Added marginal African #lithium projects for a rough estimate of their contribution to global supply.

During H1 '24, projects that have since become borderline maybe delivered 20-24% of all lithium going into batteries (EV, BESS, mobility, consumer electr)??

Any obvious errors?

If this is not good news for #lithium, what is?

#Honda will reduce China's annual gasoline production capacity to 1.2, vehicles, while accelerating the transition to electrification.

China 97%.

Incredible.

“The share of European consumers who said their next vehicle will be all-electric has not changed over the past 3 years at 43%.

Chinese buyers answering the same question positively, meanwhile, rose to 97 percent” https://t.co/CxDYOjRZV0

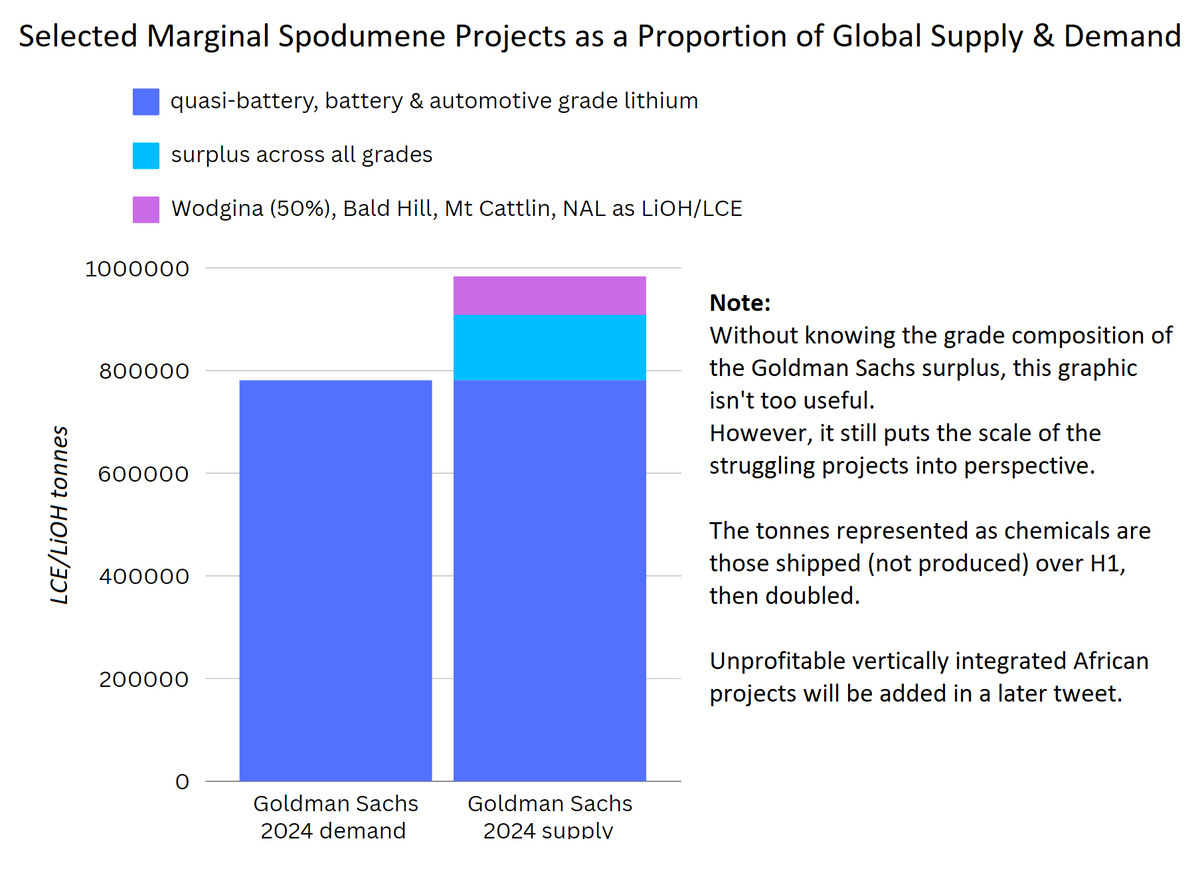

Spodumene projects that are currently borderline or unprofitable, and their contribution to global supply & demand.

