Another round of some favorite econ/finance papers recently. In no particular order:

Renting Balance Sheet Space

https://t.co/iwnlu2hW7s

Anatomy of the 2022 Gilt Market Crisis

https://t.co/AnUTCj9tff

The Treasury Market in Spring 2020 and the Fed

https://t.co/dRXqK0Q7gP

@ben_moll Thanks! As an economist particularly interested in financial stability, I think we often over subsidize debt and my intuition is in this case it could both reduce inequality and weaken some of the amplifying linkages between collateral values and credit.

@ben_moll For addressing the "buy, borrow, and die" strategy here, would a practical solution be step-up in basis + taxing asset backed loans? The latter in principale could also have financial stability externalities. Understand this is politically unpopular, but in terms of the economics

Bernanke reflects on the Powell Fed at a Brookings event offering early retrospectives

On the wins:

-“A terrific job defending the Federal Reserve during a very, very difficult time” for Powell personally and for the institution.

-Building up political capital with extensive outreach to lawmakers

-Noting his pride in introducing press conferences, he says Powell “made them less wonky and more democratic, and more effective. That was a very important contribution.”

-Powell made the Fed “more accessible” through skilled communications

On the flubs:

-He compares the Powell Fed’s mistake in describing inflation as “transitory” to his own misjudgment labeling subprime as “contained” and suggests following up such forecasts with “if” statements; ie, we think X, but if we are wrong, we are prepared to do Y.

-He says the main real-time critiques of the transitory inflation call were right for the wrong reasons. They didn’t get the diagnosis of what drove the inflation right and that is important for calibrating the proper response to the error.

Miscellaneous:

On the size of the balance sheet and the argument for reducing the Fed’s footprint in the market: “That’s a meaningless statement.”

Turns out Trump was more interested in tariffs (his favorite word) than actually reducing the trade deficit

The fiscal deficit (federal) will be back above 6 pp of GDP this best I can tell, and standard calculations would say that explains 2 pp of the 4 pp of GDP trade deficit

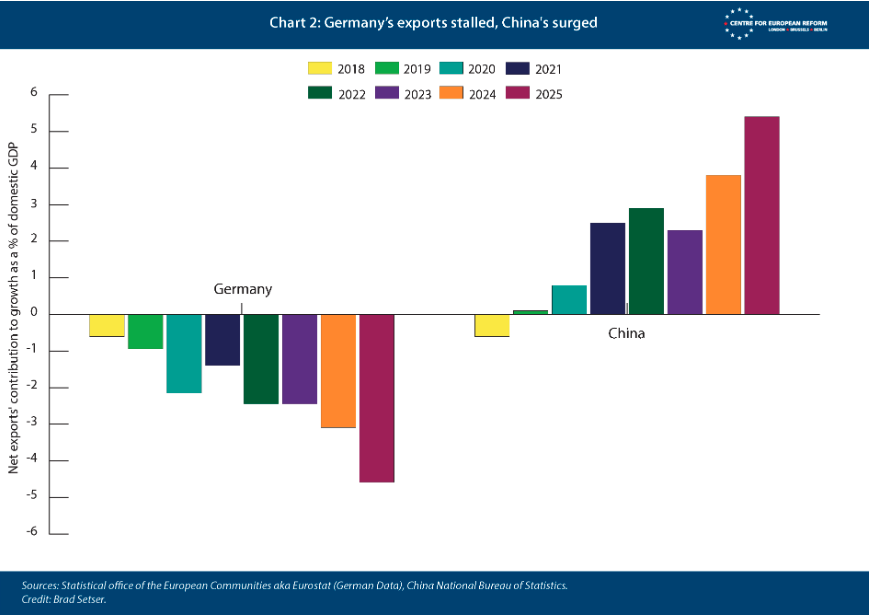

Germany is the epicentre of the China Shock 2.0 reverberating in global markets

In a new paper, @Brad_Setser and I show the shock is a key driver of Germany’s economic malaise. And it's accelerating

Berlin needs to stop admiring the problem, and join efforts to fight back

1/

I'm not extending this, but it's hilarious that people blame phones or social media for falling fertility among millennials and Gen Z. The cost of living, especially housing, is the far more plausible story.

Dettling & Kearney: a $10K rise in MSA house prices cuts fertility 2.4% among non-owners, and house prices outperform unemployment in explaining birth variation. Millennials and Gen Z are overwhelmingly renters, not owners. So this is exactly the margin that matters.

https://t.co/1vgvLlwPpi

Wenchao Li extends the result globally: surging house prices discourage fertility across countries, 1870–2012.

https://t.co/kfuvt1Xi30

This is a hawkish speech from Waller. While he doesn’t think hikes are needed in the near-term, he comes across as quite troubled by recent inflation developments. I’ll thread a few highlights:

