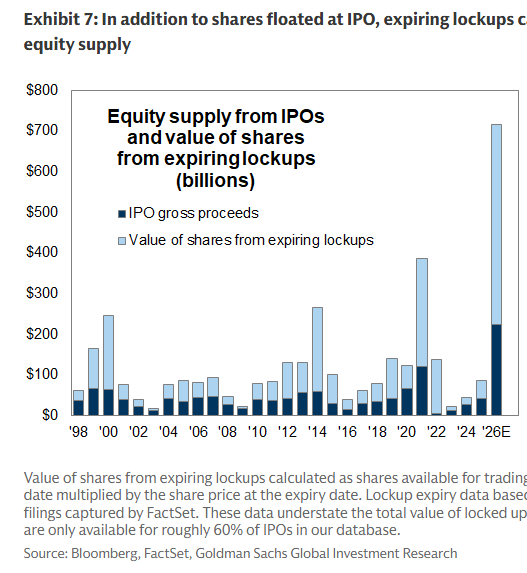

IPO issuance may not be the risk... but expiring lockups...

Based on historical patterns, we estimate that recent and upcoming IPOs will unlock roughly $500 billion in additional shares available for sale in 2026, with a likely larger amount in 2027. GS

When you go buy a Dell laptop bundle only to find out that the CPU is Intel, the RAM is Micron, the GPU is AMD, the internal Hard Drive is Seagate, the external Hard Drive is Western Digital, and they toss in a bonus SD Card that is SanDisk.

It all makes sense now...

It all makes sense.

I mapped 25 public companies across 5 sectors of the Space economy: rockets, satellites, earth observation, lunar exploration and defense.

SpaceX IPOs in weeks at $1.75 TRILLION and most people have zero exposure to the sector it's about to reprice.

🧵 Full breakdown below:

🛰️ LAUNCH & ACCESS

The foundation layer. Nothing happens in space without getting there first.

$RKLB : Rocket Lab

The one I watch most closely in this sector. Q1 2026 hit a record $200M+ in revenue with a backlog over $2.2B. Electron is one of the most reliable small launch vehicles ever built (87 launches, 83 successes). But the real catalyst is Neutron, their medium lift rocket targeting megaconstellation deployment. First launch planned late 2026. Designed to compete with Falcon 9. Peter Beck has quietly built a vertically integrated space platform: rockets, satellite buses (Photon), spacecraft components, and now aiming for human spaceflight class capability. This isn't just a launch company anymore.

$FLY : Firefly Aerospace

IPO'd August 2025. Growing 40% quarter over quarter. Designs and manufactures launch vehicles, satellites, and lunar cargo spacecraft for Artemis missions. Very early in its public life, not profitable yet, but the growth rate is hard to ignore and the government contract pipeline gives long term visibility.

SpaceX (expected $SPCX)

Not yet public but about to be. Filed S1 on May 20, 2026. Expected to list on Nasdaq around June 12. Targeting $1.75T to $2T valuation. $18.7B in 2025 revenue with Starlink alone doing $11.4B. This is not just a rocket company. It's a global internet infrastructure monopoly being built from orbit. The IPO raise could hit $40B to $80B, shattering Saudi Aramco's record. When this lists, it re rates every single company on this map.

Blue Origin (private, often paired with $BA)

Jeff Bezos' rocket company. Still private. Developing New Glenn (medium to heavy lift) and Blue Moon lunar lander for NASA's Artemis program. Now launching AST SpaceMobile's BlueBird satellites, which tells you they're becoming a serious commercial launch provider. Watch for a potential public listing down the road.

$LDOS : Leidos

The quiet giant. One of the largest US defense and IT services contractors with deep space integration capabilities. Mission systems, satellite ground infrastructure, cybersecurity for space assets. Not a pure space play but they touch nearly every government space program. The kind of name nobody talks about that keeps showing up in every contract announcement.

📡 SATELLITE COMMS

This is where revenue is scaling fastest. Connecting the planet from orbit. And personally I think this subsector is the most investable part of space right now because the business models most resemble traditional recurring revenue.

$ASTS : AST SpaceMobile

The most ambitious play on this entire map. Building the first space based cellular broadband network that connects directly to unmodified smartphones. No dish. No special hardware. Your regular phone picks up signal from satellites. Partners include AT&T, Verizon, Vodafone, Rakuten, and Google. FCC just authorized commercial SpaceMobile service in the US. BlueBird 6, the largest commercial comms array ever deployed in LEO, successfully launched. Sitting on ~$3.5B cash and over $1.2B in contracted revenue commitments. This is either a generational infrastructure buildout or the most expensive bet in telecom history. The partner list tells me it's the former.

$VSAT : Viasat. Legacy satellite broadband

Airlines, military, maritime, enterprise. Facing Starlink competitive pressure but the defense angle is the real floor here. Government contracts provide stability that pure commercial satellite plays don't have. Not the sexiest name on this list but the kind of stock that holds up when the speculative ones get cut in half.

$IRDM : Iridium Communications

Operates the only satellite constellation providing truly global voice and data coverage, including the poles. 66 cross linked LEO satellites. Critical for maritime, aviation, government, and IoT. Extremely sticky revenue, high margins, constellation fully refreshed with Iridium NEXT. One of the most underappreciated cash flow machines in the space sector. Not flashy. Just prints. If I had to own one space stock for a decade and not touch it, this would be near the top of the list.

