from the railroads of 1857.

The 1968 investor was certain stagflation couldn't happen in the modern economy.

They were all wrong in the same way.

If we're somewhere near the top of cycle four, the quality stocks being mocked today aren't dead money.

They're early.

Most investors focus on whether to buy a stock. Options income forces a more useful question: at what price would I want to own this business? That discipline alone — before a single contract is written — separates systematic income from speculation.

CHARLIE MUNGER ONCE EXPLAINED WHY CAPITALISM BEATS EVERY OTHER SYSTEM IN ONE STORY

Warren Buffett's partner of 40+ years didn't use a chart or a theory.

He pointed to a single number out of China:

"When the Chinese went away from collective agriculture and let each peasant have his own plot of land, and he got to keep the crop after his cost, the grain production went up 60% the first year."

"Now who in the hell would want collective agriculture when it was that inefficient compared to capitalist agriculture?"

His point: people take care of what they own.

"If you're managing your own affairs you're going to be pretty efficient because you're taking care of your own property. If you're working for somebody else, no matter what, you care more about yourself and your family than the telephone company you work for."

The Chinese communists agreed. They'd rather have the extra 60% of grain. So they changed the whole system.

Warren Buffett: “We make business predictions about what individual businesses will do over time. And we compare that with what we have to pay for them.”

“We’ve never made a decision based on an economic prediction.”

A cautionary tale for SpaceX and Anthropic buyers:

“There are zillions of IPOs every year and buried under those IPOs are few cinches that a really intelligent person could find and pounce on.”

“But an average person buying IPOs is going to get creamed.”

- Charlie Munger. 2004

Berkshire Hathaway has done 3 major Google buys:

> Q3 2025: $5B

> Q1 2026: $11B

> June 2026: $10B private placement

The $26B Google investment is ~$32B after gains (3rd top equity holding after Apple and Amex). Google bet getting close to $36B Apple bet Buffett did in 2016.

Bill Ackman bought a third of a $20 billion company after it crashed to $100 million - the stock went from 34 cents to $34

it's the most contrarian bet in modern Wall Street history

"I called the CEO, he didn't return my call - I called again, he didn't return my call - six weeks later they spun off the company, the CEO got fired, then he called to thank me for his exit package"

"there are analogies to 2000 - people got excited about internet stocks and Berkshire traded at the lowest valuation in its history because people said that's all old stuff

a similar thing is happening today to Amazon, Meta, Microsoft - they're undervalued"

bookmark and watch it today - 29 minutes that will change how you think about AI, markets, and what makes a great investment ↓

Speculative growth appetite is back near bubble-era peak levels.

Valuation dispersion is wide again. Historically, some of the best future relative returns for profitable small- and mid-cap value stocks have emerged when investors become most enthusiastic about unprofitable growth.

Value investing and options income share the same foundation: you need a price at which you'd genuinely want to own the business. Without that anchor, strike selection is just guessing. No momentum chasing, no lottery tickets.

A cash-secured put is not a yield trade — it's a conditional purchase agreement priced by implied volatility. If you wouldn't buy the stock at the strike, the premium doesn't justify the obligation. Free primer on the mechanics: https://t.co/N5Y0WJRawY

Not one, not two, but three S&P 500 sectors are testing either Dot-Com or GFC extremes. Relative to the rest of the market, Healthcare is back to March 2000 specifically. Consumer Staples = Dec. 1999. The S&P 500 Financials sector just broke March 6, 2009.

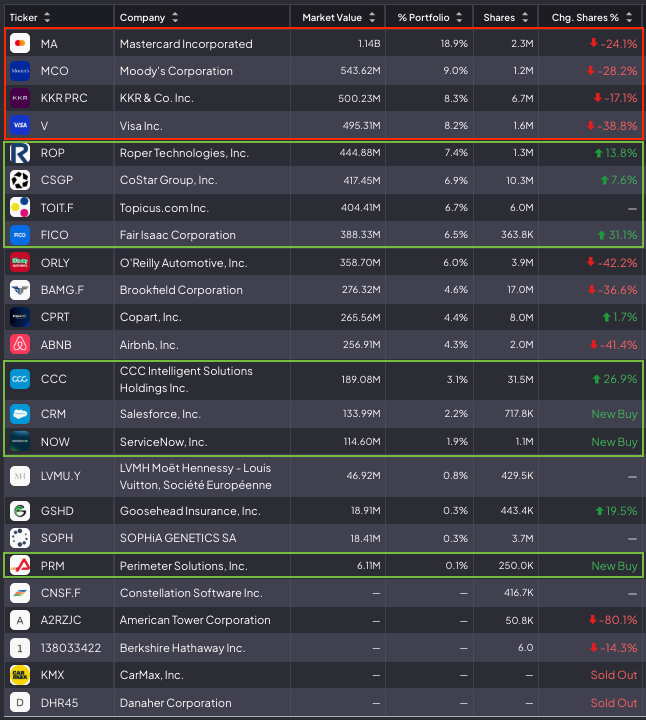

Akre Capital Management is pivoting out of its long-term holdings into software:

Sells:

$MA -24%

$MCO -28%

$KKR -17%

$V -39%

$ORLY -42%

$BN -37%

$ABNB -41%

Buys:

$CRM (New Buy)

$NOW (New Buy)

$PRM (New Buy)

$ROP +14%

$CSGP +8%

$FICO +31%

$CCC +27%

Mohnish Pabrai remembers Charlie Munger on @myfirstmilpod.

"In every way possible, he selflessly tried to be useful."

"I met so many partners he had in different businesses — [and he] always gave them the better deal."

"One day before he passed away, he was in the hospital — he knew he was dying — [and] he was trying to get one last grant done to a non-profit. No upside to him. He was dying."

"Charlie extracted everything he could from his mind and his body."

Peter Lynch: "There’s a 100% correlation between what happens to the company and what happens to the stock. The trick is it doesn’t happen over a week or even 6-9 months...

That’s terrific. Sometimes fundamentals get better and the stock goes down. That’s what you’re looking for."