@ChomeurContent@NewLeftEViews Not really. It's mainly been paid for through cuts and (now) tax raises. In fact Russia's economic bureaucracy has a very un-Keynesian approach and the war hasn't really changed that. There is a whole group of pro-war economists complaining about the lack of economic mobilisation

@NewLeftEViews Plus namedropping every famous Russian his readers would know (Berezovsky, Kasparov etc). Even the writing is just standard middle-brow French prose. Quite embarrassing how much of the French (and now, it seems, EU) upper crust fell for it.

@NewLeftEViews Haven't read his nonfiction but Wizard of the Kremlin is total trash. It's a repeat of Surkov's PR machine's output (he was doing the dark Machiavellian super advisor trope before anyone in the West) with some lazy tropes (beautiful women, Russian soul) mixed in.

@TiltingatM3 Do you know what the difference is between this dataset and the net profit rate one Briley & Renner use? Was coincidentally just reading their NLR reply and they rely heavily on that to tell a story that would kind of fall apart if you use this data instead

@TiltingatM3 Best places to start imo are McNamara, The Currency of Ideas and Schelkle, The Political Economy of Monetary Solidarity. On the politics and constitutional aspects of the creation of the EMU there is a lot of detail in Dyson and Featherstone, The Road to Maastricht.

@benbawan@GlennLuk Exactly. The borders matter in a way that they don't btw Chinese provinces, and so do the external imbalances between EU members.

I do agree that if you're looking at it globally you can gloss it as EZ vs China vs US. But the German surplus is still relevant esp at the EU level

@GlennLuk@benbawan My point is that despite its being part of a broader economic union, its surpluses still matter. They have had a rather destructive effect on many southern members of this union precisely because they shared the same currency but other aspects of economic policy were not unified.

@GlennLuk@benbawan This is a bad comparison. Yes the EU is economically unified to a certain degree, but Guangdong cannot experience a current account crisis or a sudden stop. It is also part of a larger polity with centralised fiscal policy. Something like the euro crisis could not happen in China

@SanderTordoir Simplification is a magic bullet for those (especially in Germany) ideologically convinced that economic stimulus is always wrong and that debt brakes were a great civilisational achievement. Plus it's always a moving target so it's even more convenient politically.

@NewLeftEViews@narbi16@Brad_Setser Thanks for the clarification! So I suppose WEO uses the customs data and IFS uses the BoP data. (Although interestingly the size of the surplus is almost the same in both series)

I did hear about the factoryless adjustments, but was also lazy and didn't look into the details...

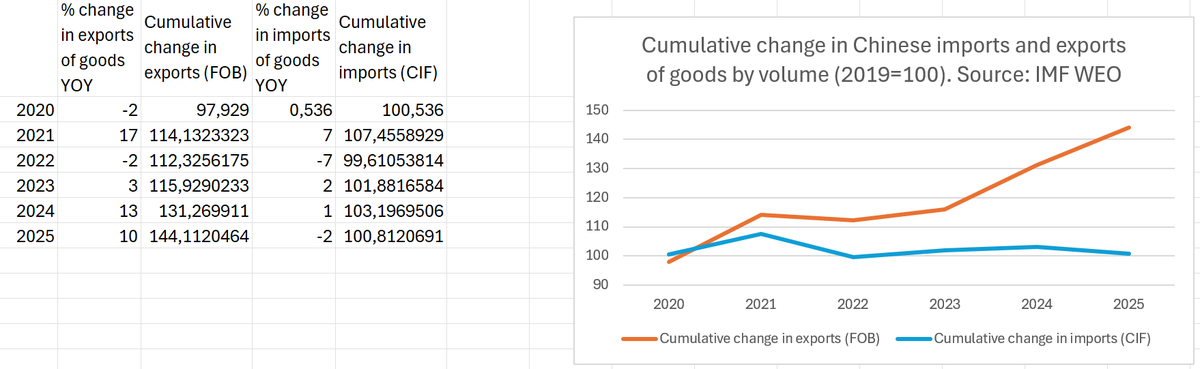

@narbi16@NewLeftEViews@Brad_Setser Seems like IFS has a bigger increase in both import and export volumes. In both series the difference btw the cumulative change in exports vs imports is about 28-29 percentage points by 2024 (no 2025 data yet from IFS).

@narbi16@NewLeftEViews@Brad_Setser Seems to be the WEO data, I was able to reproduce it. I don't know what the differences between those two series are though.