$GSAT : Globalstar

Became a much bigger story after Apple selected them to power the iPhone Emergency SOS via satellite feature. Apple invested heavily and Globalstar is building next gen satellites to expand the partnership. The Apple relationship alone makes this a completely different risk profile than most small cap space names. Effectively a satellite infrastructure play with the most valuable company on Earth as your anchor customer.

$SATS : EchoStar / Inmarsat

Operates one of the broadest geostationary satellite fleets globally. Maritime, aviation, government, enterprise connectivity. Large legacy business generating real cash flow while positioning for next gen services. The kind of mature operator that the market ignores during hype cycles and then remembers when it wants quality.

🌍 EARTH OBS & DATA

The intelligence layer. Imaging the planet daily and turning raw pixels into actionable decisions.

$PL : Planet Labs

The largest fleet of Earth observation satellites ever deployed. Daily imaging of the entire planet's landmass. Feeds agriculture, forestry, defense, insurance, and climate monitoring. Planet is the "data layer" of the space economy. If you believe Earth observation becomes as essential as GPS (and I do), Planet is the company best positioned to own that layer at scale.

$BKSY : BlackSky Technology

Real time geospatial intelligence. The play here is AI powered analytics layered on satellite imagery. Where Planet goes wide (image everything daily), BlackSky goes deep (real time intelligence for specific targets). Heavy defense and intel community customer base. Smaller but differentiated.

$SPIR : Spire Global

Satellite powered data analytics via a constellation of nanosatellites collecting weather, maritime, and aviation data. Business model is data as a service: they sell the analytics, not the hardware. Weather forecasting, ship tracking, supply chain intelligence. Interesting because unit economics improve with every satellite added to the constellation.

$TRMB : Trimble

Positioning, modeling, and data analytics across construction, agriculture, transportation, and geospatial workflows. Not a pure space company but deeply dependent on satellite positioning systems and increasingly integrating space based data into precision applications. Massive installed base. Real earnings. The boring but profitable way to play the space data theme.

$GILT : Gilat Satellite Networks

Ground segment technology: VSATs, amplifiers, modems, and managed network services. Israeli company with deep defense relationships. Every satellite constellation needs ground infrastructure to function. Gilat builds that infrastructure. Under the radar but essential.

🌙 EXPLORATION & ON ORBIT

The frontier. Lunar missions, space manufacturing, orbital services, asteroid mining. The highest risk and highest potential upside tier on this map.

$LUNR : Intuitive Machines

This one has been on a tear. Revenue nearly tripled year over year in Q1 2026 after closing the $800M Lanteris acquisition in January. Now expanding into satellite comms, orbital data processing, and deep space networking. Participating in the Space Force Andromeda program with a $6.2B ceiling. Also acquiring Goonhilly Earth Station. Went from "cool lunar lander startup" to vertically integrated space infrastructure company in about 12 months. The acquisition strategy is aggressive but so far the revenue is backing it up.

$RDW : Redwire

Space infrastructure and on orbit manufacturing. Revenue growing nearly 60% YoY with a record backlog approaching half a billion. Makes solar arrays, structures, sensors, and is pioneering manufacturing in microgravity. If the thesis that zero gravity unlocks materials impossible to create on Earth proves out, Redwire is the picks and shovels company for that entire category.

$KTOS : Kratos Defense & Security Solutions

Unmanned systems, satellite communications ground systems, cybersecurity, and hypersonic drone development. Their space division builds command and control infrastructure for satellite operations. The intersection of space and autonomous defense systems is exactly where government budgets are accelerating fastest.

$BWXT : BWX Technologies

Nuclear technology for defense and space. Provides nuclear propulsion and power systems for NASA and DoD. Nuclear thermal propulsion is considered essential for deep space missions to Mars and beyond. If humanity goes to Mars, BWXT technology is very likely on that spacecraft. Long term thesis but anchored by near term defense nuclear revenue that makes the wait very comfortable.

$ATRO : AstroForge

The asteroid mining company. Pre revenue. High risk, true moonshot category. The thesis: asteroids contain platinum group metals worth trillions. AstroForge is building spacecraft to go extract them. Most people will dismiss this as science fiction. Fair enough. But every transformative sector had a moment where it sounded like science fiction, and the people who mapped it early were the ones who captured the asymmetry.

🛡️ DEFENSE PRIMES

The trillion dollar backbone. When governments write space checks, these are the companies cashing them. Real revenue. Real earnings. Real dividends. The stability layer of the space economy.

$LMT : Lockheed Martin

Largest defense contractor on Earth. Space division builds GPS satellites, missile defense systems, Orion spacecraft (Artemis), hypersonic systems. Won the next gen missile warning satellite program. When the US government needs something in orbit, Lockheed is usually the first call.

$NOC : Northrop Grumman

Built the James Webb Space Telescope. Makes solid rocket boosters for nearly every US launch vehicle. Operates Cygnus cargo spacecraft for ISS resupply. Deep, long duration government contracts with decades of visibility.

