Identifying a theme, understanding a theme, and making money from a theme are very different ball games.

Spotting a trend early can create excitement. Understanding it requires curiosity, patience, and the willingness to dig beneath the surface. But translating that understanding into investment returns demands something else entirely...judgment, timing, position sizing, temperament, and the ability to sit through uncertainty.

A theme can be right, yet the investment can disappoint. A company can benefit from a trend, yet the stock may already reflect that future.

A lot of people analyze earnings purely quantitatively and are often surprised by the market's reaction to seemingly good (or bad) numbers.

The right Earnings analysis needs:

1. Reading the numbers themselves of course. But this is only half the story.

2. Context of what happened over the last one or two quarters to the earnings of the stock and the sector in general

3. The price action of the stock in last 3-6 months. This broadly tell us what's been the street expectation.

4. The sector or theme the stocks belongs to and how that is being perceived right now.

5. Mgmt commentary post the call that sets up the tone for the future which is what the market really cares more than the published numbers.

6. Broader market sentiment - this just amplifies the reaction based on the above five points.

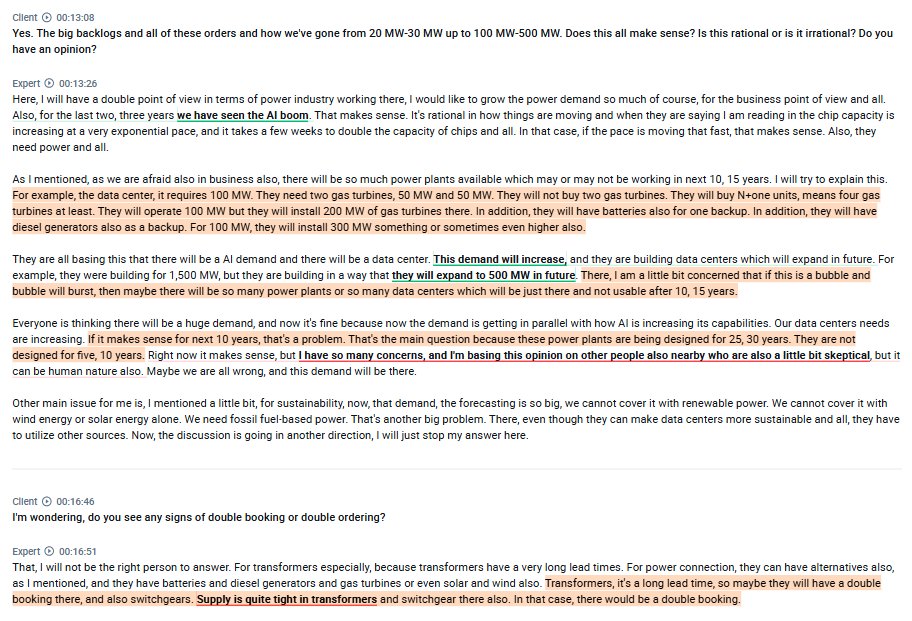

A MUST-read interview with a Siemens employee explaining just how high demand is for energy equipment right now because of AI:

