My core strength sucks and I still have difficulty holding a plank for more than 45 seconds.

So I built an app that guides me, corrects me throughout the 45 seconds and makes sure I do it right!

The repeated pothole on the road tell a story — the foundation of development is still not strong.

#mumbaigoanationalhighway

October 2025

Now there is only one question —

How many more years are we expected to keep waiting like this?

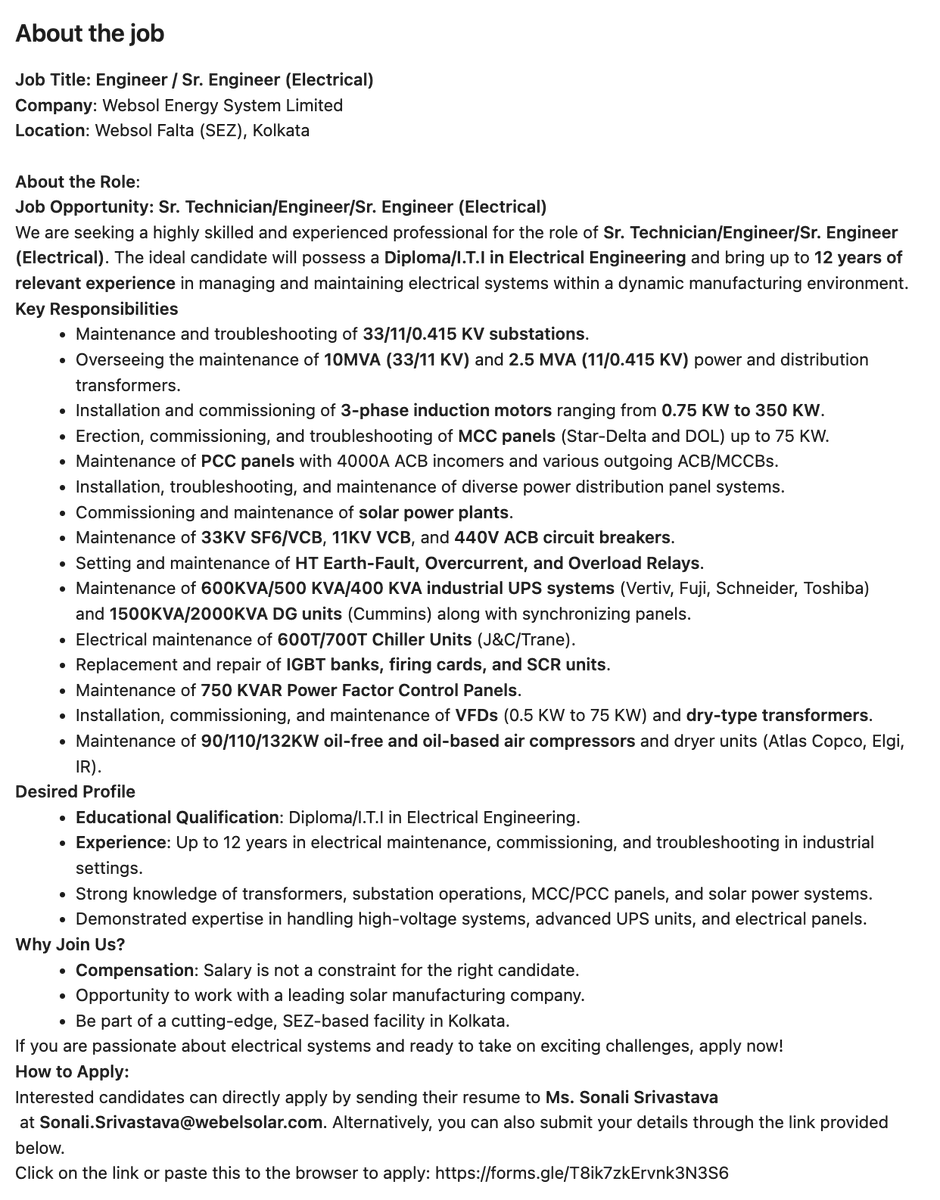

websol mgmt towards end in interview clearly said that for cell in India there is still big deficit & enough demand.

need to see the holistic picture - overcapacity in module fab capacity doesn’t mean overcapacity in whole solar value chain.

all integrated players with in-house cell mfg and later ingot/wafer mfg should continue to do well in their businesses.

discl: invested in websol & positively biased. above is opinion on business and not a recommendation to buy/sell/hold - plz do your own diligence and consider all market related research.

absolutely, websol has so far demonstrated faster commissioning & efficiency/utilization ramping up for both cell lines - full marks to their cto & tech team! hoping to see similar performance for phase 3 & 4 🤞🏼

for capex funding, considering internal accruals from fully ramped up 1.2gw cell & 0.5gw module lines, debt & equity dilution for phase 3 shouldn’t be much for its size