$RTX : RTX (formerly Raytheon Technologies)

Missile defense, radar, satellite payloads, communications systems. Pratt & Whitney builds rocket engines. Collins Aerospace provides spacecraft avionics. The merger created a space/defense conglomerate that touches virtually every program in existence.

$LHX : L3Harris Technologies

Space and airborne systems. Satellite payloads, ground terminals, electro optical sensors, communication systems for classified programs. Key contractor on the Space Development Agency's proliferated LEO constellation for missile tracking. Growing rapidly as "space as a warfighting domain" becomes official Pentagon doctrine.

$GD : General Dynamics

Submarines, combat vehicles, IT services, and space. GDIT division provides mission critical IT infrastructure for space operations, ground segment systems, and satellite data processing. Not the flashiest space exposure but deeply embedded in the classified programs that quietly fund this entire sector.

📊 THE ETF PLAY

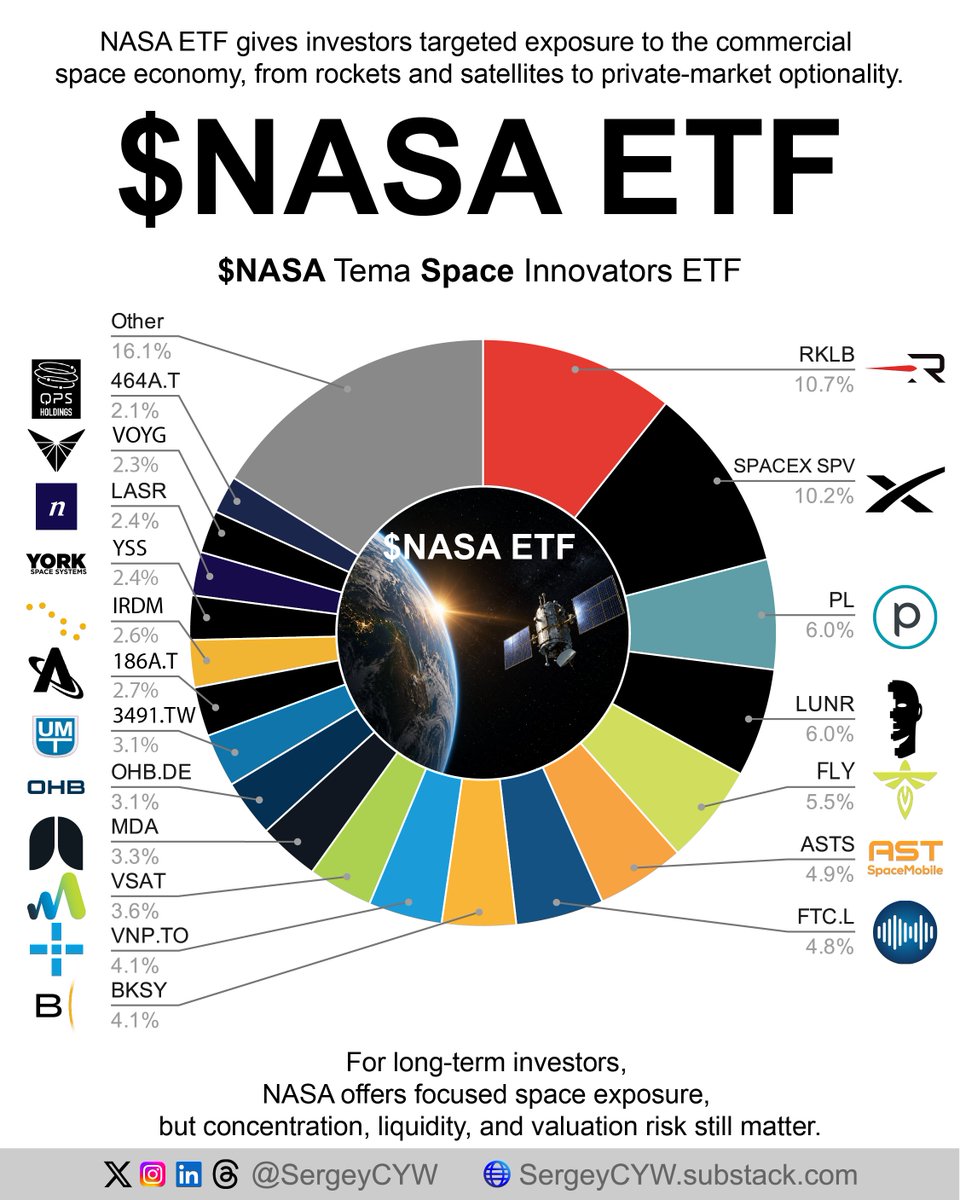

$NASA : Tema Space Innovators ETF

Launched March 31, 2026. Actively managed, 20 to 40 holdings. And the real differentiator: direct pre IPO exposure to SpaceX through an SPV, something retail investors literally cannot access anywhere else. If you want one click space economy exposure with SpaceX embedded, this is it.

🧠 FINAL THOUGHTS

Five sectors. 25 companies. The full stack of the space economy.

SpaceX targeting $1.75T+ at IPO. When it lists, it becomes the gravitational center of this entire map. Every supplier, every competitor, every adjacent company gets re rated. The Arm IPO repriced chip IP in 2023. The SpaceX IPO reprices space.