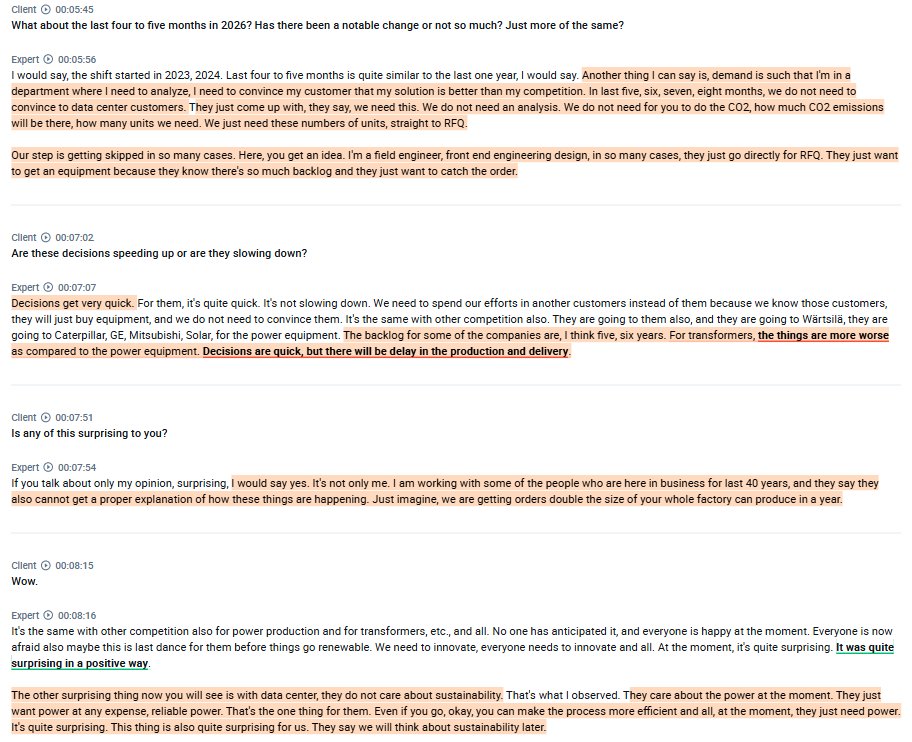

1. The whole situation is shocking even for people who have been in the business for 40 years. They are getting orders that are double the size of what their entire factory can produce in a year.

2. Demand is so high in the last 5-8 months that they don't need to convince or send any analysis (such as CO2 emissions, etc.) to clients because they just want the equipment, because there's so much backlog that they just want to catch the order.

3. Decisions are being made very quickly by clients; the backlog for some of the energy equipment companies is 5-6 years. For transformers, the situation is even more difficult.

4. He mentions that right now, data center builders do not care about sustainability; they just want power at any expense, reliable power. They say they will think about sustainability later.

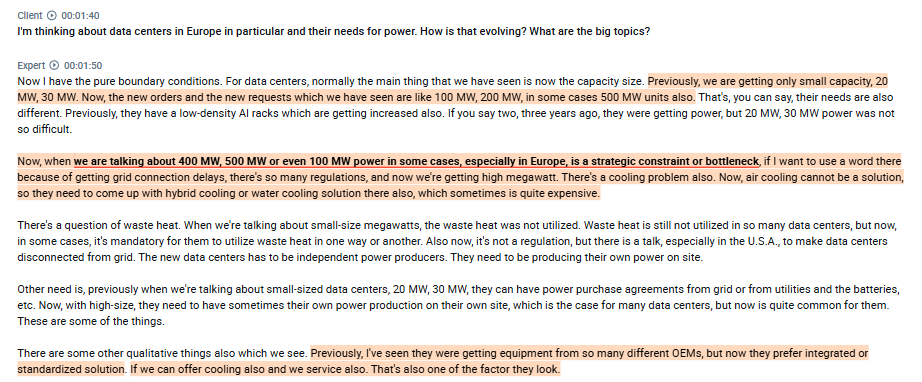

5. The orders have gone from previous 20-30 MW orders to now 200-500 MW units. Customers have previously wanted to get equipment from different OEMs, but now they prefer an integrated standardized solution.

6. An interesting dynamic is that even though the data center requires 100 MW, the builders are buying N+1 units of gas turbines (so more than just for 100 MW) as backups, as well as having more energy capacity, as they believe they will continue to grow that data center.

7. He does believe there is some double booking going on on transformers and switchgears because of extra-long lead times.

