🌍 Global Small Caps

📈 Compounders & Special Situations

🔎 Deep Fundamental Research

🎯 Targeting 20%+

🏆Early: $BE $MP $NBIS $ELS.AX $XTB.WA $EQR.AX $212A.T

Welcome, quick introduction to myself and Arborator Capital.

We are a Czech-based investment fund and research team focused on global small and mid-cap equities, compounders, and asymmetric opportunities.

My investing journey started during COVID. Between 2022 and 2024, I managed a small friends-and-family portfolio and spent thousands of hours researching businesses across global markets. The results were decent, but nothing extraordinary. I performed roughly in line with broader markets.

During those years, I began building positions in several companies that would later become some of our biggest winners. At the time, many of these ideas were highly contrarian and deeply unpopular. I was researching companies such as Bloom Energy $BE , MP Materials $MP , and others long before they became widely discussed by investors. In many cases, the charts looked terrible and most investors wanted nothing to do with them.

In 2024, I tried to break into the professional investment industry. I pitched some of these ideas, including Bloom Energy, to several investment firms during interviews in Prague. Nobody was particularly interested. I didn’t receive a single offer, and looking back, that wasn’t surprising. I was young, had no institutional experience, and many of my investment theses looked completely different from market consensus.

There was even a period during 2024 when I seriously considered whether pursuing investing as a career made sense at all.

Then things started to change. The very companies that had been dismissed by most investors began proving the original thesis right. Bloom Energy became one of the most successful investments of my life, appreciating roughly 3,000% from the time I first started pitching the idea. The AI infrastructure story played out, power demand accelerated, and many of the catalysts I had expected started materializing. At the same time, investments such as MP Materials benefited from the geopolitical shifts and supply-chain risks that had originally attracted us to the opportunity.

As those ideas played out, I continued finding new opportunities across defense technology, drones, critical minerals, software, healthcare, energy, infrastructure and others.

One example was Elsight $ELS.AX , an Israeli drone connectivity company that I discovered while researching Australian market by A-Z method. I shared the idea with several friends months before it became more widely known, and it eventually became one of our most successful investments, generating returns measured in several hundred percent.

I also invested early in Lindbergh $LDB.MI and even travelled to Italy with my friend to meet management in person and better understand the business. It was one of our first in-person meetings with a management team. We hope to continue meeting management teams directly and occasionally share some of the insights and observations we gather from those meetings here on X.

We identified Nebius $NBIS with my friend as a unique AI infrastructure opportunity and invested before the story became broadly recognized by the market. We also benefited from the long-term growth of retail investing through investments such as XTB $XTB.WA , one of the leading brokerage platforms in Europe.

Last big winner was EQ Resources $EQR.AX . After recognizing the strategic implications of China’s restrictions on tungsten exports, I identified EQ Resources as one of the few meaningful western producers positioned to benefit from higher tungsten prices. That investment also generated returns of several hundred percent.

And those are only a few examples. Today, we measure our successful investments in dozens rather than a handful. In 2025, our portfolio generated returns well above 100%, and year-to-date performance in 2026 is approaching 70 % (BE excluded). While we are proud of these results, we remain fully aware that investing is a long-term game and that difficult periods inevitably come with success. 1/2

PART 1 — Why We Started Buying 3i Group: When one of Europe’s Highest-Quality Compounders Went on Sale 1/2

What if Europe’s best retailer has quietly compounded revenue at ~25% CAGR over the past decade, delivers industry-leading returns on capital, and still trades at roughly half the EV/EBITDA multiple of Costco despite growing several times faster? We break down why we believe 3i Group’s stake in Action could be one of the most attractive compounders in global public markets. Full write-up coming soon on Substack. Link in bio.

Every now and then, the market gives investors an opportunity that doesn’t come from a deteriorating business, but from deteriorating sentiment. These are often our favorite situations. Not because they’re easy, but because they allow us to buy exceptional businesses at valuations that only appear during periods of maximum pessimism.