What stands out to me looking at this map:

The pure plays (Rocket Lab, AST SpaceMobile, Intuitive Machines, Redwire) are where the growth is. Revenue doubling and tripling year over year. But these carry higher risk and most are still unprofitable.

The defense primes (Lockheed, Northrop, RTX, L3Harris, General Dynamics) are where the stability is. Real earnings, dividends, and space as a growing share of revenue. Lower upside but much lower downside.

The satellite comms layer (Iridium, Globalstar, AST SpaceMobile) is where the business models are proving out fastest. Recurring subscription revenue from connectivity. This part of space most resembles a traditional business.

I'm not saying buy everything on this list. I'm saying map it. Understand the layers. Know which companies have real revenue versus aspirational roadmaps. Know where the government contracts are versus the commercial bets.

This sector is where AI stocks were before ChatGPT made everyone a believer. The difference is the space crowd hasn't had its catalyst moment yet. The SpaceX IPO might be exactly that. The people who already mapped the landscape will move first.

Data centers aren’t one trade, it’s an entire supply chain from power + cooling to chips, networking, storage, security, and the hyperscalers buying it all.

If AI demand stays real, this whole stack gets pulled higher (and volatility can be your friend if you sell premium).

Here’s the watchlist:

$VRT $ETN $CSCO $ANET $JNPR $AVGO $MRVL $CRDO $NVDA $AMD $INTC $ARM $GOOGL $AMZN $DELL $HPE $MU $WDC $NTAP $PSTG $MSFT $IBM $PANW $FTNT $DDOG $META $ORCL

$NASA ETF: The Space Economy Is Becoming Investable

The Tema Space Innovators ETF gives public investors targeted exposure to launch, satellites, lunar systems, defense space, Earth observation, and select pre-IPO holdings. It is not a broad aerospace fund. It is a concentrated space stack.

NASA launched on March 30, 2026 and trades on the NYSE. It is actively managed, with exposure to public space companies and selected private holdings. The portfolio is designed around companies with space-related revenue exposure, not generic industrial aerospace.

$RKLB Rocket Lab — 10.71%

Rocket Lab is a launch and space systems prime contractor. It builds Electron, develops Neutron, and won an $816M Space Development Agency contract to deliver 18 missile warning and tracking spacecraft.

$SPCX SpaceX SPV — 10.24%

SpaceX exposure comes through SPVs inside the ETF. The role is clear: indirect access to Falcon launch dominance and Starlink satellite connectivity before any potential public listing.

$PL Planet Labs — 6.05%

Planet operates the world’s largest commercial Earth observation fleet. Its Pelican and SuperDove satellites scan the globe daily, while AI aircraft detection and Tanager-1 hyperspectral data expand defense and intelligence use cases.

$LUNR Intuitive Machines — 5.97%

Intuitive Machines focuses on lunar infrastructure. It became the first commercial spacecraft provider to land on the Moon and holds a $180.4M NASA IM-5 award tied to an Australian rover mission.

$FLY Firefly Aerospace — 5.50%

Firefly is an end-to-end space transportation company. It builds the Alpha rocket, Blue Ghost lunar lander, and Elytra vehicles for in-space mobility, payload hosting, and defense logistics.

$ASTS AST SpaceMobile — 4.88%

AST SpaceMobile is building space-based cellular broadband for standard smartphones. Its BlueBird satellites reached peak speeds near 100 Mbps from space, and operator commitments cover roughly 3B subscribers.

$FTC.L Filtronic — 4.85%

Filtronic supplies RF, microwave, and millimeter-wave components for harsh space environments. Its E-band amplifiers and transceivers support LEO satellite links, including a major SpaceX contract.

$BKSY BlackSky — 4.07%

BlackSky provides real-time geospatial intelligence using satellites and AI analytics. Gen-3 satellites add very-high-resolution imagery, while NGA Luno contracts deepen its role in facility monitoring.

$VNP(.TO) 5N Plus — 4.06%

5N Plus supplies specialty semiconductors and performance materials for space solar cells. A 30% expansion in space solar material capacity supports satellite connectivity, observation, and defense demand.

$VSAT Viasat — 3.58%

Viasat provides secure satellite connectivity for defense, aviation, and government clients. The U.S. Space Force awarded it a Protected Tactical SATCOM contract, while ViaSat-3 F3 targets Asia-Pacific capacity.

$MDA MDA Space — 3.33%

MDA Space builds geointelligence, robotics, and mission systems. Canadarm3, the MDA AURORA satellite bus, and a $32M Canadian defense observatory contract show its position in critical space infrastructure.

$OHB(.DE) OHB — 3.15%

OHB is a European satellite systems manufacturer for LEO, GEO, defense, telecom, and Earth observation. A €280M ESA Harmony mission contract and propulsion work for CHIME and ROSE-L anchor its role.

$3491(.TW) Universal Microwave — 2.94%

Universal Microwave supplies millimeter-wave devices, filters, and ground station antenna systems. LEO satellite components for Starlink and Project Kuiper helped the segment exceed 50% of quarterly revenue.

$186A.T Astroscale — 2.71%

Astroscale targets orbital servicing and space sustainability. Its robotic spacecraft are built for debris removal, satellite inspection, and end-of-life disposal, with an $81M debris removal contract validating demand.

