Venn is a factor-based analytics platform designed for asset owners managing multi-asset class portfolios, including those with an alternatives allocation.

This Venn spotlight focuses on a University hospital system that has about $9 billion in annual revenue & $9 billion in investments & leverages Venn to help support key investment decisions.

The Venn subscriber featured in this article was not compen...

https://t.co/bnSput2BNo

Discover how tariffs and policy shifts since the recent U.S. inauguration have caused divergent factor performance in the U.S. and U.K. Our analysis dives into global and local factors, discussing actionable insights for strategic portfolio construction.

https://t.co/67mHgHe5w9

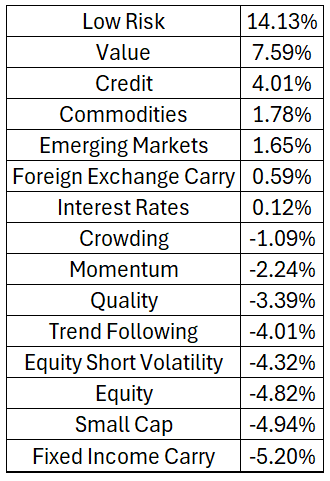

Five out of our six Equity Styles registered historically significant performance in February. This implies larger than normal performance swings for institutional investors. Come learn more about the performance of our Equity Styles and...

https://t.co/fOOKp9skld

January's market was a rollercoaster: from bullish CPI data to the DeepSeek AI shock. We analyze Equity Style performance before, the day of, and after the DeepSeek news rattled markets.

https://t.co/BC2dFXLsQ2

Equity Styles were among the best and worst performers in 2024, with other factors also having a standout year. Check out our latest report to analyze calendar year performance through the Two Sigma Factor Lens!

https://t.co/ztFmM2Hsz0

Asset class analysis can be useful to assess the impact of the recent Presidential Election, but the Two Sigma Factor Lens may offer a different and potentially more precise understanding.

https://t.co/EYZWik2HrV

Explore how October's U.S. themes, including the presidential election and rate cut expectations, impacted key factors such as Fixed Income Carry, Interest Rates, Trend Following, and Foreign Currency.

https://t.co/baPyGI5Yoi

September marked the first interest rate cut by the Fed, and it was a big one. Fundamental risk factors reacted, which ultimately matters for investors' portfolios and risk exposures.

https://t.co/1CeUUypWmw

We believe that conducting quantitative analysis is essential for making more informed asset allocation decisions. Read more about how this thinking pertains to Conservative, Moderate, and Aggressive fund categories, and why there is of...

https://t.co/6mDQBpYUVn

Join @VennTwoSigma and SimCorp's webinar on Wed, Oct 23rd at 11AM EST. This goes over our research regarding the relationship of Conservative, Moderate, and Aggressive fund categories. https://t.co/a29SpblkPV

https://t.co/KxgCPeshsa

Discover why Venn’s Foreign Currency factor is crucial for portfolio diversification and risk management in today's market. In this month’s report, we review the methodology and design of this factor, and explore August and historical results.

https://t.co/vv2TqvEUyn

Explore how fundamental risk factors performed before and after recent U.S. presidential elections, as well as during different government compositions.

https://t.co/aBLZZfuvSa

See risks here - https://t.co/bWThyBiReB

https://t.co/aBLZZfuvSa

Explore July's performance of the Two Sigma Factor Lens, analyzing macro and style factors, with commentary on tech sector trends and carry dynamics.

https://t.co/6olZD6rdBr

See risks here https://t.co/Irjnfdm1Tv

https://t.co/6olZD6rdBr

Join us for a Venn Webinar on Wed, July 31st at 11AM EST. The webinar will showcase core workflows such as manager due diligence, unearthing multi-asset portfolio risks, and comparing current and proposed portfolio.

RSVP here: https://t.co/N4egyglLeM

https://t.co/l2DYFCnzYX

Explore Venn’s new peer group analysis tool, designed to compare investment managers against their peers and understand their performance within the context of a competitive landscape.

https://t.co/65gyc15jMn

April proved to be an eventful month for markets, with historically significant performance across various Venn factors. In this report, we discuss market themes such as high inflation in the U.S., the weakening Japanese Yen, and continued geopolitical...

https://t.co/MZXub8ncFK

Join us for a Venn and Northern Trust Webinar on Tues, Apr 30th 11AM EST. The webinar will showcase how allocators can conduct sophisticated manager due diligence, unearth holistic multi-asset portfolio risks, and seamlessly conduct familiar workflows.

https://t.co/AmrQaRtX4q

Read today’s Institutional Investor Opinion piece where Chris Carrano questions whether PE truly offers diversification to long equity and bond markets.

Private assets are less liquid than public assets and have additional risks https://t.co/AYYVi7xVJx

https://t.co/AYYVi7xVJx

In this piece, we aim to quantify the AI hype by analyzing an AI related equity ETF, including the portion of its excess return driven by its truly unique characteristics.

https://t.co/c7jXZ0w25G