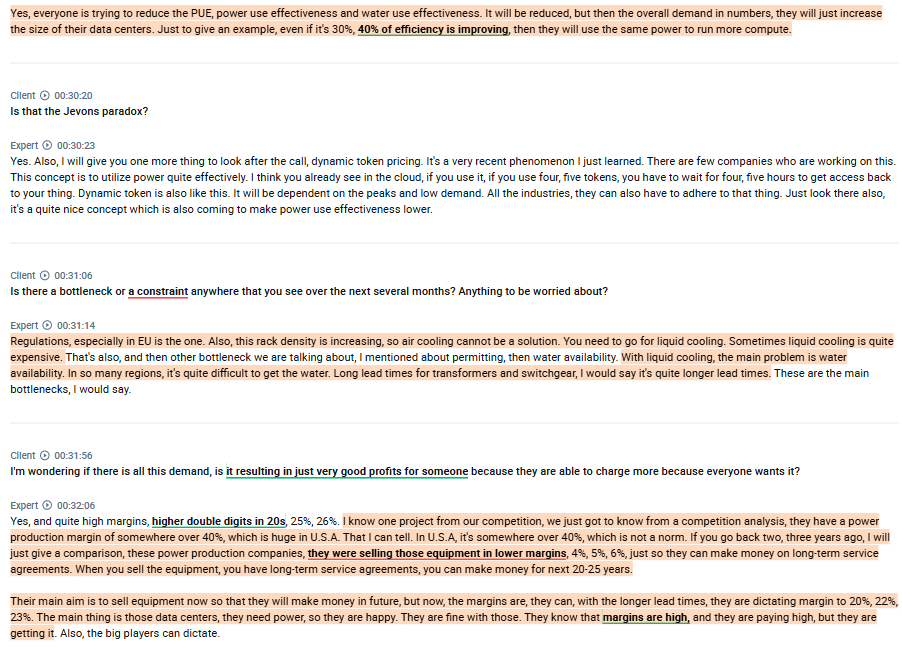

8. Everyone is trying to reduce PUE, and water use effectiveness, but even after improving, they just use the same power to run more compute.

9. The problem is also liquid cooling, as it is expensive, and water availability in many regions is a problem.

10. Margins on equipment in the sector have gone from 4-6%, where they were 2-3 years ago, to 20-23% and in some cases even 40%. The data center builders know the margins are high, but they are fine with it because they just want to get it.

found on @AlphaSenseInc

Citadel Founder Ken Griffin at the Stanford Leadership Forum 2026 discussing how AI agents compress elite analytical work from months into hours:

"It has been interesting to watch...work that we would usually do with people with master's and PhDs in finance over the course of weeks or months, being done by AI agents over the course of hours or days. So these are not mid-tier white-collar jobs. These are like extraordinarily high-skilled jobs being ...automated by agentic AI. And I got to tell you, I went home one Friday, actually fairly depressed by this because you could just see how this was going to have such a dramatic impact on society."

AI has completely changed the equity research game!! Feels scary and enabling at the same time. Detailed research as an edge has now completely evaporated. Focus on breadth, delta identification, mental models, position sizing, EQ and visualisation.

One thing I have learnt over the years is to re look at a stock I once rejected when the facts have changed with a fresh lens that has no baggage/bias , that has helped to really expand on capabilities of buying great companies that have rate of change , something that took me some time to build

The Toll Booth on the Digital Economy → The One Company Without Which AI Does Not Exist

One of the most unique companies in the entire global semiconductor value chain that checks our filter of unique businesses :-

→ High barriers to entry (might need at least 15 yrs to crack which is both R&D and cost heavy to build it)

→ Cannot be replicated even with a blank cheque (China has tried for a decade)

→ Exceptional return ratios

→ Zero direct competitors at the leading edge

→ Doing something that sits at the absolute frontier of human engineering

Let's discuss more on ASML Holding in 3 simple steps :-

→ Why this business is Unique → Financial Health → Growth Triggers

The PFBR achieving criticality is a 22-year journey finally paying off.

India's nuclear program is a three-stage chain reaction by design.

Stage 1 PHWRs produce plutonium as waste. That plutonium becomes fuel for the Stage 2 fast breeder reactor, PFBR. Every four PHWRs generate enough waste to fuel one PFBR. The PFBR then breeds Uranium-233 from thorium blankets surrounding its core. That U-233 becomes fuel for Stage 3 reactors. India has 846,000 tonnes of thorium. Enough to power the country for decades. That's the beauty of this program. India can be permanently self-sufficient on energy.

Stage 2 just went live. One step left.

The plan from here is to build two more FBRs at Kalpakkam, then scale the fleet until it can absorb all the plutonium coming out of India's PHWRs. India has 19 operational PHWRs today with ten more 700 MWe units sanctioned in fleet mode. Every new PHWR generates power and feedstock for the next generation of reactors.