$IRDM Iridium — 2.60%

Iridium operates 66 cross-linked LEO satellites for pole-to-pole voice and data. Its L-band network serves maritime, aviation, government, IoT, field operations, and emergency response markets.

$YSS York Space — 2.43%

York Space is a defense and commercial satellite prime contractor. Its vertically integrated factories mass-produce standardized satellite buses, lowering cost-per-satellite and shortening production timelines.

$LASR nLIGHT — 2.39%

nLIGHT supplies high-power semiconductor and fiber lasers for aerospace and defense. Its beam control, fiber amplifiers, and 450+ patents position it inside directed energy and advanced optical systems.

$VOYG Voyager Tech — 2.34%

Voyager builds space infrastructure for orbital and deep-space missions. A 1.3 book-to-bill ratio, $45M in new bookings, and a record $275M backlog point to rising demand for specialized mission hardware.

$464A.T QPS Holdings — 2.07%

QPS develops small SAR satellites for high-resolution Earth observation in any weather, cloud cover, or darkness. A ¥370M Japanese Cabinet Office contract supports defense, disaster, and infrastructure monitoring.

The opportunity is meaningful, but risk remains high.

NASA is concentrated, thematic, and exposed to smaller names, private holdings, valuation swings, and liquidity risk. Better viewed as a satellite allocation than a core ETF replacement.

5 ETFs Dominating AI, Power, Space & Robotics

$DRAM — Invests in memory chip companies. Bets on the companies storing and moving AI data faster than ever.

$NLR — Invests in nuclear energy. Bets on uranium miners and reactors powering the AI electricity boom.

$NASA — Invests in space companies. Bets on satellites, rockets, and the businesses building the space economy.

$HUMN — Invests in robotics and AI. Bets on companies building the physical robots that will replace human labor.

$EUV — Invests in semiconductor equipment. Bets on the machines that print the world’s most advanced chips.

$SMH — Invests in semiconductors broadly. Bets on the companies designing and manufacturing the chips powering everything.

$GRID — Invests in electricity infrastructure. Bets on the companies upgrading power grids to handle surging energy demand.

THIS IS INSANE!!!🤯

Someone built a FULL stock market app…

Real-time data. TradingView charts. Auth. Persistence.

Then open-sourced the whole thing.

No subscriptions. No paywalls.

No gatekeeping.

It’s called OpenStock.

And the code is FREE.

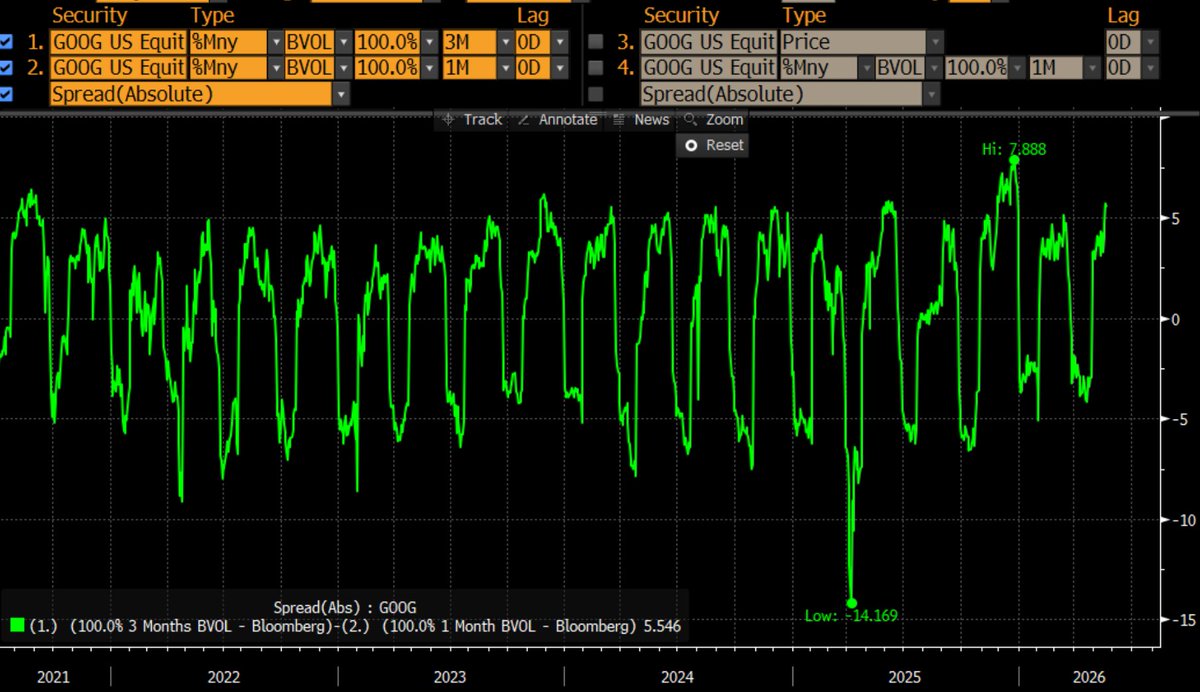

incredibly cyclical pattern of the spread between 1m and 3m implied vol on $GOOG.

once the name reports, all of the implied vol comes out of the 1m option and it then gets priced into the 3m option (which now contains the next earnings date and the vol anticipated from it).

so the spread between 1m and 3m implied vol reaches 6-7 vol points (1m 6-7 BELOW 3m).

the opposite occurs as the name is about to report. the 1m implied vol gets bid up ahead of the earnings, typically 6-7 ABOVE the 3m implied vol.