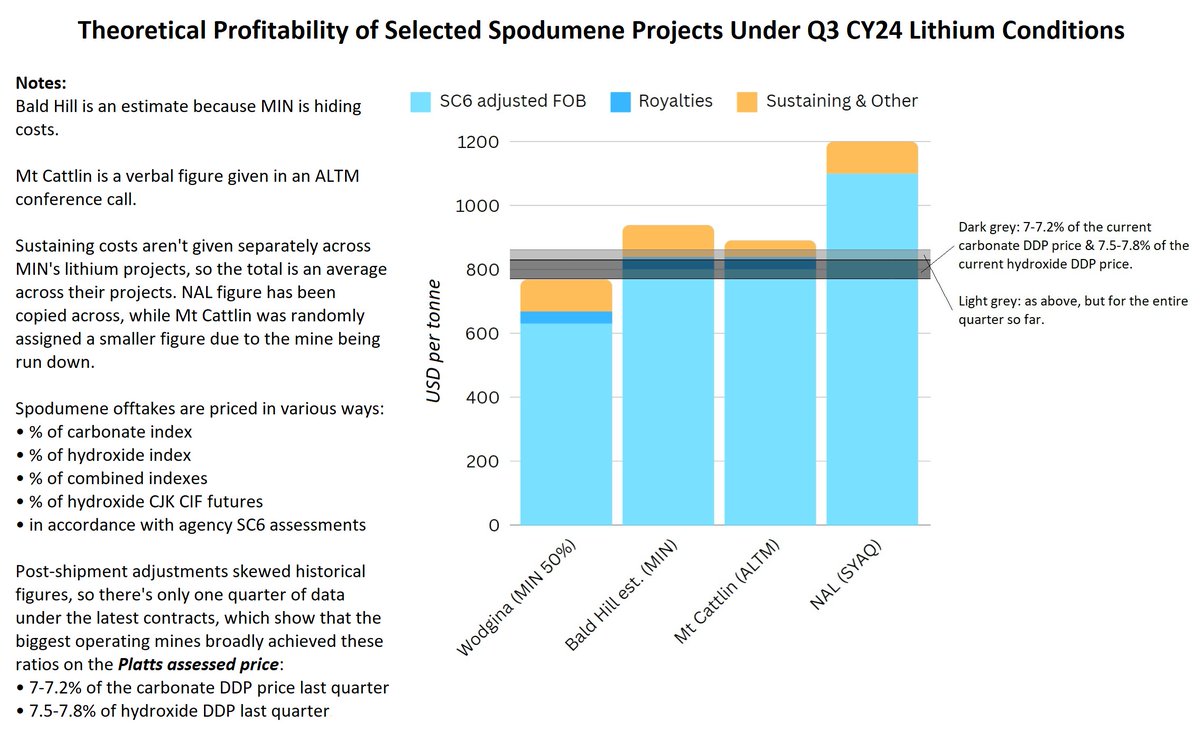

$MIN's Bald Hill & $ALTM $LTM's Mt Cattlin FOBs are inaccurate, but probably not greatly.

Vertically integrated projects more complex: coming later.

$SYA #lithium

Trump tonight: "I'm for electric cars. I have to be because Elon Musk endorsed me, so I have no choice. I'm for them, but for a small slice. They want to go all-electric & there's no way you can ever load (charge) them up; A charger is a gas pump with electricity coming through."

Lots of speculation about Zimbabwe #lithium production costs.

I suggest $SGML, and $MIN's partnership with Ganfeng at Mt Marion, provide possible answers.

Cobbled together info suggesting vertically integrated SC4 operations from Zimbabwe are currently unprofitable.

Any errors?

$IGO quarterly confirms the perils of chem conversion in Australia.

3 of #lithium's big 4 are floundering, set to be blitzed by Posco & $PLS in SK, both in speed and CAPEX.

Is a midstream product like phosphate or sulphate the most realistic path downstream in AUS?

$WES $SQM $ALB

The latest quarterly from $ALB @AlbemarleCorp shows they are taking the necessary steps to preserve their balance sheet. Kemerton is down to 1 train. AUS chemical production from Kemerton and Kwinana is a disappointment. Quinzhou and Meishan, by comparison, are on or ahead of schedule. While our 2030 demand forecast is the same as ALB's, our split is materially different. RK Equity has "grid" at 40% to 50% of EV demand.

Local China-based & China-controlled global mineral & chemical supply continues to grow rapidly. This has made S/D forecasting extremely difficult, especially when the laws of economics seem to be ignored. Excluding government subsidies, almost no one across the entire supply chain is making any real profits. #Lithium

Some more thoughts i had on the lithium market whilst sipping my morning coffee.

Looking at the import data (posted below), these mines producing out of Zimbabwe are running at a combined total of around ~1.21Mtpa of ~SC3.9. To get the 1.21Mtpa, I’ve simply multiplied the monthly output x 12. To calculate the grade, I’ve taken the price it was sold for, $US634.09, and scaled back from the current SC6 spot price.

The total nameplate capacity for Zimbabwe for 2024 is meant to be around ~2.08Mtpa (Arcadia, Bikita, Sabi Star). In 2025, its meant to be around ~2.5Mtpa with the addition of Sandawana and Kamativi. Looking at these numbers for the first time, I initially thought that obviously the Chinese were lowering production at these mines due to supply demand issues.

But after looking a bit closer into who actually owns these mines, I realised that this most likely isn’t the case.

Sinomine, Yahua & Chengxin all own/have interests in mines within Zimbabwe and funnily enough, all have recently signed off-take agreements with Australian producers. Sinomine is to take 100kt of SC6 from Liontown Resources over the next 10months, Yahua is to take 220kt – 400kt of concentrate over the next 3 years from Pilbara Minerals and Chengxin is to take 385kt of concentrate over the next 3 years from Pilbara minerals.

So why did these Chinese companies sign these offtakes if their Zimbabwean mines aren’t anywhere close to full capacity? They are 0.87Mtpa of concentrate short?

My prediction (and I could be off with the fairies here) is that the proper metallurgy test work wasn’t done on these deposits. Maybe large amounts of CAPEX are required to upgrade the plants to be pushing out a decent concentrate. Making a lithium concentrate isn’t easy and requires a lot of prior test work. If you put a DMS in instead of a flotation plant for example, it’s almost game over. There are also many intricacies with flotation plants. They are complex and not easy to run. The fact that ~SC3.9 is coming out of Zimbabwe (my estimation), there are serious processing issues.

The offtakes definitely paint an interesting picture. Why not just increase production at the Zimbabwean mines? Ramp up issues you ask? Bikita has been producing spodumene for over 2.5 years and petalite concentrate for over 5 years…

0.87Mtpa of concentrate is considerable. If we convert this to LCE, 870kt @ SC6:

LCE = 870kt / (40.4/(6*0.85)) = 105kt of LCE missing from supply-demand tables. As stated within my most recent post, the lithium market is expected to be in a surplus of 75-200 kt of LCE per year over the next several years according to several supply-demand tables. Knocking this ~105kt off from supply makes these predictions very interesting.

Next year, the difference in capacity and what is really coming out of Zimbabwe could become considerably larger. Does this mean that more supply should be pulled from supply demand tables? Cheers for reading!