Hoping the next stage takes much less time!

Anthropic just passed OpenAI in revenue run rate. OpenAI is at roughly $25B. Anthropic just crossed $30B. Sixteen months ago Anthropic was doing $1B.

You could add up the annual revenue of Snowflake, Datadog, Cloudflare, MongoDB, and HubSpot and you'd still be $15B short of where Anthropic sits today. Combined they do about $15.4B. Anthropic does double that. A company that didn't exist five years ago.

That $1B was December 2024. By end of 2025 it had hit $9B and people thought the growth would slow. It didn't slow. It doubled again to $14B by February. Then $19B by March. Then the number everyone is staring at today: $30B run rate in April. In a single month they added $11B in annualized revenue. That's an entire Atlassian appearing overnight.

They've 10x'd revenue every year for three straight years. If they do it again, Anthropic hits $100B run rate by end of next year. More revenue than IBM. More revenue than Nike. From a company that earned its first dollar less than three years ago.

Claude Code didn't exist 14 months ago. It's at $2.5B run rate. 4% of all GitHub commits on Earth are now written by Claude Code. That number doubled in a single month. Projected to hit 20% by December. One in five commits on the planet written by one model.

To serve this demand they just ordered $21B in custom chips through Broadcom. Nearly 1 million TPUs. Over a gigawatt of compute. That's enough electricity to power a city of 700,000 people. Just for inference. Not training the next model. Running the current one.

Anthropic pulls $211 per monthly user. OpenAI pulls $25 per weekly user. 8x monetization on a fraction of the audience. Two years ago 12 companies spent $1M+ a year with Anthropic. Today it's over 500. 8 of the Fortune 10 are customers.

The secondary market has already repriced what this is. $2B in buy-side demand chasing Anthropic shares. Almost no sellers. Bids implying a $600B valuation, up from the $380B primary round two months ago. Meanwhile $600M in OpenAI shares are sitting unsold. Goldman is charging 15-20% carry on Anthropic allocations. They're giving away OpenAI for free.

The IPO was originally targeting $500B. It will likely come in north of $800B. At 10x annual growth for three consecutive years, the question isn't whether Anthropic is overvalued. The question is what multiple you put on a company that might be doing $100B in revenue 18 months from now.

Sixteen months ago this was a research lab. They just passed OpenAI and the run-rate revenue of Netflix. And every number in this post will be outdated by next month.