Over the past few months, we believe 3i Group $III.L has become one of those opportunities. After reporting results that were, in our opinion, far from disastrous, the stock experienced one of its sharpest corrections in years.

The market reacted to several concerns at once:

•weaker-than-expected like-for-like sales in France,

•some softness in Germany,

•concerns that Action’s extraordinary growth may finally be slowing,

•the announcement of a future expansion into the United States,

•and, more recently, fears that rising oil prices and geopolitical tensions in the Middle East could pressure European consumers.

All of those headlines arrived almost simultaneously. The result? The share price fell from above £40 last year to nearly £19 at the lows. For us, that wasn’t a warning sign. It was an invitation to start buying.

We gradually accumulated our position primarily between roughly £19 and £25 per share, where we believed the market had become far too pessimistic about a business whose long-term economics had barely changed. Even after the recent recovery, we still believe the current valuation offers an attractive long-term entry point for investors looking for a high-quality compounder.

We’ve spent the last few weeks researching the company, visiting Action stores, speaking with industry participants, building our own valuation model, and gradually building a position. Here’s our full investment thesis.

Why did the market panic?

Interestingly, none of the individual concerns would normally justify such a dramatic decline. Instead, investors started combining several narratives together. The first was the weaker same-store sales performance in France.

Action had become almost synonymous with flawless execution over the last decade. When one of its largest markets reported softer comparable sales, many investors immediately began questioning whether the company’s best years were already behind it.Then came another concern.

Management announced plans to begin entering the United States around 2028. Whenever an outstanding European retailer announces U.S. expansion, investors immediately think about all the previous failures. Different consumer preferences. Higher logistics costs. A much more competitive retail landscape. Execution risk.The market quickly started discounting a scenario in which management would destroy shareholder value trying to replicate its European success overseas.

Finally, geopolitical tensions in the Middle East pushed oil prices higher. Since Action imports a large portion of its merchandise from Asia, investors feared higher freight costs, higher inflation and weaker consumer spending across Europe. One negative headline followed another.The stock continued falling. Yet when we looked underneath those headlines, we reached a very different conclusion.

Please look at one of my posts from the end of June (my H1 portfolio update), I shared the positions that contributed the most to this year’s performance.

FitEasy and $SMSH.TA are our highest-conviction ideas today precisely because they haven’t appreciated much yet. We significantly increased both positions only over the last couple of months, so naturally they aren’t the main drivers of this year’s returns.

The biggest contributors were positions we accumulated much earlier, such as $ELS.AX, $EQR.AX, $URGN, and $LDB.MI. Some of those appreciated by well over 100% (and in a few cases several hundred percent), and we’ve gradually trimmed them as they rerated and reallocated capital into opportunities like FitEasy and Smart Shooter.

That’s simply how our process works—we continuously recycle capital from ideas that have already performed into what we believe are the next high-conviction opportunities.

I’d just ask that before making assumptions, please have a look at my previous portfolio updates. They’re public, and they answer questions like this in quite a bit of detail. I’d much rather spend time discussing the investment theses themselves than re-explaining information that’s already available.

🚀 Our first deep-dive on Substack is finally live!

We decided to start with our largest portfolio position — $212A.T #212A (FitEasy).

In our opinion, it’s one of the most mispriced small caps we’ve found globally, and we believe it has the potential for more than 100 % return over the next 2–3 years if the business continues executing as we expect.

📖 Read the full write-up here:

https://t.co/5ZQxAPNNel

Compared with the X thread, the Substack version includes an updated valuation model, cleaner formatting and a more detailed explanation of our investment thesis.

A huge thank you to everyone who has already read and shared it.

Since publishing the write-up, FitEasy has gained another ~10%, accompanied by noticeably higher trading volumes. We’re glad the company is reaching a wider audience and, more importantly, we continue to believe the investment thesis is playing out.

At the same time, $SMSH.TA (Smart Shooter) has also appreciated by more than 10% since we first shared our research. Together with FitEasy, these remain our two highest-conviction positions today.

