Microsoft $MSFT and Chevron $CVX just signed a 20-year deal to power a massive West Texas data center with natural gas. This could be one of the largest data centers in the US 🇺🇸 - Bloomberg

$NVDA CLARIFIED RUBIN GPU RAMP-UP SCHEDULE AND IMPLICATIONS FOR DEPRECIATION LIFECYCLES

Updates regarding the Rubin GPU timeline and legacy product utilization provide clarity on future supply and depreciation dynamics.

🗓️ CLARIFICATION OF PRODUCTION TIMELINE

Management has explicitly defined the mass production schedule for the Rubin GPU following a series of updates.

→ The company initially mentioned a vague production plan for next year during its 2Q25 earnings call.

→ A subsequent meeting with JPM revealed the completion of the TSMC tape-out and targeted a 2H26 ramp-up.

→ The 3Q25 earnings call reinforced this timeline, confirming mass production will commence in the second half of 2026.

📉 UTILIZATION AND DEPRECIATION IMPACT

Legacy A100 GPUs are running at maximum utilization, defying concerns about rapid obsolescence in the hardware cycle.

This high usage rate serves as a counterargument to fears surrounding aggressive depreciation lifecycles.

The rapid two-year GPU development cycle typically implies a shorter useful life for hardware assets.

However, the expanding AI inference market generates robust demand for older models, extending their operational relevance.

This structural shift will likely loosen the current tight restrictions on depreciation cost management.

Good report on Corning

(They don't cover the tech part so I will do it here)

- Corning’s Vapor Axial Deposition produces the world’s lowest-attenuation silica glass (~0.15 dB/km), reducing signal loss over long interconnects

- ClearCurve (Bend Insensitive Fiber) allows 10 mm bend radius routing inside dense AI racks without optical degradation.

- RocketRibbon (high density cable architecture) supports 3,456 fibers per cable, enabling compact, high-bandwidth backbones within constrained spaces

- EDGE (Low loss connectors) with 0.2 dB typical insertion loss ensure signal integrity across thousands of parallel connections.

AppLovin just wrapped up their talk at the GS Communacopia + Technology Conf - Here are some notes from the $APP live stream. Follow this thread - I'm putting my initial takes up here now ...(1/x) 🧵Feel free to share this...Let's go 💰💰 #AppLovin

China's National Data Administration reports daily AI token consumption has increased over 300-fold in 18 months, signaling rapid growth in its AI applications.

- China's daily token consumption surpassed 30 trillion by the end of June.

- This rapid rise reflects the quickly expanding scale of AI applications within the country.

- Daily token consumption was 100 billion at the start of 2024.

→ It reached over 30 trillion by the end of June 2024.

"Your margin is our opportunity" - $AMZN is using its first-party purchase data to build a programmatic ad platform that's eating The Trade Desk's lunch.

It's strategically undercutting $TTD by charging a take rate as low as 1% compared to TTD's 7%.

Applovin for the first time commanded 4% of total ad spend in August according to @northbeam. This is with just 600 customers. I expect them to hit a much higher share in H1 2026 inshaAllah. $APP

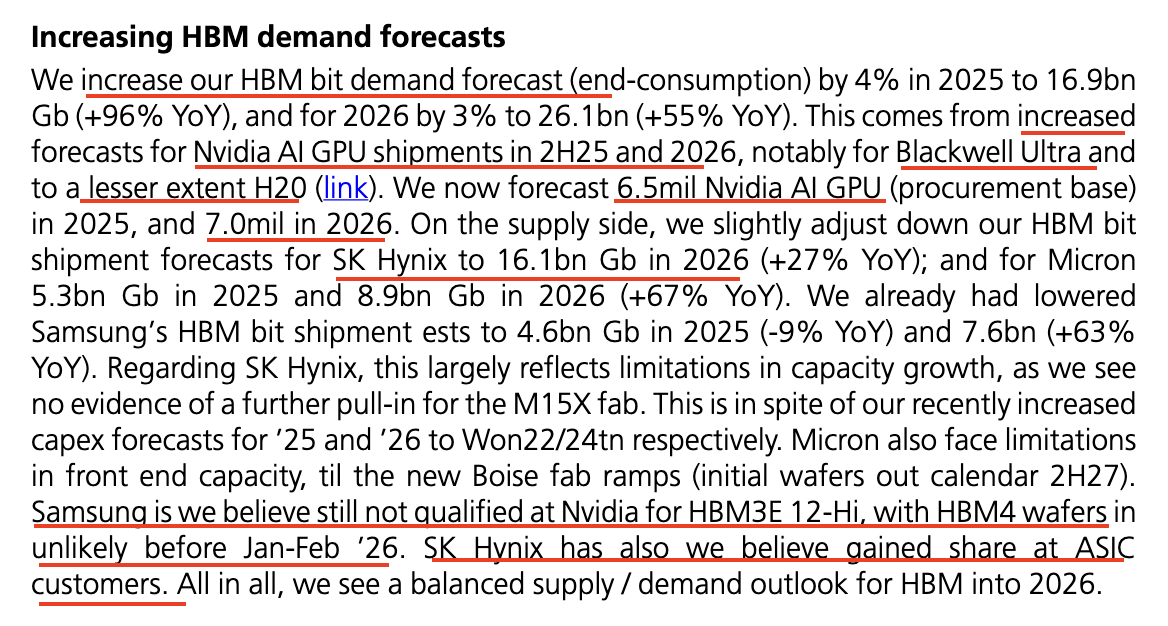

UBS on HBM. Few points (I agree couple points below).

1) Increased HBM bit demand forecast by 4% in 2025 and 3% in 2026.

