We (@fund_defi) submitted a letter in response to the SEC’s RFI asking for thoughts on "exchanges" and crypto ATSs. TL;DR: don't misclassify DeFi technology and devs that aren't actually performing "exchange" functions.

We urge the Commission to:

1️⃣ Adopt a functional test for an exchange "facility” so only those actually performing exchange functions are in scope, and not disintermediated software, AMMs, smart contracts, or developers.

2️⃣ Avoid an overly broad reading of a “group of persons" constituting an "exchange." Where there’s no shared intent or control over exchange functions, developers/entities shouldn’t be treated as an exchange just because their software is used by one.

Bottom line: DeFi tools that provide liquidity or run autonomously aren’t performing exchange functions and neither the tech nor its devs should be regulated as exchanges.

Full letter: https://t.co/NMYpFoWxho

"... we cannot erode more on developer protections if we really want to bring developers back onshore," says @RebeccaRettig1 on @CoinDesk's new show, The Policy Protocol.

"If we want to real innovation, and real builders, and people feeling safe building onshore, we have to make sure that the bill that passes and gets signed by President Trump really does protect software developers."

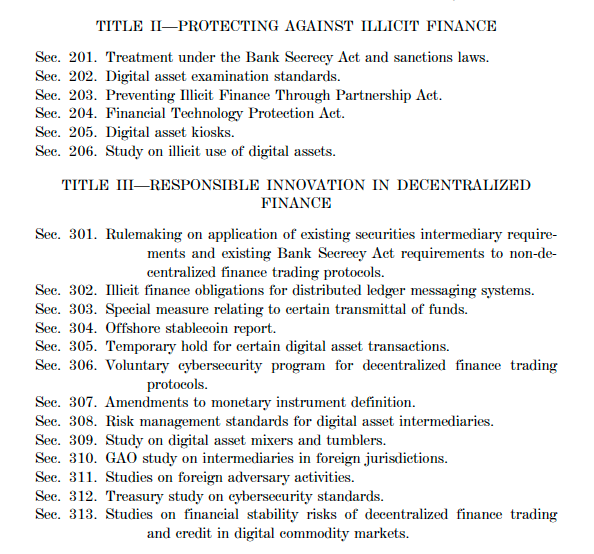

Clarity Act Title III ("Responsible Innovation in Decentralized Finance") was added to the Clarity Act to address concerns related to illicit finance and digital assets. It did not exist in the September draft. It was specifically added in response to concerns raised by prosecutors/law enforcement, to provide even more tools than were already in Title II ("Protecting Against Illicit Finance").

Anyone saying this bill does not give enough tools or runway for law enforcement to go after bad actors should *actually read* read Title II or Title III.

Powerful statement from @SECPaulSAtkins today. In his remarks, the Chairman explains that "our existing framework" does not always organize "neatly" to today's onchain markets. AND, he commits to providing a future-proof framework to clarify how existing regulatory definitions apply to technologies spanning the decentralization spectrum.

"But software applications today do not always organize themselves neatly along these categorical lines. A single protocol can execute a trade, manage collateral, route liquidity, execute trading strategies through vault structures, and settle the transaction—all within a unified, automated system, often within seconds."

The DEF team, in particular, appreciates that Chair Atkins highlights that DeFi *is* unique and requires different treatment from TradFi:

"As the Commission considers these policy initiatives, we should remember that onchain market structures today are often hybrid in nature, combining elements of what are often referred to as “traditional” and “decentralized” finance. We should clarify how the Commission views the spectrum of models that may implicate our statutes through notice and comment rulemaking, using our exemptive authorities where necessary and prudent, all with full participation from innovators, investors, and the public alike."

New op-ed from Democratic Sacramento District Attorney @ThienHoCA on why software developer protections are an essential component to the next era of financial innovation in the United States. More importantly, he explains that as a prosecutor, Section 1960 has been stretched beyond its intended scope to target developers of non-custodial, p2p software.

He writes, "Neither the developers nor the software itself controls other people's funds or transfers funds on their behalf. Charging them under a statute built for traditional financial intermediaries is a mistake, because it is misinformed and misdirected."

"This approach chills open-source innovation, pushing many U.S. developers offshore. This unfairly saddles some with a criminal conviction and erodes American technological leadership in an area of consequential financial innovation."

That's why we need clear developer protections in crypto market structure legislation.

https://t.co/dpqRyQISDu

Completely Agree. DeFi technology should NEVER be subject to the BSA. The BSA is a broken and ineffective regime that is incompatible with decentralized systems.

@fund_defi wrote about this in Feb 2025. The ineffectiveness of the BSA warrants a thoughtful discussion on future improvements.

The problem with the BSA is nuanced but significant: (1) it is overly burdensome and costly, (2) it has demonstrated minimal success in achieving its key objectives through transaction reporting, review, and investigation, and (3) it creates harmful downstream effects, including arbitrary enforcement, prohibitive compliance costs, and centralization.