We’re currently working on several additional deep dives covering what we believe are highly asymmetric investment opportunities across different sectors and regions.

Thanks to the recent performance of these positions, my personal portfolio has now surpassed +80% YTD.

Hopefully that’s only the beginning. We look forward to sharing many more ideas with you over the coming months.

PART 4 — Our Model, Expected Returns and Why 3i Remains One of Our Highest-Conviction Compounders 2/2

Why we prefer 3i over many other European compounders

One question we’ve received several times is why we currently find 3i more attractive than other high-quality European growth companies. Our answer comes down to valuation.

We like several businesses across Europe. For example, Dino Polska $DNP.WA remains an outstanding company. But at today’s prices, we believe 3i offers a better balance between quality, valuation and long-term upside.

You’re effectively buying:

•one of Europe’s best retailers,

•at a discount to NAV,

•with meaningful shareholder distributions through dividends and buybacks,

•while still benefiting from a very long reinvestment runway.

That’s a combination we rarely see.

Risks

No investment is risk-free.The biggest risks we currently monitor include:

1. Same-store sales remain weaker for longer

If comparable sales deteriorated across multiple major markets rather than stabilizing, we’d need to revisit our assumptions.

2. Consumer spending weakens materially

A prolonged European recession would naturally pressure discretionary spending.

Although discount retailers have historically been relatively resilient, they’re not immune.

3. U.S. expansion destroys value

We think this risk is currently overemphasized.

Nevertheless, we’ll closely monitor execution once the rollout begins.

4. Multiple compression

Even exceptional businesses can experience lower valuation multiples if interest rates remain structurally higher.

Fortunately, our investment thesis depends primarily on earnings compounding rather than multiple expansion alone.

Our valuation framework

Ultimately, we don’t think investors should look at 3i as a one-year story. It’s a business where the real value comes from what Action can become over the next decade. To keep ourselves disciplined, we built three different scenarios rather than relying on one optimistic forecast.

Conservative Case

Our conservative scenario assumes:

•approximately 5% annual like-for-like sales growth

•around 10% annual store growth

•only modest operating leverage

•no meaningful multiple expansion

Even under these assumptions, Action continues compounding at an attractive pace.

Our DCF values 3i’s 65% stake in Action at approximately £21bn.

Adding roughly £8bn for the remaining private equity portfolio and net cash results in a total equity value for 3i of approximately £29bn, equivalent to roughly £28–29 per share.

Importantly, this scenario assumes fairly conservative operating assumptions and little valuation expansion.

Base Case

Our base case assumes:

•6-7% annual like-for-like sales growth

•12% annual store growth

•gradual operating leverage as purchasing scale improves

•continued expansion across continental Europe

Under these assumptions, our DCF values 3i’s stake in Action at approximately £34bn.

Adding the remaining £8bn of assets results in a total equity value of approximately £42bn, or roughly £41 per share.

This is the scenario we currently view as the most realistic if management simply continues executing similarly to the past several years.

Bull Case

Our bull case assumes Action continues executing at an exceptional level for another decade.

That includes:

•sustained high single-digit like-for-like sales growth,

•store growth remaining above 10% for significantly longer,

•continued margin expansion,

•and successful expansion into additional geographies.

Under these assumptions, we estimate 3i’s stake in Action could be worth approximately £45bn.

After adding the remaining £8bn portfolio, total equity value approaches £53bn, equivalent to approximately £52 per share.

We assign a relatively low probability to this scenario—perhaps around 10%—but if Action continues delivering as consistently as it has over the past decade.

PART 4 — Our Model, Expected Returns and Why 3i Remains One of Our Highest-Conviction Compounders 1/2

Ultimately, every investment comes down to one question: What do we believe this business can look like three to five years from now? We buy businesses because we believe the market is materially underestimating what those businesses can become over many years. That’s exactly how we’re looking at 3i Group today.

