i don't understand why people call this a bailout

a bailout is when government steps in and prints money to save banks or companies at a cost to the rest of society (devaluing everyone else's money)

this can create a moral hazard because if someone is protected from the consequences of their actions, they’re more likely to take bigger risks

this is not what's happening here

private companies are coming together and using their hard earned money to make users whole

this is the opposite of a moral hazard as they will 100% become *more* risk averse in the aftermath to avoid these costs in the future

The aWETH Redemption Protocol is now live on @Arbitrum and @Base.

After processing $400M+ in redemptions on Aave Ethereum, we're expanding to L2s.

This time, we’ll be opening up for all loopers to unwind while ETH lenders exit to LSTs.

How it works 🧵

Introducing aWETH Redemption Protocol

With ETH utilization at 100% on Aave, many lenders are currently unable to withdraw and face increasing risk if markets move.

aWETH Redemption Protocol allows ETH lenders to:

• Exit into wstETH or weETH

• Regain immediate liquidity

• Reduce exposure to liquidation risk

If you’re just lending ETH — you can fully exit.

If you have ETH collateral and another debt — your collateral is seamlessly swapped into wstETH or weETH while your debt remains the same.

We’re working alongside @LidoFinance , @ether_fi, @0xProject, @1inch,

@KyberNetwork, and other ecosystem partners to:

• Reduce systemic risk in DeFi

• Ease utilization pressure

• Support a healthier DeFi market

Our goal is simple: protect users while reinforcing the foundations of DeFi.

Capacity is initially limited to $1B in ETH.

https://t.co/VBIAT9FZyg

Testing out Plasma One by @Plasma for the past 2 weeks

• really good UX

• smooth and fast onboarding

• fx rates slightly better than etherfi

• instant deposits on Plasma

might capture sizable chunk of the payment market soon

thanks @river0x for inviting me

@letsgetonchain Good read!

One question:

In the case of Cross-Collateralization, does that mean the advantage of aggregated liquidation is gone in this mode?

Since every cross-collaterazation position can be quite different and probably hard to group them into tick-based liquidation buckets?

Aave and other DeFi lenders increasingly position themselves as viable alternatives to traditional banks.

One useful comparison is net interest margin (NIM) — the share of borrower interest kept by the platform.

Aave’s NIM has historically ranged from ~0.3% to 1.3%. Large U.S. banks typically operate with NIMs greater that 2%, and regional/community banks often exceed 3% (Fed St. Louis).

From a depositor’s perspective, a low NIM is exactly what you want — more of the lending spread flows to suppliers instead of being captured as platform margin.

That’s a fundamental structural advantage DeFi lending protocols like Aave have over traditional banks.

notice how every new chain wants fluid as launch partner?

there is no better way to bootstrap deep liquidity on stables and FX

welcome to the new paradigm

Now Gold collateral on Fluid is earning 6.3% APR while borrowing USDC is at 6.1%.

You are literally getting paid to borrow against your gold on Fluid!

Smart gold 🪙🌊

the EF is always a few steps behind!

they chose compound (a long-abandoned protocol) over fluid (one of the most innovative DeFi projects in recent years)

- ignored the fourth-largest lending protocol by active loans

- ignored the second-largest DEX on ethereum by daily volume

after every crash there's a migration of loans to Fluid because it simply has the best terms for borrowers:

- highest loan-to-value ratios (e.g 95% on ETH)

- 0% liquidation penalty, aka liquidations are not a source of revenue (10% or higher elsewhere)

- the protocol liquidates the min. amount just enough to bring the loan back to safety (as low as 1%)

the last point is only possible because of their fundamentally different liquidation engine

all user positions are aggregated into a Uniswap V3 type concentrated liquidity range

instead of a per-user auction based liquidation which is gas heavy and only works for big amounts, liquidations on Fluid are just normal swaps executed by retail users on DEX's like @CoWSwap and @KyberNetwork