The inefficiencies and burdens of the AML system highlight the challenges that would arise if DeFi were subjected to the framework.

https://t.co/zU8mAaFvdr

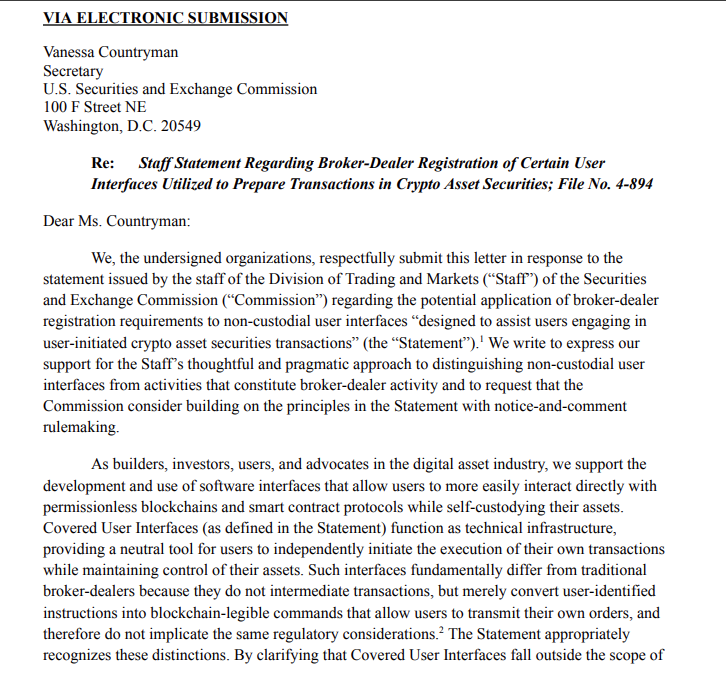

The SEC took an important step on UIs - and now we’re asking them to lock it in.

On April 13, 2026, the SEC published a staff statement with a thoughtful, practical approach for distinguishing non-custodial user interfaces from activities that constitute broker-dealer activity.

DEF and 35 industry leaders are now requesting the SEC formalize the principles in the statement in notice-and-comment rulemaking, so we have durable regulatory clarity that lasts.

Walking & listening to @TechnicallyLgl, featuring DEF’s Senior Counsel @_ayanadow.

Get to know one of our favorite lawyers, and how she thinks about:

➡️ correlations between crypto policy & playing tennis

➡️ why this is a Dodd-Frank moment for crypto lawyers

➡️ crypto as a tool for financial inclusion

Imagine writing multiple letters insisting tx-based comp is dispositive…

And the SEC says it’s just one factor of the broker-dealer analysis.

Tough day for the gatekeepers and the moat protectors. Good day for builders.

Thrilled to be part of a team that pairs deep @CFTC expertise with private-sector experience ranging from major law firms, @BlockchainAssn & @fund_defi.

Legacy market infrastructure is slow, expensive, and inaccessible. Moving onchain solves these problems.

But capturing that opportunity depends on clear rules for the blockchain apps that enable investors to trade peer-to-peer, without rent-seeking middlemen. The @a16zcrypto and @fund_defi safe harbor proposal for DeFi apps would accomplish exactly that.

Today, former SEC Chief Economist and Director of the Division of Economic and Risk Analysis Craig Lewis submitted an economic analysis of that proposal to the Commission.

Though scoped to the proposal itself, Lewis' analysis speaks to something larger: the economic costs and benefits of tokenized securities broadly, and what blockchain technology could mean for the future of financial markets.

His bottom line: there are real costs, but the overall economic case is compelling and the proposal offers a sound path forward.

We (@fund_defi) submitted a letter in response to the SEC’s RFI asking for thoughts on "exchanges" and crypto ATSs. TL;DR: don't misclassify DeFi technology and devs that aren't actually performing "exchange" functions.

We urge the Commission to:

1️⃣ Adopt a functional test for an exchange "facility” so only those actually performing exchange functions are in scope, and not disintermediated software, AMMs, smart contracts, or developers.

2️⃣ Avoid an overly broad reading of a “group of persons" constituting an "exchange." Where there’s no shared intent or control over exchange functions, developers/entities shouldn’t be treated as an exchange just because their software is used by one.

Bottom line: DeFi tools that provide liquidity or run autonomously aren’t performing exchange functions and neither the tech nor its devs should be regulated as exchanges.

Full letter: https://t.co/NMYpFoWxho

Another big win for @Uniswap and @haydenzadams today.

The court dismissed all claims in the Risley class action with prejudice, reaffirming the core principle that a developer isn’t liable for third-party misconduct simply because it built neutral infrastructure others used to do bad things.

Read the whole opinion here

https://t.co/HXHkqe85yA

Today, SPI together with @fund_defi, submitted a letter to Commissioner @HesterPeirce and the @SECGov Crypto Task Force providing context on non-custodial wallets and neutral user interfaces.

Recent submissions have inadvertently conflated different technologies and overlooked key legal precedents. Our letter aims to ensure policymakers have accurate information as they develop a coherent regulatory framework.

