Roman Chernin on 20VC podcast: If they had 10x the capacity overnight, they could still sell it reasonably quickly, because "we certainly have the demand for it."

It's very rare that a company can say this and it is likely true. That gives significant pricing power to the capacity they do have.

$NBIS

The 25-30% QoQ DRAM price increase in C3Q26 would compound on top off ~+95% QoQ in Q1 and ~+55% QoQ in Q2. The growth rate gets smaller, but in an absolute sense the EBIT increase will be almost as big.

Additionally, Bernstein sees HBM4 pricing at $53/GB in 2027, up from $16.6/GB. This will significantly increase 2027 EBIT after $NVDA locked in HBM-prices before the memory surge on an annual contract.

Jensen said the "memory shortage will persist for quite a few more years."

Elon sees a huge gap between too little memory capacity being added and future demand.

-> Memory prices will rise further and multiples are still too cheap, because the shortage seems unlikely to end before 2030 IMO.

$MU #skhynix

Morgan Stanley: Server OEMs expect another 25–30% Q/Q increase in DRAM pricing in C3Q26, alongside a further 20–40% Q/Q increase in NAND prices.

* This suggests that 3Q DRAM pricing could deliver another upside surprise, as current market research firms and sell-side analysts are expecting only a 15% increase.

$DELL call had a very bullish read-through for memory and AI compute in general.

“Demand continues to exceed supply, with memory as the primary constraint.”

"We don't know how big the TAM is other than we know it's bigger, it's growing, and we're in the early innings of it."

"The premium for computational capability across edge devices, PCs, smartphones, servers, and GPUs continues to grow at a rate we've never seen and is pulling the rest of the ecosystem."

"I don't think applying historical models or historical views about the market and how it's going to act are appropriate today. What's the value of adding intelligence into every workflow, every decision, every product, every customer interaction? I would assert the value is pretty darn high. And that's what's been really, I think, the game changer since that October time is what's really happened in agentic. And what you're seeing are new categories of TAM expanding."

$MU #skhynix $NVDA $NBIS

Leopold Aschenbrenner made $NBIS his by far largest holding.

It's one of my biggest holdings too, because I really like the team and what they are building, AI compute demand really seems insatiable and will keep growing much bigger. Nebius is still cheap based on my longer-term projections, despite the large increase in the stock price, because the great news like the hyperscaler deals and large prepayments keep pushing my intrinsic value estimates higher.

UBS says memory long-term agreements have price floors only slightly below current prices. It's unclear whether the agreements allow for price upside.

With 5-year contracts, Micron trading around ~5.6x near-term EBIT-runrate and SK Hynix at an even lower multiple, both still look very attractive.

I expect AI demand to be so large that even the supply they bring online end of 2027 won't break the bottleneck. We may be transitioning to a structure where memory makers expand mostly against contracted demand 5 years out, making them less cyclical than in the past and deserving of higher multiples.

$MU #skhynix

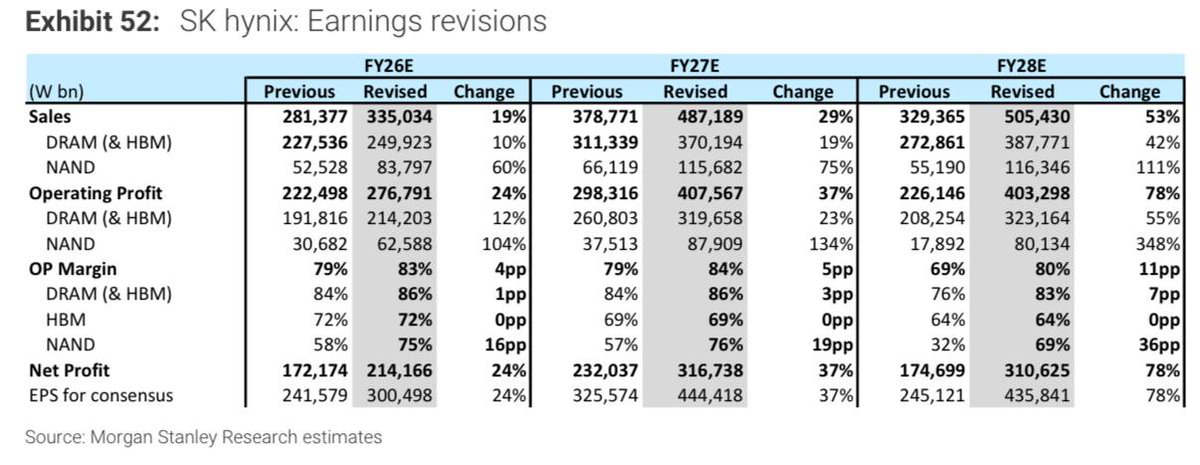

Morgan Stanley's newest EBIT-forecasts for SK Hynix:

FY26: KRW 277 T

FY27: KRW 408 T

FY28: KRW 403 T

Current Market Cap: KRW 866 T

Hard to reconcile these earnings with this valuation. I'm long.

I think so, yes. Taiwan had a multi-month buffer. SK Hynix and Samsung had like 6 months worth of Helium and procured more from diversified sources to further reduce the risk and they are also working harder on recycling Helium.