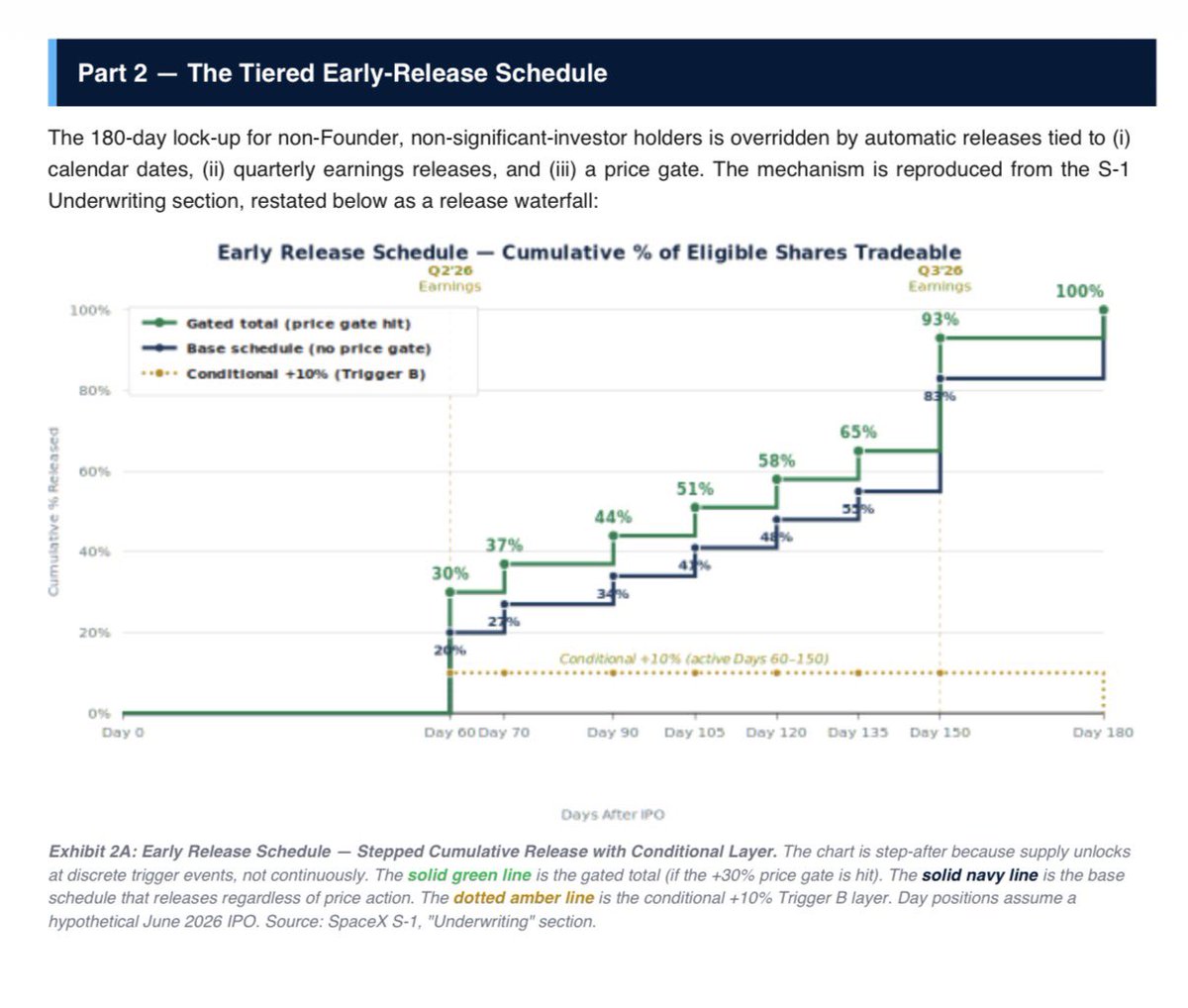

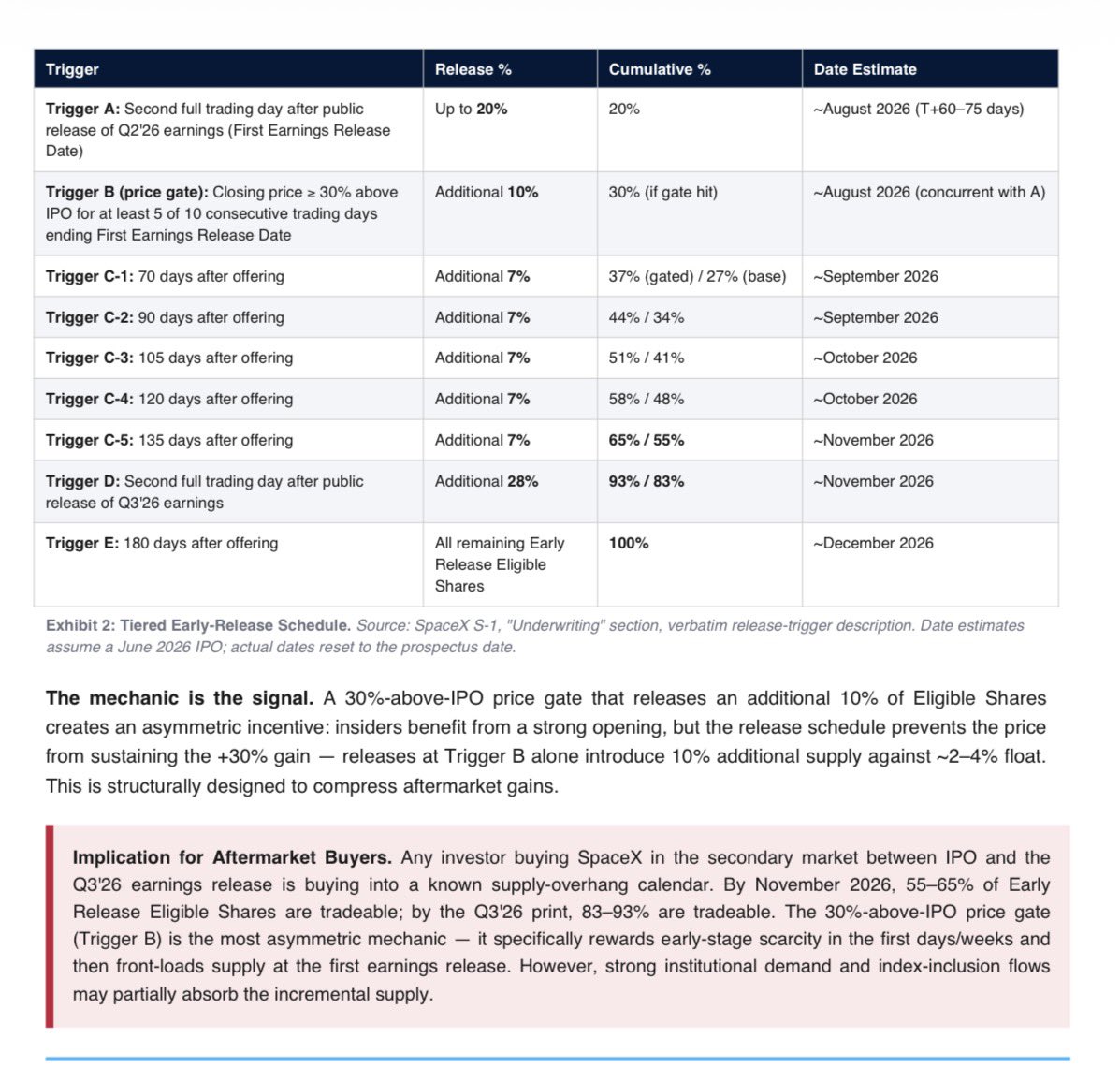

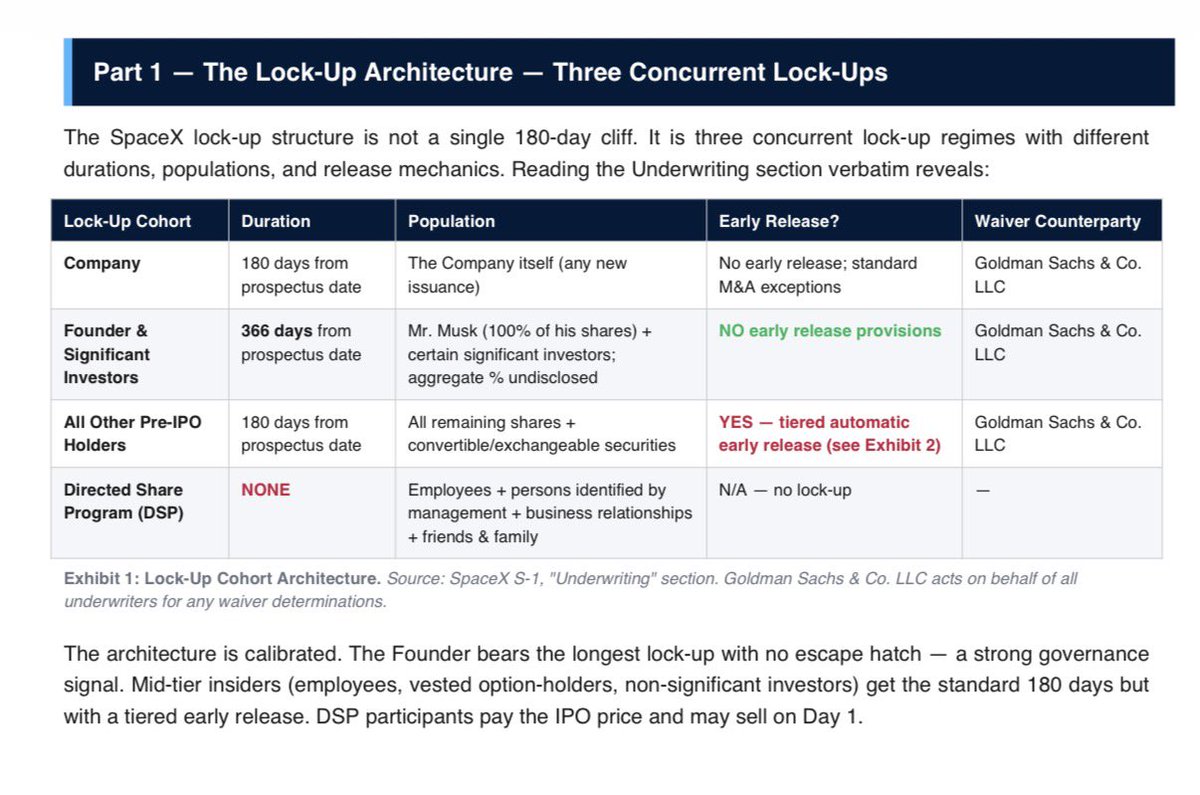

The lockup for SpaceX shares is like nothing I have ever seen.

Three groups with different lockup regimes.

The largest group has 180 day lockup after IPO, but with a graduated ability to sell based on share price at milestones before then.

instead of watching 2 hours of Netflix tonight, watch this 40-minute masterclass from the founder of a $20B China AI company

it's the clearest explanation I've seen of how Agent Swarms and AI systems actually work at scale

useful whether you've never built an agent in your life or have been using Claude every day for the past year

I took the key ideas and turned them into a practical guide on how to actually build with Kimi

find it below

10 WEBSITES THAT FEEL ILLEGAL BUT ARE 100% FREE.

Bookmark every single one. Most people will never find these on their own.

1. https://t.co/KbqhyXK8JL

Self-hosted replacement for Google Drive, Dropbox, and iCloud. Unlimited storage on your own server. Zero subscription forever.

2. https://t.co/wCipQxh4dK

Free access to 88+ million research papers that journals charge $40 each to read.

3. https://t.co/OAhaYocdxH

The world's largest open knowledge archive. Almost any book, textbook, or paper ever published.

