Feels like the only thing that hasn’t crashed…

Is memory like $MU, indexes, or large cap semis like Intel so far.

- Photonics from $AXTI to $SIVE down 40%.

- Space from $ASTS and $RKLB down 40% 1M.

- Popular AI names like $PLTR is down ~35% YTD.

- Software like $CRM down -40%.

- Bitcoin sub <60k, Ethereum sub <$16k.

Not a fun time with a hawkish fed narrative and potential rate hikes.

However this does sorta feel overshot due to margin liquidations on less liquid assets compared to mega caps.

But we’ll see what happens, usually fundamentals override liquidity shock in the longer run.

I’m still personally bullish on the AI buildout + upstream AI capex beneficiaries, but 1-2 potential rate hikes certainly don’t help.

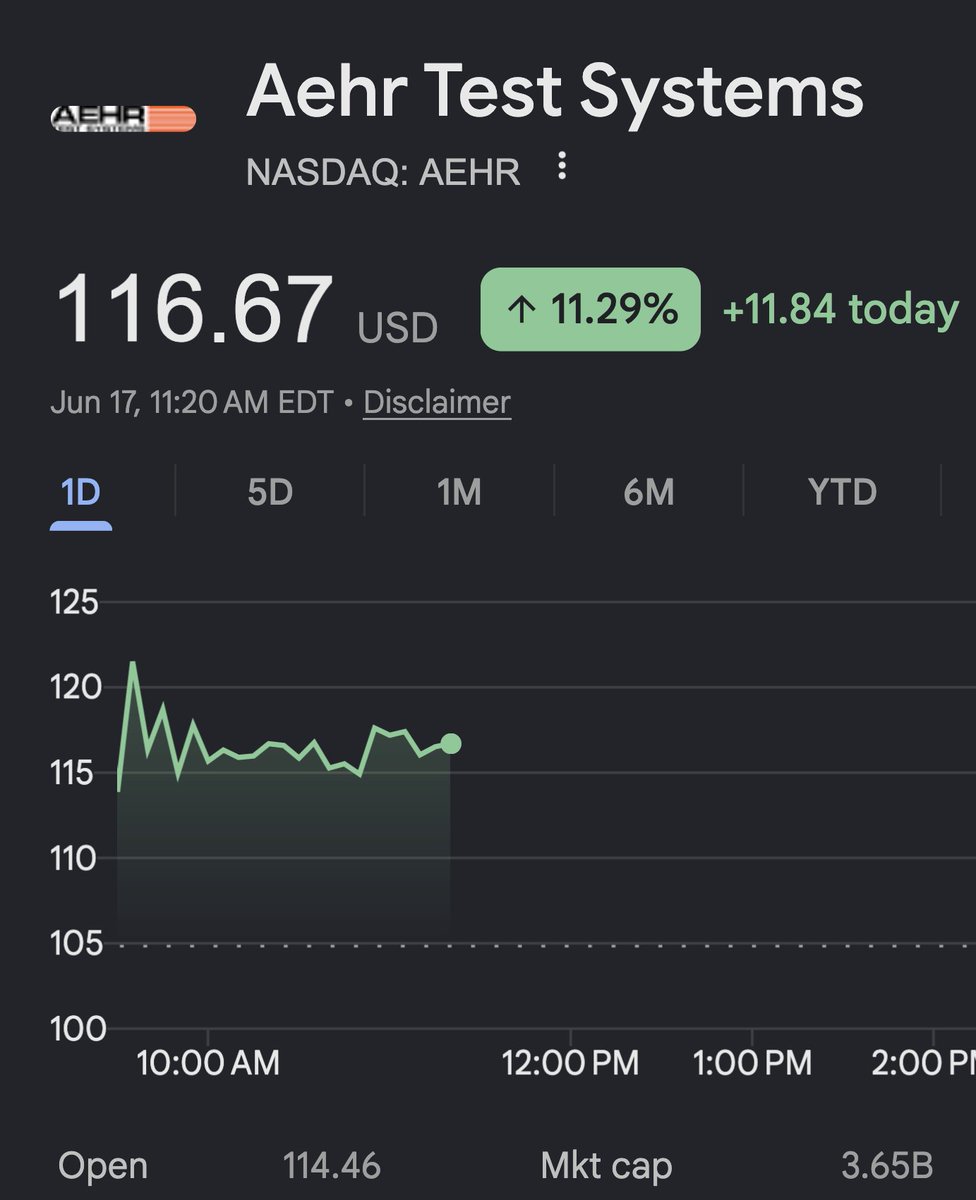

$AEHR receives follow up production order from major Silicon Photonics Customer for wafer level burn in systems.

Now up 11.29% today to $116.

Only 2 months ago it was in the $30's, good times.

Yeah... I'm not quite sure why everyone likes just throwing personal accusations.

Like "scam" or "memestock" every time I post a thesis.

Like when I bought $AXTI (still holding shares btw):

- spent the time mapping the InP substrate supply chain

- found analyst sources around market share

- tracked high purity indium pricing on SMM

- modeled game theory around bottleneck hikes/supply shocks.

- tracked Gov publications like seizure of optical companies or export controls

Then just posted the idea for free, cause it's a hobby.

Everyone just threw out personal insults as it went up in price...

Just for Reuters to confirm it 7M later that InP substrates can halt the AI buildout.

I'm just sharing ideas out for free, could always be wrong, and they usually take some time to play out.

But would prefer instead if folks/media played devil's advocate on the thesis side like export controls or ASP pricing power...

Over just making up narratives or personal accusations like "memestock" or "foreign institutional team" when they lack the technical depth to understand AI supply chains.

Thanks, we might not see a InP substrate bottleneck yet, but we’ll likely see it when hyperscaler ASICs (TPU, Trainium, Maia, etc.) ramp up -> supply strains like memory mid-2026.

That doesn’t quite mean material providers should be valued like $LITE, but the fact that the entire future AI buildout has a single point of failure that comes from a small $600m company like $AXTI is amusing.