Our investment case doesn’t require perfection

One thing we’d like to emphasize immediately: Our thesis is not based on an aggressive U.S. expansion. It doesn’t require Action becoming another Costco by multiple. It doesn’t require a dramatically higher valuation multiple. Our base case is actually much simpler.

We assume Action simply continues doing what it has done for more than a decade:

•opening approximately 10% more stores every year,

•maintaining healthy same-store sales,

•generating industry-leading returns on capital,

•reinvesting internally generated cash at exceptionally high returns,

•and continuing to gain market share across Europe.

If management simply executes on that plan, we believe shareholders should do very well.

Europe alone offers a massive runway

Perhaps the biggest misconception we see is that Action is somehow approaching saturation. We disagree. Today the company operates just over 3,000 stores. Our own long-term framework suggests Europe could ultimately support well above 10,000 locations. We’re not saying management will necessarily reach that number.

But even if the ultimate opportunity proves materially smaller, the remaining runway is still enormous.

Markets such as:

•Italy,

•Spain,

•Central Europe,

•Eastern Europe,

remain significantly underpenetrated compared with Action’s more mature geographies. That’s why we don’t believe the investment thesis depends on entering entirely new continents. Europe alone could support many years of double-digit expansion.

The U.S. is a free option

One topic that generated considerable concern after the latest update was management’s decision to begin entering the United States. We understand why investors became nervous. Retail history is full of failed international expansions. But we think the market may be overreacting. The current plan is relatively modest.

Initial expansion will consist of only a few dozen stores, with the rollout beginning around 2028. Relative to a network already exceeding 3,000 stores—and a European opportunity measured in thousands of additional locations—we view the financial risk as limited.

If the U.S. expansion struggles, it won’t fundamentally change our investment thesis. If it succeeds, however, shareholders gain access to one of the largest retail markets in the world. To us, that’s exactly what a free option looks like.

Capital allocation continues to impress us

Another reason we remain constructive is management’s capital allocation. Unlike many listed private equity firms, 3i has been remarkably disciplined. Rather than chasing acquisitions simply to grow assets under management, management has increasingly focused on creating value per share.

Recently they’ve been:

•selling selected mature investments,

•recycling capital,

•repurchasing shares while the company trades below NAV,

•and continuing to increase exposure to Action over time.

We think that’s exactly the right approach. When your own shares trade at a discount to intrinsic value, buybacks become one of the highest-return investments management can make. That gives us confidence that management thinks like long-term owners rather than asset gatherers.

Quick note Arrow Exploration $AXL.V our large position.

Today’s Colombian election result could be one of the biggest catalysts for the company. A pro-business, right-leaning candidate won, which could significantly improve the odds of extending Arrow’s key Tapir license beyond 2028.

After the first round, we saw strong moves in $EC and $GPRK, but Arrow’s reaction came later as trading opened in Canada, in the morning trading in London you could buy the stock around the last day trading price, although later the stock was up more than 10 %. This election result is arguably even more important for Arrow than for either of those companies. Today at night trading both $EC and $GPRK are up more than 7 %.

Why?

The market continues to apply a significant discount due to the 2028 Tapir license expiry. If that uncertainty starts to disappear, the valuation could look dramatically different.

At the same time, Arrow remains one of the purest ways we have found to play higher oil prices:

• No meaningful hedging

• Strong balance sheet

• Growing production

• Significant exploration upside

• Multiple catalysts over the next 12-24 months

Even in a downside scenario, we estimate the company could accumulate $70 million of net cash by 2028, providing substantial downside protection relative to its current valuation.

On the upside, we see several major catalysts:

• Tapir license extension

• Additional Icaco discoveries

• Production growth toward management’s 10,000 bopd target

• Potential asset acquisitions

• Future shareholder returns through dividends or buybacks

• Higher oil prices

This remains one of our largest positions.

At current prices, we still believe the risk/reward remains highly attractive.

1/2

#Oil is back around $75, Brent even close to $80. Trump has effectively ended the ceasefire. So what’s the best way to position for a period of higher oil prices?