Micron should be totally isolated from this risk as US-based with the US being large Helium-producers. They also said on the call they see pretty much zero supply risk from the Iran war, which would be a pretty risky statement if they needed to be worried.

Helium also has lower-priority uses like party balloons, which obviously get cut way before critical semiconductors. So unless the war takes forever, this should be no problem. Given how high memory margins are, who cares if they need to pay double or triple for a small input cost? If margins go from 81% to 80%, that doesn't really move the needle.

Memory stocks are down on Google's TurboQuant reducing memory demand in KVcache by "6-8x" by compressing down to 3-bit.

But the paper was published a year ago. In the blog post linked below, $NVDA wrote Blackwell will soon reduce KVcache further down from 8-bit to 4-bit. So the incremental step is closer to 4 -> 3 bit in new setups. So a 25% reduction rather than 6-8x.

Also, KV cache is only part of total memory (weights etc. unchanged), so total memory reduction is much smaller.

And lower memory per token typically increases usage through higher ROI for hyperscaler (Jevons Paradox).

$MU

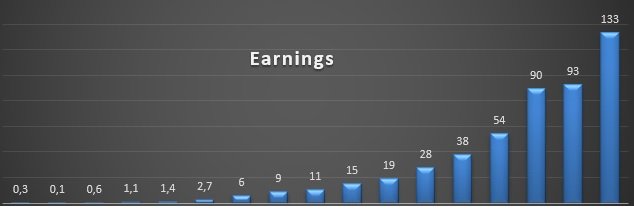

South Korea’s semiconductor exports are up +163.9% YoY for March 1-20, after being up 134% in February and "more than double" in January.

Memory profitability keeps accelerating. Good for SK Hynix.

#SKHynix $MU

Jensen says H200 will be sold into China in a few weeks. Chinese companies finally gave purchase orders, signaling they got Chinese authorization. U.S. government issued the export licenses. In his eyes it is a done deal.

Once the U.S. companies have Vera Rubin out, he'll ask Trump to sell Blackwell chips to China.

He refuted the Reuters report though that NVIDIA will sell the new Groq chip to China. "Totally false."

https://t.co/YIoaOYBCl9

$NVDA will not only start selling H200 again to the Chinese, but may also sell the brand-new Groq chips.

Neither Groq nor China are in the $1 T order visibility.

After all the back and forth on China, this won't be the final word. But China surely would LOVE to buy a new chip and Jensen met Lutnick yesterday, so they must have talked about it.

https://t.co/MLmrVMYuRd

Samsung talked about 3-5 year contracts at their AGM.

It's a big change that reduces cyclicality and suggests AI demand is structural rather than a short-term buildout that fades.

https://t.co/3g5fTDDKOE

"SK Hynix chairman expects memory shortage to last until 2030"

Memory makers now seem willing to stabilize memory prices in return for adopting a less cyclical industry structure. Hyperscalers seem to increasingly lock in 3-5-year supply with very significant prepayments. Probably memory makers commit to using some of that money to build more badly needed supply with less risk.

Memory per GPU keeps rising and rapidly improving GPUs and AI capabilities increase demand, which means memory demand keeps growing strongly.

Yet memory stocks trade at low forward multiples as if earnings will collapse in 2-3 years. But if demand grows rapidly and supply gets increasingly built against committed demand, the traditional boom-bust dynamic should be significantly less severe than in past cycles.

I expect great earnings from $MU tomorrow and also like SK Hynix.

https://t.co/bTKg5I62MC

#Breaking Nvidia CEO on China: "We have received purchase orders, and we're in the process of restarting our manufacturing. And so, so that's new news for all of you, and it's different than it was two weeks ago or three weeks ago" 1/2 $NVDA

$NVDA increased Blackwell + Rubin order visibility from $500 B (2025-2026) to $1 T (2025-2027).

Importantly, this excludes Hopper (significant in 2025) and other products (e.g. Groq, Vera CPU racks, self-driving tech).

Crucially, this doesn't mean $NVDA expects to earn "only" $500 B in 2027 (~7% above estimates). This is order visibility 9 months before the year even starts! Jensen explicitly said this pipeline keeps growing.

The market seems to interpret this as revenue guidance for 2027. But order visibility doubled in just 4.5 months and they can clearly take more orders. It seems VERY likely that they will get more orders for 2027 and do significantly better than $500 B.

You are worrying about genius moves.

Jensen secured memory supply early before prices went parabolic. Now just a couple months later he would have to pay at least 50% more like all the others. Google fired its purchasing manager because he did not secure a LTA agreement early like Jensen. This was a great investment that already clearly is paying off.

Securing future wafer capacity at TSMC helps with a 2nd key bottleneck. Others can't build as many chips as they'd like and reduce NVIDIA market share, because TSMC allocation is limited, NVIDIA secures so much ahead of time and TSMC won't expand unlimited. So $NVDA keeps growing and the growth of competitors stays bottlenecked.

$AMD doesn't have the money to do this and the hyperscalers need theirs for large capex. So $NVDA is the only one that can really do this, making it a moat.

So I consider both of these genius moves and hope Jensen makes more of them.

Inventory growth is also not worrying when revenue is growing > 2x faster.

Accounts receivable days of sales outstanding also went down from 53 days to 51.