Most investors still see $MARA Marathon as a Bitcoin miner

The company now has a 2.2 GW power pipeline and exposure to the sovereign AI infrastructure market via Exaion

Power and AI sovereignty are becoming 2 of the most valuable assets in the world

Must watch for investors:

$MARA + Exaion on French national TV at Macron’s Choose France summit. Anthropic filing for French entry in the ticker crawl right above.

Coincidences?

In this market? 👀

At Choose France, President Macron's annual investment summit at Versailles, French national media turned to MARA and Exaion.

Hear from MARA CEO Fred Thiel (@fgthiel) and Exaion CEO Fatih Balyeli (@balyeli_fatih):

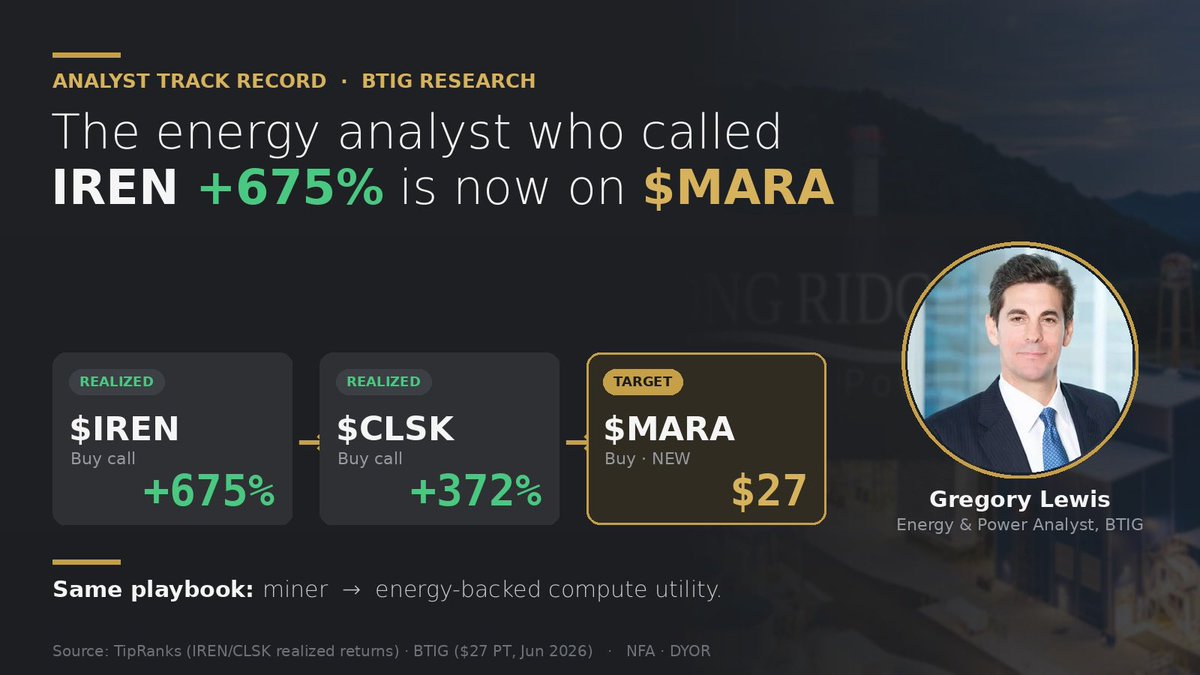

BTIG’s Gregory Lewis who covers oil tankers and power plants just put a $27 target on $MARA.

Lewis doesn’t price Bitcoin miners. He prices power assets.

Last time he made this call on a miner pivoting to compute:

$IREN — Buy → +675%

$CLSK — Buy → +372%

Same playbook. Same analyst. Same setup.

Now he’s looking at $MARA.

He sees Long Ridge a 505MW gas plant, $140M+ EBITDA and prices it for what it is:

not a miner, an energy-backed compute utility.

When the energy guy who called IREN at +675% lands on $MARA at $27…

the market’s still reading the old story.

Free optionality on every single AI deal.

Market handed this one out for free.

We must thank @MorganStanley analyst for pointing out the forgotten truth which is - $MARA bears need exactly one thing to be right:

Zero deals. Forever. Not one.