One of our favorite ideas remains $AXL.V $AXL.NE (Arrow Exploration).

We’ve written about the company last month and it remains in our portfolio.

In our opinion, it’s one of the most asymmetric ways to gain exposure to higher oil prices.

Unlike many small E&Ps, Arrow is already generating significant free cash flow, has no hedging so fully benefiting from higher oil prices, a strong balance sheet w excess cash, and several company-specific catalysts that don’t depend solely on oil prices.

If Brent remains elevated for the next few months, we believe the stock could appreciate by tens of percent.

And if oil prices normalize lower, we still think the downside is relatively limited thanks to the company’s attractive valuation, cash buffer and oil price unrelated catalysts.

The most important catalyst is Colombia. Following the recent political developments, we believe the probability of obtaining the remaining production licenses has improved materially, which could unlock additional value beyond the macro story.

Interestingly, the London listing has barely reacted so far. It’ll be worth watching how the Canadian market prices the news once it opens.

Below I’m reposting a more detailed thread I published about two weeks ago explaining why we continue to own the company and why we still believe it’s one of the most attractive oil names in the small-cap space.

Quick note Arrow Exploration $AXL.V our large position.

Today’s Colombian election result could be one of the biggest catalysts for the company. A pro-business, right-leaning candidate won, which could significantly improve the odds of extending Arrow’s key Tapir license beyond 2028.

After the first round, we saw strong moves in $EC and $GPRK, but Arrow’s reaction came later as trading opened in Canada, in the morning trading in London you could buy the stock around the last day trading price, although later the stock was up more than 10 %. This election result is arguably even more important for Arrow than for either of those companies. Today at night trading both $EC and $GPRK are up more than 7 %.

Why?

The market continues to apply a significant discount due to the 2028 Tapir license expiry. If that uncertainty starts to disappear, the valuation could look dramatically different.

At the same time, Arrow remains one of the purest ways we have found to play higher oil prices:

• No meaningful hedging

• Strong balance sheet

• Growing production

• Significant exploration upside

• Multiple catalysts over the next 12-24 months

Even in a downside scenario, we estimate the company could accumulate $70 million of net cash by 2028, providing substantial downside protection relative to its current valuation.

On the upside, we see several major catalysts:

• Tapir license extension

• Additional Icaco discoveries

• Production growth toward management’s 10,000 bopd target

• Potential asset acquisitions

• Future shareholder returns through dividends or buybacks

• Higher oil prices

This remains one of our largest positions.

At current prices, we still believe the risk/reward remains highly attractive.

1/2

Thanks, I think these are all very fair questions.

Regarding Fast Fitness Japan, I actually think the differences are larger than they initially appear. By the time the take-private happened, the business was already much more mature, competition had intensified (particularly from ChocoZAP), margins were under pressure and they were investing heavily just to defend market share. They had also started expanding internationally, which to us suggested the domestic opportunity was becoming increasingly mature.

In contrast, I think FitEasy is still much earlier in its lifecycle. Based on our model, we expect revenue to grow roughly 50–60% this year, followed by around 30% annually over the next couple of years. More importantly, unlike Fast Fitness Japan, we expect margins to continue expanding as the revenue mix shifts toward higher-margin recurring franchise income. So far, management has consistently executed well and has repeatedly raised guidance rather than cutting it.

We also believe there is still a substantial runway for expansion. Our base case assumes around 1,000 clubs over time, which we think is achievable given current penetration. The network is still far from that level, so we don’t believe saturation is the main issue today.

I completely understand your point about same-store sales growth. Normally I’d agree that rapidly expanding gym chains can benefit from younger stores maturing. However, what surprised us was that even clubs that have been open for around five years are still growing membership by roughly 10% annually, while second- and third-year clubs are often growing closer to 20%. We shared the underlying chart in our write-up because we thought it was one of the most interesting operating metrics the company reports.