4. https://t.co/OWjQrMcCUO

Free movies, books, software, music, and 800 billion archived web pages going back to 1996.

5. https://t.co/kUt8t60udq

Download any video or audio from YouTube, TikTok, Instagram, Twitter, and 30+ other sites. No ads. No watermarks.

6. https://t.co/qpcsBtDU0p

Full Photoshop running in your browser. Opens PSD files. 100% free forever.

7. ladder (https://t.co/svEmkUHPGm)

Self-hosted proxy that bypasses paywalls on NYT, WSJ, Bloomberg, Nature, and hundreds more.

8. https://t.co/Upx6RlFjdG

300+ free tools for PDF, image, video, and AI tasks. No signup. No limits.

9. https://t.co/0DBTEfz0fo

Replaces Dropbox, iCloud, and OneDrive. Syncs files between your devices with zero cloud and zero subscription.

10. https://t.co/EEAoCMQlxq

Installs every program you need on a new PC in one click. No bloatware. No toolbars.

The internet still has free corners. Most people just stopped looking.

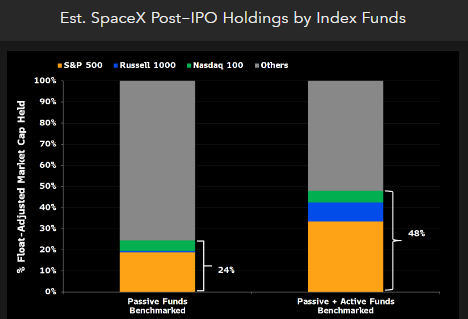

Passive S&P 500 funds could have to buy roughly 19% of public SpaceX shares within 6mo under fast-tracking framework (it would enter the index at the est 6th spot), Russell 1000 and Nasdaq 100 may buy another 5.5% within weeks of the IPO. Thrown in active MFs benchmarked to those indices and you get to HALF of SpaceX shares. Nice study from my colleague @rduboff

Those who listen will become MILLIONAIRES.