(given net cash inflow from operating activities post tax for h1fy26 was 132 cr from a single 0.6gw cell line plus v small module line contribution)

ingot/wafer capex may stretch the debt a bit more, depending on when they start.

once the capacity base reaches 3.2gw cell & 2.5gw module post phase3 execution, phase 4 should get funded comfortably from internal accruals along with ongoing debt reduction.

discl: invested from lower levels and positively biased. above views are for discussion & not a recommendation - do your own due diligence & consider market related risks.

what type of analyst / expert the industry has to make these kind of assumptions (in blue) and go with long caveats (in red) - kotak/bernstein did something similar earlier.

forget fy28e 113 gw, fy27e is just 15 months away which shows 98gw from 45gw in fy26e (which in itself is a farce given we are less than 20gw as of today - next 3 months 25gw!!!!)

installation, follows up commissioning with start-up, then ramp up and then stabilization - all this is time consuming process, even for experienced players!

some data:

waaree 5.4gw plant is "operational" since mar'25, latest q2 result reported 0.6gw for q2 (i.e. 2.4gw annual operational for comm production)

premier 3.2gw current capacity, q2 production was 0.5gw (i.e. 2gw annual operational for comm production)

reliance announced 10gw plant, it is nowhere even close - as of sep'25, 0.2gw hjt production was announced - but heard they are facing issues and changing the strategy to move away from hjt to topcon.

vikram has nothing and suddenly 12 gw in fy17.

fy27e numbers claimed here are impossible to achieve even in fy28...

what sort of joke are these analysts from multiple institutions running!! boss, at least have some experts who can assess and cut through the developers' announcements and say with certain confidence/probability what can and what can not be achieved!!

Save our Pink Trumpet trees & service road on EEH (Vikhroli–Ghatkopar)!

This green stretch is not just trees—it’s our morning sanctuary.

Infrastructure should not come at the cost of our health & nature.

@mybmc@mybmcWardS@mybmcWardN@MMRDAOfficial#SaveEEHTrees#GreenMumbai

SHE ACCIDENTALLY SOLVED INDIA'S ₹40,000 CRORE CRISIS AND MADE INDIA PROUD!

India grows 26 million tons of onions every year. But 40% rots before reaching people.

That's enough food for 50 million Indians. Just wasted.

Farmers relied on smell to detect spoilage. By the time they knew, it was already too late.

Every year, Kalyani Shinde’s father lost 50% of his onion harvest to spoilage.

But what she built next changed everything for millions of farmers.

So Kalyani did something no one expected.

Just a daughter who couldn’t see her father suffer anymore.

She was still a computer engineering student.

She went to Lasalgaon, Asia’s biggest onion market and built a solution.

With just ₹3 lakh in funding, she created Godaam Sense - India’s first IoT device that detects onion spoilage before it starts.

This IoT device tracks:

📌 Temperature and humidity changes in real-time

📌 Gas emissions from early-stage spoilage

📌 Sends alerts when just 1% starts rotting

Today, farmers using her device save 20–30% of their onions.

Kalyani didn’t want fame. She just wanted to protect her father’s harvest.

And in doing so, she may have solved India’s biggest storage crisis.

Post Credit: Akhil Tripathi LinkedIn (https://t.co/P82KF9hfE0)

this is good news and is in line with govt’s stated objectives & ongoing efforts to localise the whole solar supply chain ecosystem, as it will become a very large energy infra for the country at some point (already at ~100gw)

though suggested names, besides premier (who is doing cell mfg for over a decade), are bit off since the other two have no operational cell line as of now.

there are few other players in cell mfg w/ long experience, listed (websol, tatapower) & unlisted (Mundra, Jupiter etc)

@Nigel__DSouza

module & epc stories are exposed now in the market as procurement bottlenecks for solar pv cell becoming apparent to everyone.

there is no moat in the module business specially.

narrative is changing & I reckon that more institutional money will move to cell mfg companies

No recommendation for buy/sell/hold - above views are for discussion. please do your own due diligence always.

agree - so we can assume that websol has orders in place for its module lines both locally (in dcr market) as per the data shared below by TheObscureInt, and internationally as per export data shared by Investindia6 in below quoted tweet!

local dcr data I cross-checked at mnre dcr portal (https://t.co/a9SEL7WhBY). but don’t have access to export data platforms to cross-check export data, but hs code 8541.43.00 refers to modules export to US.

discl: invested & biased in websol. Above data share for information & discussion purpose - it shall not be considered as buy / sell/ hold recommendation - plz do your own diligence & cross check the data shared.