Another important difference, in my opinion, is positioning. ChocoZAP competes primarily on price and convenience, while Fast Fitness Japan remains a fairly traditional 24/7 gym operator. FitEasy is increasingly building a premium ecosystem around the membership—golf simulators, coworking, wellness, beauty services and other complementary offerings. I actually think this makes the concept much harder to replicate than it first appears, because competitors would need fundamentally different layouts, larger spaces and significant capital investment rather than simply adding a few new services.

That’s why we believe FitEasy is more likely to take share from competitors than the other way around if management continues executing.

Finally, regarding valuation, I certainly wouldn’t argue that our bull case is the most likely outcome. We’d probably assign something like a 10% probability to that scenario. Our focus is really on the base case, which we believe already offers an attractive risk/reward if the company simply continues executing as it has over the last 18 months. To be honest, we’ve actually had to revise our own forecasts upward several times because the company has consistently exceeded our expectations. So far, we simply haven’t seen meaningful evidence that the underlying growth engine is slowing.

Two Themes We’re Betting Big On 1/4

First of all, thank you! We started this account only a short while ago, and we’ve already surpassed 1,000 followers.

Today I wanted to share two investment themes where we currently have some of our highest conviction. We believe both are still in the early innings, supported by strong structural tailwinds rather than short-term market sentiment. While not every company will succeed, we think a handful of businesses in these sectors have the potential to become true multi-baggers and significantly outperform global equity indices over the coming months. These are exactly the kinds of opportunities we’re spending hundreds of hours researching—and where we’ve allocated a meaningful portion of our portfolio.

We’re also putting the finishing touches on our Substack, where we’ll publish much longer research reports, complete financial models and deep dives into our highest-conviction ideas.

Our updated FitEasy report is almost finished, and we already have several additional write-ups in the pipeline.

👉 https://t.co/ec5KmVMgM7

Now back to two themes where we’ve allocated a meaningful part of our portfolio and where we still believe the market is underestimating the long-term opportunity.

These obviously aren’t the only ideas we own, but they’re two sectors where we believe structural tailwinds, industry transformation and attractive valuations could still create returns measured in tens of percent—or potentially much more—over the coming years.

The two themes are:

• Drones & Counter-Drone Defense

• Critical Minerals & Supply Chains

Let’s start with drones.

Two Themes We’re Betting Big On 4/4

Another commodity opportunities we’re particularly excited about

Another position we’re very optimistic about is a small copper producer that we aren’t ready to disclose publicly yet.

Interestingly, despite the recent weakness across much of the mining sector, it has continued to significantly outperform many other commodity stocks over the past few months.

Even after that move, based on our model, we still believe the company trades at a forward free cash flow yield comfortably in the double digits. If execution continues, we think the market is still underestimating its earnings power.

We’ll likely publish a full write-up once we’ve completed our accumulation.

Beyond copper, another market we’re researching very closely is nickel.

Over the past decade, Indonesia has completely transformed the global nickel industry.

Supported by Chinese investment and processing capacity, the country rapidly became the dominant producer, pushing many higher-cost Western producers out of the market.

From a cost perspective, that made perfect sense. From a strategic perspective, however, it created another highly concentrated global supply chain. Now, we believe that story may be starting to change.

Indonesia has begun tightening regulations around nickel production and processing, introducing stricter rules that increasingly favor domestic value creation instead of simply exporting raw materials at the lowest possible price.

If these policies continue, they could materially reduce the supply advantage that has pressured non-Indonesian producers for years.

We’re still doing a lot of work in this area, but we think it could become another highly attractive investment theme over the coming years.

If supply becomes tighter while demand from batteries and industrial applications continues to grow, producers located in jurisdictions such as Australia and Canada could become increasingly valuable.

More broadly, one of the biggest conclusions from our research over the past few years is that security of supply is becoming just as important as cost of supply.

For decades, the world optimized almost exclusively for efficiency. Today, governments and corporations increasingly optimize for resilience.We don’t think this shift is temporary.