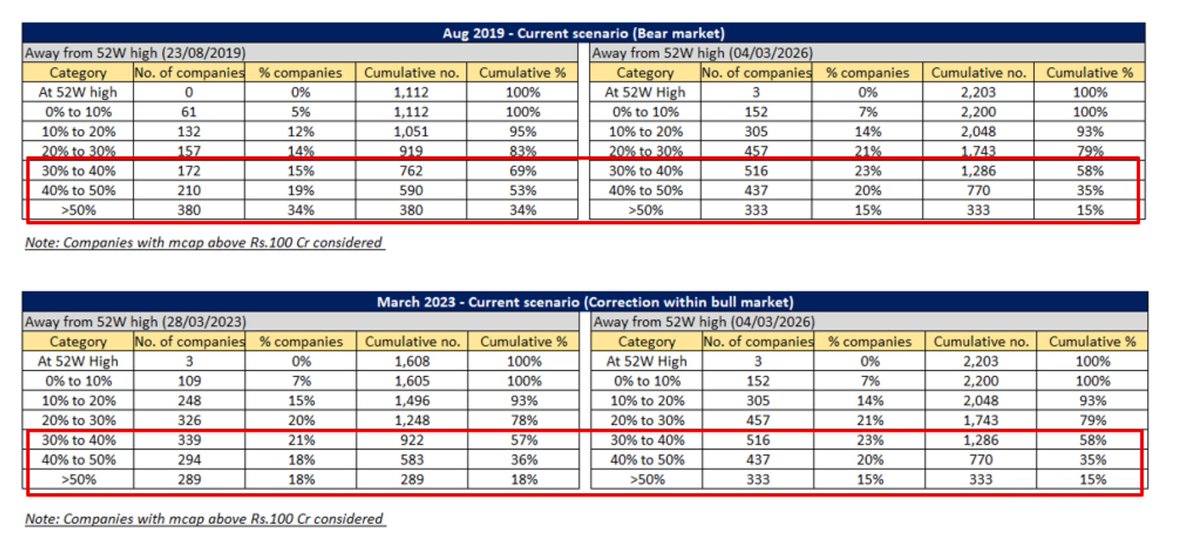

Major learning: Best time to sell losers in the portfolio was yesterday. Get out at the first sign of thesis not playing out, regardless of markets- in bull market the price for course correction is opportunity cost and in bear market- huge drawdowns. Both hurts more with time.

Current broader market looks replica of March’23, though the absolute valuation multiples across most of the counters in March’23 was lower than current ones but very high probability of having great FY27, similar to FY24. Great time to deploy capital. Stock pickers delight.

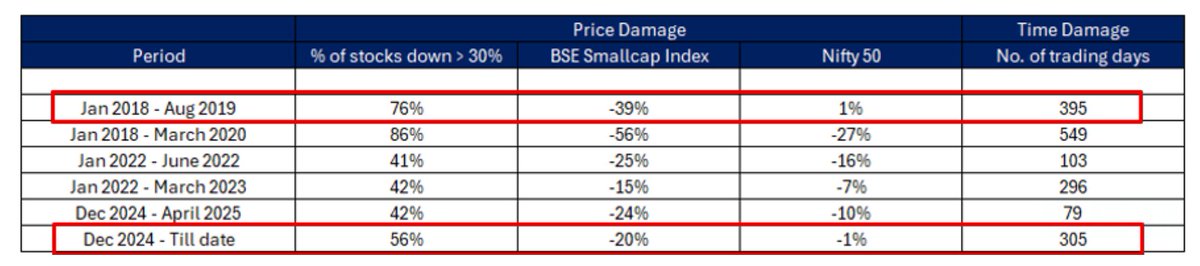

Headline Index is hiding the pain just like Jan 2018-Aug 2019. Markets have seen good time and price correction. Incremental fall will make outlook brighter. Intensity of negative news flow and its price impact could diverge.

This is one of my favorite Druckenmiller interviews. He reveals the type of mentality you need to compound at 30% CAGR for almost 3 decades, without a single down year

"I am a very competitive person, even though it is just my own money [now]. I wish I wasn't, but I am. Probably one of the reasons why my results are good as they are, but I prefer myself not to be. It is a bit of sickness but it works for me"

"I compete against, what I would call, the opportunity set. If there was a great opportunity set that year and I missed it, I am disappointed in myself. If I am up 20%, but I think I should have been up 50%, I am disappointed in myself. If the opportunity set was +10-15%, but I am up 20%, then I am thrilled."

This is probably one of my favorite clips from Stanley Druckenmiller. Listen to it at the start of every new year

"We have always believed that January 1 is when the house starts. I think this is the reason we have not had a down year. When I am up, I will play much more aggressively.

I see a lot of managers get up 20% and say I want to book my year, I made my high watermark, lets go to the beach. I am the opposite. Frankly I learned a lot of that from George [Soros]. If you are up 20 or 30%, you are playing the house money, thats when you try to get up 60 or 70%."

Stanley Druckenmiller, one of the greatest macro investors of all time, arguably the GOAT, saying the quiet part out loud 🧠

Diversification is where conviction goes to die.

All eggs in one basket, full accountability, ruthless monitoring.

That’s how asymmetry is built.

Major learning: Best time to sell losers in the portfolio was yesterday. Get out at the first sign of thesis not playing out, regardless of markets- in bull market the price for course correction is opportunity cost and in bear market- huge drawdowns. Both hurts more with time.

@subhrakantpanda Many congratulations to you for this truly exemplary achievement!

Given our impactful legacy, unparalleled lowest cost market leadership and impeccable corporate governance track record, aggressive growth was the only missing element towards a leap forward.

Choicest wishes ✨🤗