truly under appreciated what a genius @smykjain is

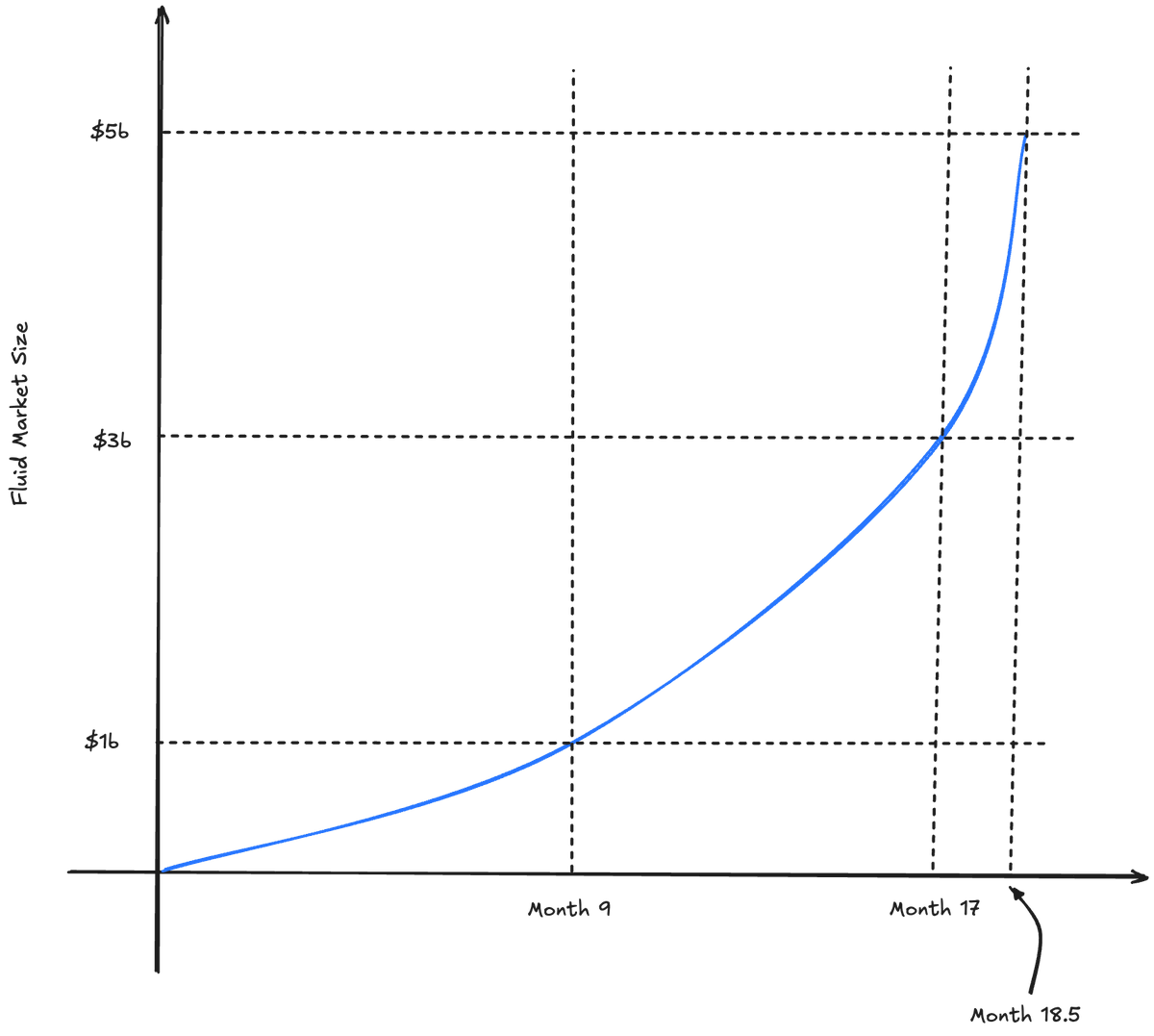

Fluid growth has been tremendous; their deployment on @Plasma and recent collaboration with Jupiter to deploy @jup_lend on Solana added another $2b quickly to their market size.

Fluid is reaching the escape velocity.

Onward.

Again, 50%+ dominance on the market

Although DEX v2 will be focused on volatile pairs, stablecoin volumes will increase even more. Probably up to 70-80% market share

Fluid 7 day annualized rev is at $19.5m

Fluid 30 day annualized rev is at $12m

This is what growth looks like!

The majority of rev is coming from the money market which is growing across Ethereum, Arbitrum and Solana deployments.

This is non volatile growing revenue!

I think the flywheel is unleashed!

Borrowers choose Fluid for low liquidation penalties, higher LTVs, and cheaper borrowing via Smart Debt -> this drives the highest utilization in DeFi -> which delivers the best yields for lenders.

More lenders -> more TVL -> more DEX credit consumption -> deeper DEX liquidity and higher DEX revenue.

Some interesting stuff happening with @0xfluid now:

• Jupiter Lend on Solana has teamed up with Fluid, pulling in $1.2B in TVL in just 21 days. You can now use $JUP as collateral to borrow USDC.

• There’s going to be tons of money flowing into Solana due to DATs. So I think Fluid’s in a strong position to benefit with Jup Lend.

• Fluid’s revenue is on track to overtake incentives. Buybacks are starting October 1st.

All mainnet revenue for the first month is going towards buybacks. This is ~$1.3-$1.5m of buying pressure. There are plans for Jupiter Lend and L2 revenue streams to be added to the buy back program.

• Fluid just ranked #1 among lending DAOs for 30-day active loan growth (+48%).

• #1 in stablecoin swaps

• Wall Street is wrapping tokens like $FLUID into DATs (stock-like products) so traditional investors can get exposure.

• DEX Volume is ~$700m per day. Dex v2 launches next month

• They’re planning to launch on Plasma. Remember, Plasma is an L1 build for stablecoin with a projected $2 billion-plus in stablecoin TVL

We’ve seen what happens this cycle when a protocol has product market fit, sustainable revenue, and implements buybacks.

Lots of great developments that the market hasn’t priced in yet.

Disclaimer: not a sponsored post - just grinding for my bags

People are sleeping on @0xfluid.

One of the major misconceptions is that people think Fluid being the top DEX on Ethereum for stablecoins and other non volatile token pairs is a low margin business and thus not a major revenue booster.

They miss the key point: the DEX is a huge borrower which translates to sticky recurring revenue for the money market.

Among the top 10 lending protocols on Ethereum by TVL, Fluid has:

- highest borrow % vs deposits.

- most revenue per unit of TVL.

Study Fluid.

Data on Solana's fastest growing money market @jup_lend is now live on Blockworks!

- Supplied Collateral

- Outstanding Loans

- Positions

- And more 🔜

Higher.