Good luck.

@TrooperTrading@MARA I was getting concerned that the AI deals for $MARA were getting priced in, but thankfully the Morgan Stanley analyst yesterday clarified that the market has completely discounted the possibility of any deals ever being signed

Rare to find a stock where big news is NOT priced in

Hi @grok I want hard predictions on $MARA. No hedging, no “it depends”.

Setup (May 2026):

(1) 1,900 MW operating, 19 data centers, 4 continents

(2) Long Ridge acquisition: 505 MW + $144M annualized EBITDA, closing H2 2026 (PJM grid, 1,600 acres in Ohio)

(3) Starwood JV: multi-GW AI infrastructure pipeline

(4) Exaion (64% of EDF subsidiary): French nuclear-powered HPC

(5) Q1 2026 earnings call: 90% of MARA’s owned sites in active tenant discussions

(5) Zero hyperscaler leases signed to date

(6) Morgan Stanley just cut PT to $7 (Underweight), valuing pipeline MWs at 10% probability of electrification

Three predictions. Commit to numbers:

1) Predict MARA’s next 3 concrete strategic moves over the next 12 months. Specific deals not “they’ll pursue diversification.” Name names. Give timelines.

2) For MARA’s first signed hyperscaler/AI lease, allocate probability across these tenants. Must total 100%:

•Microsoft / Azure ____%

•Google / Alphabet ____%

•AWS / Amazon ____%

•Meta ____%

•Oracle ____%

•xAI / Colossus ____%

•CoreWeave ____%

•Apple ____%

•Other (specify) ____%

3) Same allocation exercise, but specifically for the Long Ridge Ohio campus (505 MW, PJM, near hyperscaler-dense corridor).

Who gets those electrons?

Show your reasoning chain. Commit to the percentages. Don’t hide behind probability ranges.

Let's do the math the @MorganStanley analyst couldn't:

According to his own calculation:

$7 PT × 381.27M shares = $2.67B implied market cap.

What $MARA actually holds (per Q1 2026 SEC filing):

35,303 BTC ≈ $2.82B

Cash ≈ $80M

**Total liquid: $2.9B

Even gross of debt, Morgan Stanley's entire valuation is less than MARA's BTC stack alone.

After netting $2.3B in convertible debt (already reduced 30% via March buyback), MS still has to justify giving ZERO credit to:

*1,900 MW of operating power capacity

*19 data centers across 4 continents

*Exaion (64% of EDF subsidiary — French nuclear-powered HPC)

*Long Ridge ($1.5B acquisition adding 505 MW + $144M annualized EBITDA, closing H2 2026)

*Starwood JV (90% of MARA's owned sites in active tenant discussions per Q1 call)

Same Morgan Stanley values $CIFR operating + contracted MWs at ~$19M each.

$MARA's MWs at the $7 PT? ~$1.4M each.

~13x discount for the same physical electrons.

Different rationale: CIFR has signed hyperscaler leases. MARA hasn't yet.

Which brings us to MS's own admission.

Per MARA IR @RobSamuelsIR, quoting directly from the MS analyst's note today:

"We value pipeline MWs at a 10% chance of electrification until the partnership results in a deal."

90% written off. Before a single signature.

This is the same Morgan Stanley that told clients Bitcoin's intrinsic value could be $0 in 2017.

Today they run $MSBT the cheapest spot BTC ETF on the market at 0.14% and bought 430 BTC on launch day.

The bank long Bitcoin is underweight the equity holding 35,303 of them.

8/ Most analysts model $MARA as a Bitcoin miner pivoting to AI.

The real model: MARA is becoming what EDF is to French electricity, a global utility selling the same electron into the highest-bid compute use case at any moment.

The valuation framework for this doesn't exist yet.

1/ The $MARA story 99% of analysts are missing:

Two people are quietly orchestrating the entire tenant pipeline before any of it goes public.

One is Fred Thiel. The other will surprise you.

A thread. 🧵

7/ The market is waiting for "the big tenant headline"

The reality: tenants for the 3 anchor sites are likely already in late-stage discussions.

They just haven't been announced because the orchestration is still in motion (Long Ridge closing 2H 2026).