2) Raised forecast of $NVDA GPU to 6.5M in 2025 and 7M in 2026

3) Samsung is still not qualified at $NVDA HBM3E 12hi, with HBM4 wafers in unlikely before Jan-Feb 26'

4) SK Hynix has also gained share at ASIC customers.

$WBTN SURGES ON STRONG Q2 RESULTS AND DISNEY PARTNERSHIP

🤝 DISNEY PARTNERSHIP LEVERAGES MUTUAL STRENGTHS

- Disney's Marvel and Star Wars content will be adapted for $WBTN's mobile-optimized vertical format.

- Disney's Marvel Unlimited app, less suited for mobile, will benefit from improved readability and MAU growth.

- $WBTN gains premium content; Disney taps the top US comics app's marketing power.

- Favorable revenue-sharing terms are expected.

- A major marketing campaign is set for New York Comic Con in October.

UBS raised its HBM demand forecasts through 2026, citing stronger Nvidia AI GPU shipments.

1) 📈 DEMAND RISES ON HIGHER NVIDIA GPU PROJECTIONS

- UBS increased its 2025 HBM demand forecast by 4% to 169B Gb, a 96% YoY rise.

- The 2026 forecast rose 3% to 261B Gb, reflecting 55% YoY growth.

- Higher Nvidia AI GPU shipments in H2 2025 and 2026 drive this revision.

- Growth is mainly due to the Blackwell Ultra GPU and H20 model.

- UBS projects 6.5M Nvidia AI GPU shipments in 2025 and 7.0M in 2026.

2) ⚙️ SUPPLIER OUTLOOKS LIMITED BY PRODUCTION

- UBS lowered SK Hynix’s 2026 HBM bit shipment forecast to 161B Gb (+27% YoY) due to M15X fab capacity limits.

- No early production ramp-up is evident.

- This persists despite capex forecast increases to ₩22T and ₩24T.

- Micron faces front-end capacity constraints until its Boise fab starts in H2 2027.

- Micron’s HBM shipments are projected at 53B Gb in 2025 and 89B Gb in 2026 (+67% YoY).

- Samsung lacks Nvidia’s HBM3E 12-Hi certification.

- HBM4 mass production is unlikely before January or February 2026.

- UBS forecasts Samsung at 46B Gb in 2025 and 76B Gb in 2026.

3) ⚖️ MARKET TO BALANCE AS SK HYNIX GAINS ASIC SHARE

- SK Hynix has expanded its ASIC customer market share.

- UBS projects a balanced HBM supply/demand outlook through 2026.

Markets are now pricing in over 100bp of US rate cuts for the next 12 months.

This implies total rate reductions will exceed 200bp since September 2024.

JP Morgan's analysis highlights two trends shaping the global gas turbine market.

📈 GLOBAL DEMAND SURGES, LED BY US AND MIDDLE EAST

- Global gas turbine orders hit 41.8 GW in H1 2025, up 37% year-over-year. Q2 orders were 21.4 GW, a 28% rise.

- Turbines over 10 MW grew 36% to 41.7 GW in H1.

- Orders for industrial turbines under 100 MW nearly doubled in H1, with Q2 growth estimated at 140%.

- North America and the Middle East accounted for 68% of H1 orders. US demand surged over 400% to 17.8 GW from 3.4 GW.

- Orders elsewhere dropped 20% to 13.4 GW due to higher turbine prices and limited gas supplies.

🏆 1) SIEMENS ENERGY LEADS AS SMALL TURBINES GAIN TRACTION

- Top three manufacturers hold 89% of the gas turbine market.

- Siemens Energy's market share rose to 40% from 29% in H1; GE Vernova's fell to 27% from 35%, and Mitsubishi Heavy Industries' dropped to 22% from 25%.

- Small industrial turbines, favored by data centers, have a median lead time one year shorter than larger units, currently just over two years.

- Small turbines suit backup power for grid-connected data centers, aiding faster grid connections. Large turbines are preferred by hyperscalers building power plants.

- Siemens Energy's Q3 margin hit 13.0%, beating the 11.8% consensus, with the US driving half of new orders (14 GW, 65% for data centers). Its order backlog grew to 58 GW from 50 GW.

- Siemens Energy plans a 10% capacity increase for small turbines next year and a 25-30% expansion for large turbines by 2028.

⚙️ 2) MARKET SEGMENTATION AND TECHNOLOGY

- Turbines under 100 MW, called "industrial turbines," serve process industries with lower efficiency in simple-cycle operation.

- This segment includes fast-starting "aeroderivative" turbines used as backup when renewables falter.

- Turbines above 100 MW, known as "heavy-duty," are used for baseload power - divided into E-class, F-class, and advanced-class.

- Advanced-class turbines, the largest and most efficient at ~65%, typically operate in combined-cycle setups.

- E-class and F-class turbines, older technologies, can be serviced by third parties, while advanced-class turbine servicing is OEM-exclusive.

Two key updates on $BE data center market expansion:

https://t.co/b11r1UCiB8

1. BLOOM ENERGY NEGOTIATES NEW POWER DEALS

- $BE CEO KR Sridhar announced negotiations with major data-center developers.

- New deals similar to its Oracle agreement are expected soon.

- Following a July deal, Bloom will use fuel cells to power Oracle’s AI facilities, though the deal's size was not disclosed.

2. COMPANY PLANS SIGNIFICANT CAPACITY GROWTH

- Bloom Energy provides over 0.5 gigawatts to data centers, with total installed capacity exceeding 1 gigawatt.

- The company aims for 2 gigawatts by next year’s end.