Once the AI hardware rotation slows down…

power will still need to grow exponentially.

Here’s the AI Power Super cycle that RETIRES you:

1. Layer 1 Fuel & Natural Gas Supply

(the energy feeding the AI boom)

• $EQT - largest U.S. natural gas producer

• $KMI - gas pipelines + infrastructure

• $WMB - natural gas transport + LNG

• $ET - massive U.S. energy network

2. Layer 2 Onsite / Fast Deploy Power

(the real near-term bottleneck solution)

• $BE - Bloom Energy fuel cells

• $GEV - gas turbines + power systems

• $CAT - backup generators

• $CMI - power generation systems

• $KGS - gas compression + mobile power

• $TE - solar + microgrid exposure

3. Layer 3 Grid & Electrical Infrastructure

(the hidden AI winners)

• $ETN - electrical systems

• $PWR - grid buildout

• $VRT - cooling + power management

• $HUBB - transformers + grid equipment

• $NVT - electrical infrastructure

• $EMR - industrial power systems

4. Layer 4 Nuclear & Long-Term Baseload

(the future AI power source)

• $OKLO - advanced nuclear

• $SMR - small modular reactors

• $NNE - portable microreactors

• $CEG - largest U.S. nuclear fleet

• $VST - nuclear + power generation

• $BWXT - reactor components + services

Here is how it breaks down.

AI models get larger. Data centers get bigger.

Energy demand keeps accelerating.