Whether we’re talking about rare earths, tungsten, copper, nickel or other strategic materials, we believe Western supply chains will continue receiving substantial investment over the coming years.

That doesn’t mean every mining company will succeed. Far from it.

Mining remains a difficult business.

But we do believe that selected producers with long-life assets, strong balance sheets, low operating costs and exposure to structurally constrained commodities could deliver exceptional shareholder returns over the next several years.

These are just two of the broader themes we’re currently most excited about.

Our portfolio contains also other ideas across healthcare, construction, software, industrials and consumer businesses, we generally prefer focusing on areas where we believe we have a genuine informational edge rather than simply following what’s already popular.

Over the coming months we’ll continue publishing our highest-conviction ideas, valuation work and deep research on Substack, while using X to share ongoing developments, portfolio updates and shorter investment thoughts.

Hopefully these posts provide a useful look into how we think about markets and where we’re currently finding opportunities.

And as always, if you have a different view, or know something we don’t, we’d genuinely love to hear it. One of the biggest advantages of building a community on X is learning from investors around the world who specialize in different industries and regions.

Two Themes We’re Betting Big On 3/4

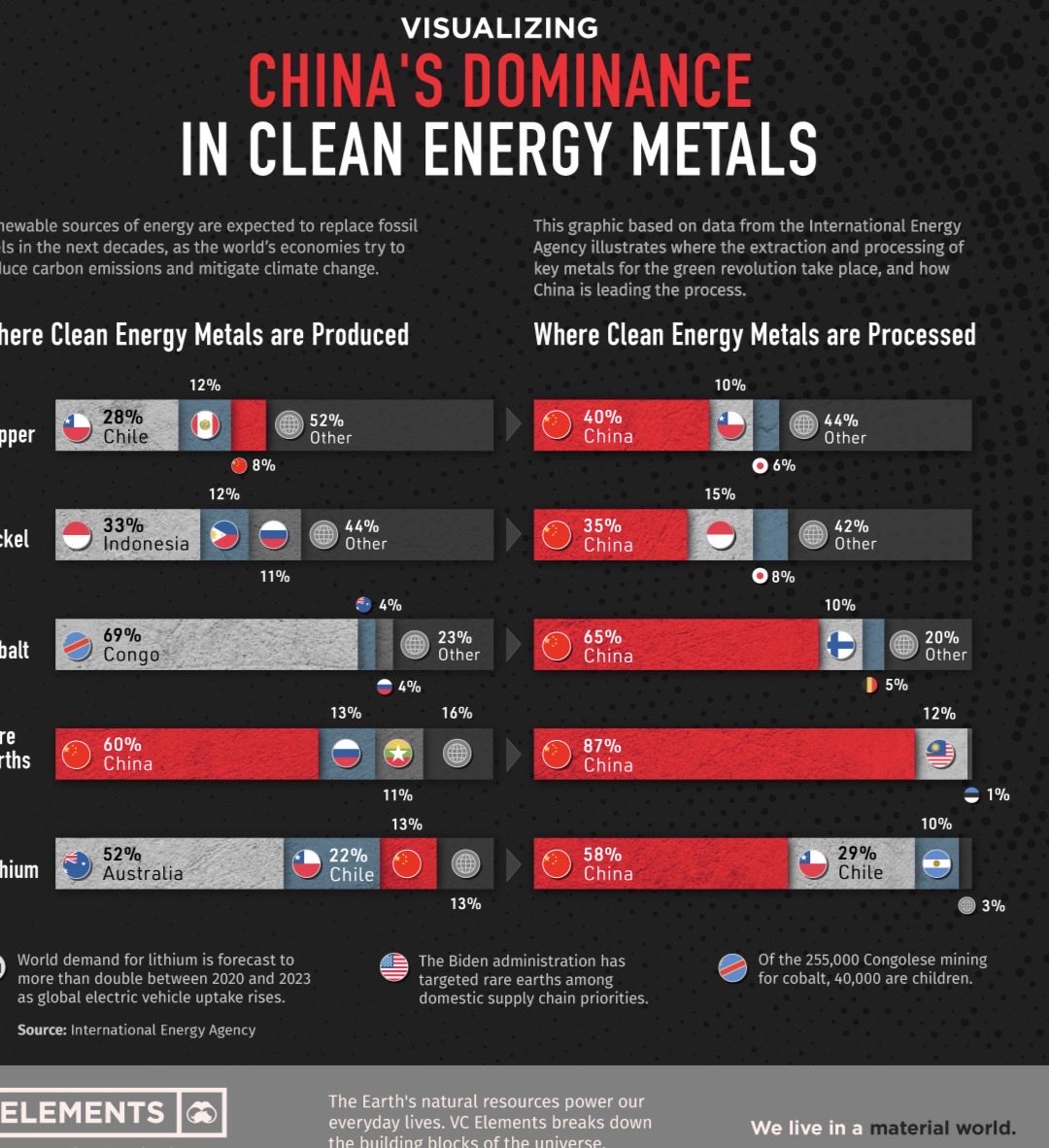

Critical minerals: where supply chains are starting to matter again

The second theme where we’ve been allocating capital is critical minerals and strategic supply chains.

For years, the market optimized almost exclusively for the lowest-cost producer.

Today, the world is slowly realizing that security of supply can matter just as much as cost.

China has built dominant positions across many commodity supply chains—not only in mining, but also in refining, processing and downstream manufacturing.

That worked extremely well in a globalized world. But in a more fragmented geopolitical environment, we believe many Western supply chains are simply too fragile.

We’ve already seen how powerful these setups can become.

$MP (MP Materials) was one of the best examples: one of the few Western rare earth companies attempting to build an integrated supply chain from mining through refining to permanent magnet production.

More recently, we’ve seen a similar dynamic in tungsten, where Chinese export restrictions helped expose how concentrated global supply really is.