Read the full submission: https://t.co/MUwwNX47zr

[NEW] Today, the DEF team published a myth vs. fact resource on the Blockchain Regulatory Certainty Act

The BRCA is good policy, and its inclusion in market structure is a red line for the industry for good reason.

Below: we debunk common misconceptions about the BRCA. 👇

4/ Effective regulation must recognize the real differences between CeFi and DeFi technologies, avoid entrenching particular technical solutions, and ensure rules are workable in practice. Read our full comment letter here: https://t.co/NeWRidNwv8

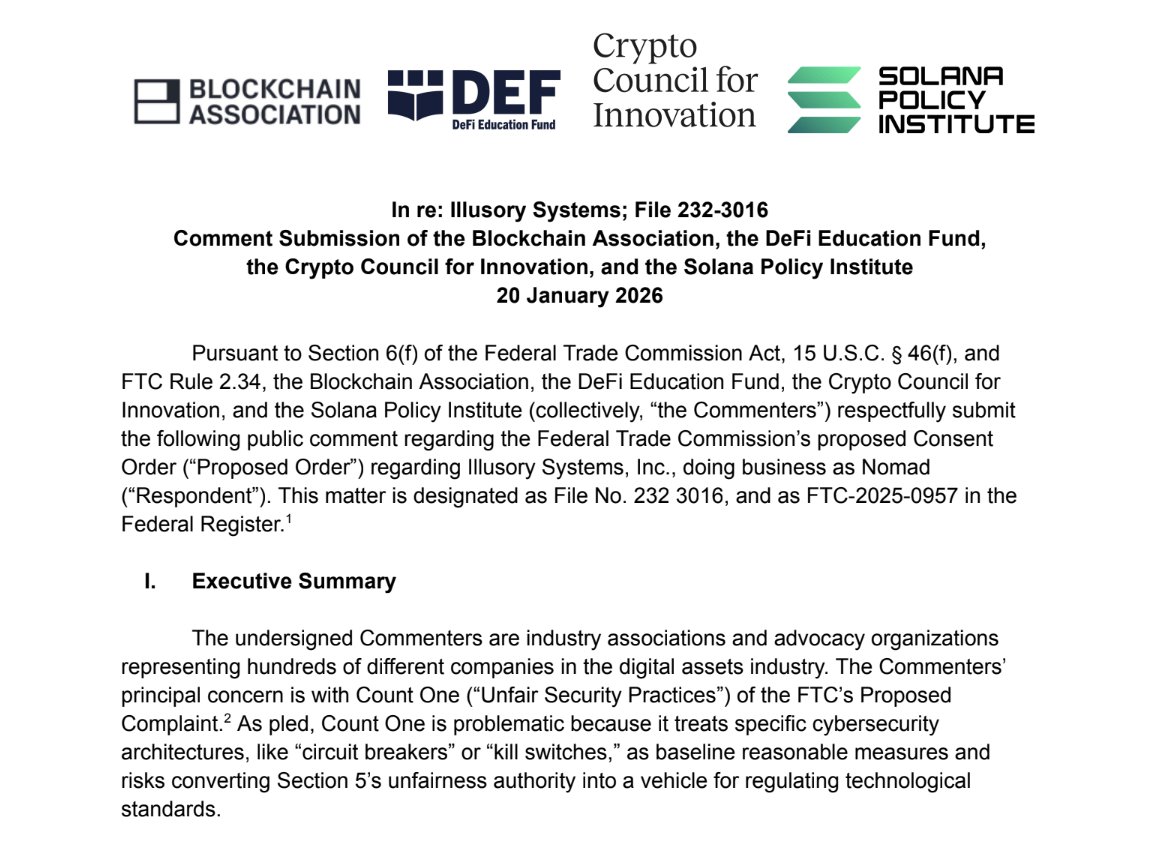

1/ @fund_defi joined @BlockchainAssn, @crypto_council, and @SolanaInstitute in submitting comments to the @FTC on its proposed order related to Nomad/Illusory Systems Inc. While we share the FTC’s consumer protection goals, the proposed order suggests that crypto systems must use "circuit breakers" and "kill switches" – calling this a "widely-accepted industry norm."

Why it matters: Not all crypto systems are designed the same way, and mandating technical solutions such as centralized controls would stifle DeFi innovation.

3/ Our comment letter requests that the FTC remove Count One or significantly revise it to avoid mandating specific technical architectures. We highlight that using “unfairness” authority to impose specific technical requirements turns the FTC into a de facto standard-setting body for engineering controls, without statutory authority. Importantly, Congress is actively working on comprehensive digital asset legislation. The FTC should not preempt these legislative efforts through enforcement settlements.

![fund_defi's tweet photo. [NEW] Today, the DEF team published a myth vs. fact resource on the Blockchain Regulatory Certainty Act

The BRCA is good policy, and its inclusion in market structure is a red line for the industry for good reason.

Below: we debunk common misconceptions about the BRCA. 👇 https://t.co/HxSariz2TG](https://pbs.twimg.com/media/G_OTQgDXIAAHEOx.jpg)