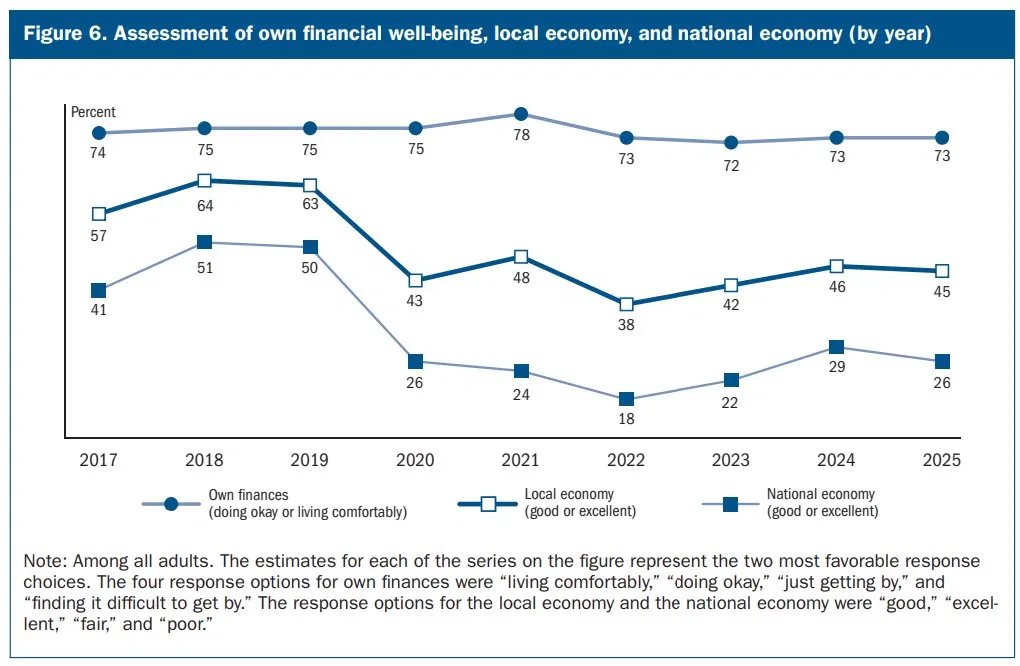

The funny thing is people rate their own economic circumstances far more favorably now than they did during the Great Recession. This lines up with the data. It's the external economy that rates poorly. Explanations that rely on people not doing well individually don't fit.

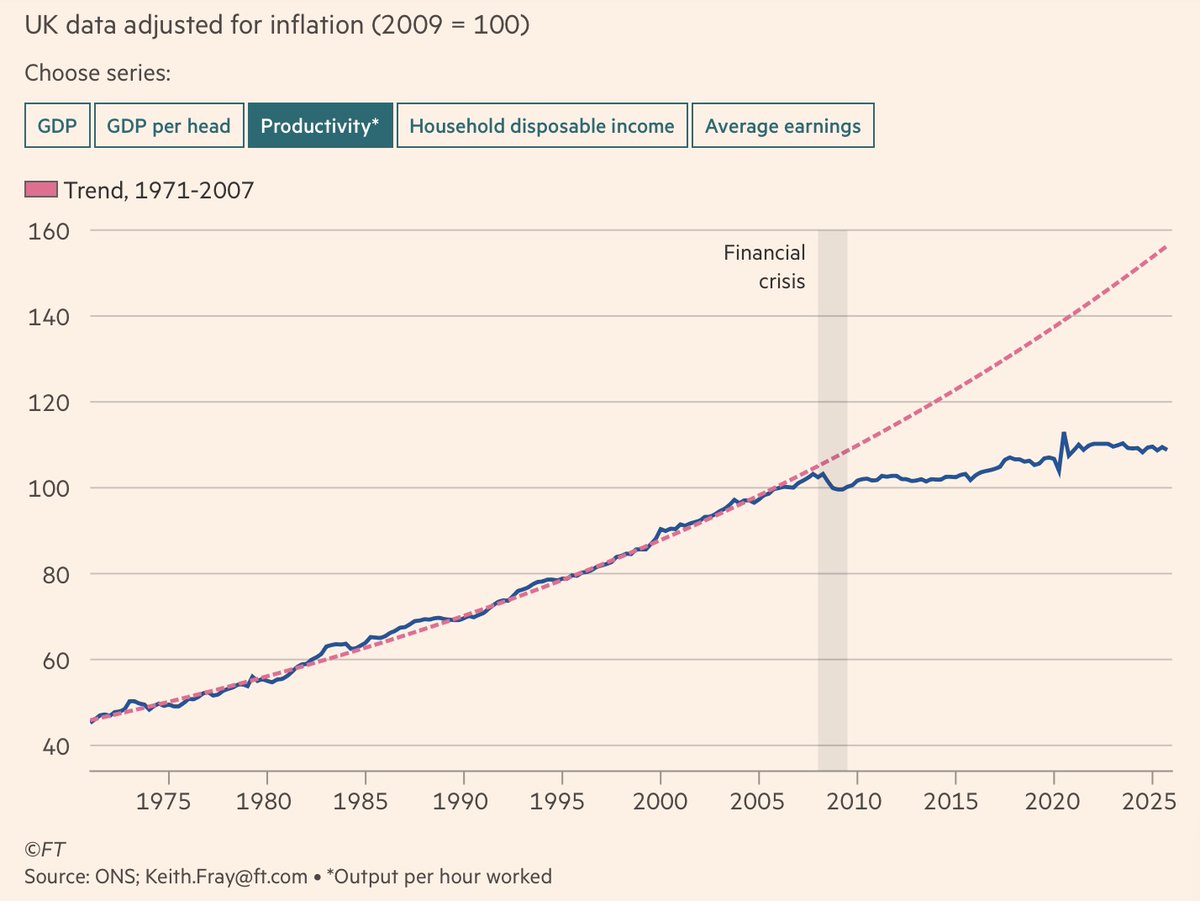

A good FT piece from Martin Wolf arguing, rightly imv, that at root of UK's political woes is a 20 yr long slowdown in productivity growth

"a good economy — one with widely shared economic growth — is a necessary condition for political stability in a liberal democracy"...