Our exposure there has been $EQR.AX (EQ Resources), which we believe is becoming one of the most important tungsten producers in the Western Hemisphere.

But the broader point is not only rare earths or tungsten.The same logic applies across multiple commodity markets.

One area we’re particularly focused on right now is copper.

Unlike tungsten, our copper thesis is less about a single export restriction and more about long-term supply/demand.

AI infrastructure, data centers, grid upgrades, robotics, EVs, renewable energy and electrification all require significantly more copper.

At the same time, many large high-grade deposits are being depleted, new projects often have lower ore grades, higher capex requirements and longer permitting timelines, and the sector has been underinvested for years. That creates a very attractive setup.

What makes the opportunity in miners even more interesting is valuation.

Across smaller commodity producers, we still find companies trading at free cash flow yields that can approach 40–50% under current commodity prices.

That is extremely rare in most parts of the market. Small producers are often ignored, under-covered and too illiquid for large institutions. But for us, that’s exactly where opportunities can appear.

One account I read regularly in this space is @GPs_capital_, who does excellent work on small commodity producers across different geographies and metals.

One example we currently like is $ORV.TO (Orvana Minerals).

It gives exposure to both gold and copper, trades at what we believe is a very low valuation relative to current cash generation, and has several potential catalysts ahead.

GP Capital has written very detailed work on the company, and we found the setup compelling as well.

In our view, companies like Orvana are a good example of why we still spend time in small-cap mining despite the sector being difficult.

When sentiment is poor, the market often prices these businesses as if current cash flow is temporary or irrelevant. But if management executes and commodity prices remain supportive, the upside can be substantial.

The bigger picture is simple:

The world needs more strategic materials. But supply is increasingly difficult, expensive and geopolitically sensitive.

That combination creates opportunities in small producers with real assets, current or near-term cash flow and exposure to commodities where supply chains are structurally tight.

We don’t think every mining company deserves a high valuation. Most don’t.

But selected small producers in the right commodity, right jurisdiction and right set up still offer some of the most asymmetric opportunities we see today.