And now modules also showing in DCR - Which means modules are most likely going to be sold both in local markets and international! I feel this is big news!

Onwards and upwards to the whole websol team working hard to make India energy independent!

good time to read this below tweet again - and will give insights why pure play solar pv cell companies like websol & premier are trading near the ATH - trend should continue as this capex cycle is going to be long.

note: pure play module (without in-house solar pv cell mfg) or solar epc companies has a business bottleneck to source solar pv cell. don’t go by narratives.

Discl: invested in websol from low levels. Above is Not a recommendation - names discussed are for discussion purpose only - do your own due diligence.

websol provided the following update on its next 600 mw cell line capex:

• purchase order for machinery placed

• related advance payments done.

• mgmt has reconfirmed the timelines:

-commissioning : q1fy25-26

-commercial production: july 2025

Cheers @Investindia6 - my pleasure as always. I enjoy your updates too on dcr sales for websol among other informative stuff - thank you for constantly updating us.

indeed, market ignored it for long time, but mostly bcoz lot of people discard businesses by just looking at past numbers/ratios etc w/o rationalising it in sectoral context, and ignore the important intangibles like tech knowhow, past experience, which can become v potent instruments when the sector turns-around and start supporting. For ex, most looking at company wouldn’t have looked at background of its cto or even chairman.

lot of this ignoring was also due to narrative of last several years focussed on module fabrication, and that led us believe that cell is also a commodity and can always be imported from China since it was capital intensive & we were starting slow as a country - but any responsible govt can’t think of installing such large energy infra without securing it through building the complete ecosystem, specially when main importing source is a country that is inimical to our country’s larger interests. So there was some undermining of govt resolve as well - people thought we will survive just by importing and never reviewed solar PV cell mfg seriously.

now that govt is shifting gears on solar pv cell also, market narrative is shifting to cell and players are also finding out that just money isn’t enough to commission a solar pv cell line (waaree has been trying for last 2-3 years).

so overall there would be lot of focus on solar pv cell going forward - govt has done its job by implementing favorable policies and also many schemes like pm surya ghar yojana besides large scale projects by PSU - while private players are also gearing up with utility scale solar power plants.

by the way, demand will increase with more supply coming - India has such great potential (and to be honest more of a basic need in fact to provide cheap energy to its citizen) - I shared earlier a study by mnre+ceew which talks of 1700 gw potential - so 50-60 gw is just an intermediate number in my view, and 100 gw plus supply wouldn’t be a surprise in next decade.

as I say Future is bright 🌟, Future is solar 🌞- and websol should shine bright starting from low base but with high competence in the area they work.

Discl: holding websol since lower levels - above is shared for discussions and shall not be construed as recommendation to buy/sell/hold. Please always do your due diligence.

@RakJhun websol doesn’t import solar pv cells from China.

websol is a manufacturer of solar pv cells and is currently selling them in Indian dcr market.

no adverse impact on websol.

Usually people who talk less have better things to say.

Thanks @MeAmitMishra for adding nuance to a rather banal/sweeping generalization on the solar industry overall.

certainly true for pure play module companies and that may not even take 3 years to be treated like commodities companies.

To top that, India already has overcapacity of module mfg as compared to what we can consume today - apparent from low capacity utilization numbers of biggies in the space - they are clearly in bubble.

cell companies on other hand won’t fit in this generalization since solar pv cells are subject to technological cycles and innovation, unlike a classic commodity, and hence always command the premium - here technology continues to evolve with advancements in efficiency, durability, integration & manufacturing processes.

From govt regulations & subsidies pov for building and supporting local solar industry ecosystem. Govt has two issues at hand which they aim to solve from harnessing solar power - 1) large population with access to affordable energy to give opportunities for long term social & economic equity 2) establish India’s credentials of sustainable economy with leadership in renewables with a cheap and low risk solar energy.

People thinking that Indian govt may pull out or reduce support from solar industry just because some US related political posturing are missing these points - and intentionally or unintentionally spreading fear mongering.

Solar energy for India is a strategic energy investment for India - not only from sustainable economy side but also politically to address the election promises of free electricity etc. Geopolitically also, people should understand why Indian govt will let another energy source, which is aimed to be sizeable eventually (read mnre+ceew note shared earlier for potential solar installations upto 5600 gw), on the whims and fancies of inimical countries to support - the whole purpose of subsidies is to promote a local ecosystem to be self sufficient so that this can be supported by our own industry.

I see lot of smart money invested in pure play module companies to diversify into cell companies which are now in focus where capacity has started to build up and lot more to come in this decade. Given the specialization and capital intensive capex, there will be only 5-6 companies for cell manufacturing in India vs 100s of pure play module manufacturers.