In today’s Going Private, our twice-weekly newsletter about private markets, we look at the fading bull case for private equity https://t.co/IXvTicG5R0

PIMCO WARNS DEFAULT WAVE IS COMING

PIMCO warns that a credit-loss cycle is underway, with defaults expected to rise sharply among lower-quality borrowers, including leveraged and private credit companies. The firm says AI-driven disruption could hurt heavily indebted businesses, while current credit markets appear complacent about risks. PIMCO favors intermediate-term government bonds, citing recession risks, persistent uncertainty, and the potential for future central-bank rate cuts.

Since @costplusdrugs was listed on TrumpRx on May 18, we have implemented price reductions on 90 products as part of our regular weekly pricing review process.

We expect these price cuts will continue as our volumes grow

I doubt the barefoot hike. I'm no fan of the Christopher Columbus complex, and I happen to admire elites who develop a country rather than exploit one. So let me explain what is actually going on here.

I did, among others, property across Eastern Europe during my years at Babcock & Brown, and I spent the better part of a decade fighting a court case in Romania against people who tried to defraud my land title. I won. And here is the lesson I paid for: the one thing that separates an investable Eastern Europe from an uninvestable one is European Union membership. It is the guardian of the rule of law in an otherwise wild East, the easiest place in the world to lose your money.

That is the lens through which I read what is happening on Sazan Island.

You see, there was a time when Western elites saw themselves as custodians of institutions, rules and the places they touched. That instinct is fading. What remains too often is the Columbus reflex: arrive by yacht, "discover" land that people already know perfectly well, and treat the rules as obstacles reserved for everyone else. And then have the wisdom to go on camera and brag about it. Jesus. No wonder Albanians are now on the streets in their thousands.

"We were on a friend's boat and stopped for a swim. That's how we found it. We swam to the island. We went on a hike, barefoot all the way up to the top, and we were just captivated."

What she "found" has been there for millions of years, in the Adriatic, not "the Mediterranean." It has a name. Sazan Island sits where the Adriatic meets the Ionian: a former military base, Italian and then Cold War, including a Soviet submarine base, inside a protected national marine park that has been open to the public since 2017 via boat tour from Vlorë. An island crawling with snakes, including the nose-horned viper, Europe's most venomous. So much for the barefoot hike.

Nothing was discovered, and nothing justifies any entitlement. Quite the contrary.

What actually happened is that Jared Kushner set out to cash in on his father-in-law's temporary power as President of the United States. That status means precisely nothing in Switzerland, with its seven centuries of direct democracy and institutions no outsider can buy. But it means everything to a weak man like Albania's prime minister, Edi Rama, cornered at home, courting Washington, and now under criminal investigation for how his government handed this deal away. Kushner understands that asymmetry perfectly. And he wants to exploit it. Period.

In Albania, he can. Albania is chronically bureaucratic, the long tail of its communist heritage, a home-grown Stalinism so absolute it broke even with Moscow and sealed the country off from the world. That legacy is the same one that ran, and still runs at times, from Sarajevo to Tirana, from Bucharest to Belgrade: decades of one-party rule that hollowed out the courts, the press and property itself, and left a vacuum filled by the personalised, strongman power of a connected few. It is the soil in which corruption flourishes, and Albania's greatest vulnerability.

And on that soil, in one of Europe's poorest countries, the island's protected status was suddenly changed in December 2024, in the weeks between Trump's election victory and his inauguration. Just like that. The public-tender rule was bypassed. "Strategic Investor" status went to a Kushner-linked SPV before the inauguration: no business plan, no feasibility study. Wonderful. Because Ivanka "discovered it". Right? Wrong.

A country vulnerability like that can be met in two ways. A responsible investor sticks to the rules and ties his fortunes to the country's long-term development, because that is what makes returns durable in the first place. And that will take a lot of time and upfront investment, with a highly uncertain reward. That's called risk-taking.

A powerful one, on the other hand, willing to bend the rules, as this deal suggests the Trump family is content to do, sees only something to exploit.

The subsequent damage runs far deeper and longer than a few harmless bungalows built without a proper concession. What is happening here is that Kushner is becoming part of the problem that corrodes Albania's path into the European Union. That is the real issue here. Just like the issue when JD Vance travelled to Europe and openly campaigned for illiberal politicians while lecturing Europeans about democracy. Who do these people think they are? Guardians of democracy?

Consider what the Albanian path actually looks like right now. The Balkans, like much of post-communist Europe, are chronically corrupt. But they are also full of people fighting to turn their countries toward something better, and EU accession is the single most powerful tool they have. It forces the one thing that actually develops a country: predictable rules, secure property, contracts that hold, and the credible belief that the same rules apply to everyone.

That belief is what brought the great wave of investment into Poland. Its absence is why Romania and Bulgaria remained under special monitoring for years after accession. The rule of law that eventually held in that Bucharest courtroom, and saved me, exists because membership forced it into being. Brussels learned the lesson. Today enlargement runs on a "fundamentals first" basis.

Which is exactly where Albania stands.

Last month it became only the second candidate after Montenegro to clear those rule-of-law benchmarks, with the EU's own enlargement commissioner describing SPAK, the very prosecutor now investigating this deal, as the country's "most trusted institution." The concession lands squarely on the chapters that decide membership: the judiciary, justice and public procurement. So this is not a side issue to Albania's European future. It is a direct test of it.

And that is why this does not help. It does the opposite. A single family connected to the presidency of the United States showing that the rules bend on demand corrodes the one asset a poor country cannot afford to lose: the belief, hard-won and easily lost, that the rules are real.

Then those same people have the chutzpah to complain about corruption in Eastern Europe and lecture the world about American exceptionalism. It is all so deeply wrong. And make no mistake, it erodes our democracies too, ever so slightly.

The thousands in the streets of Tirana understand all of this instinctively. They are not protesting a resort. They are defending the only thing that gives their country a future and hope: the rule of law applied equally to all.

And make no mistake about who the brave ones are. They are not on a yacht. They are on the street of Tirana and inside SPAK, because in Albania, stepping on the toes of the powerful is done in the knowledge that the danger is real. Confronting entrenched corruption in the Balkans has cost prosecutors, judges and journalists their their lives. That is the issue here, ladies and gentlemen!

I doubt Ivanka loses any sleep over any of this. Her concern is closing the deal while her father remains in office. And on a timeline that tight, a public tender, one they may well have won fairly, becomes an inconvenience rather than a safeguard.

That is the difference between a custodian of capitalism and democracy like Warren Buffett and the late Charlie Munger and a primitive land-grabber without any moral compass and integrity.

The world’s largest private investment group said investors in the $45bn Blackstone Private Credit Fund attempted to withdraw 10% of its net assets in the second quarter. https://t.co/fctosiQVvN

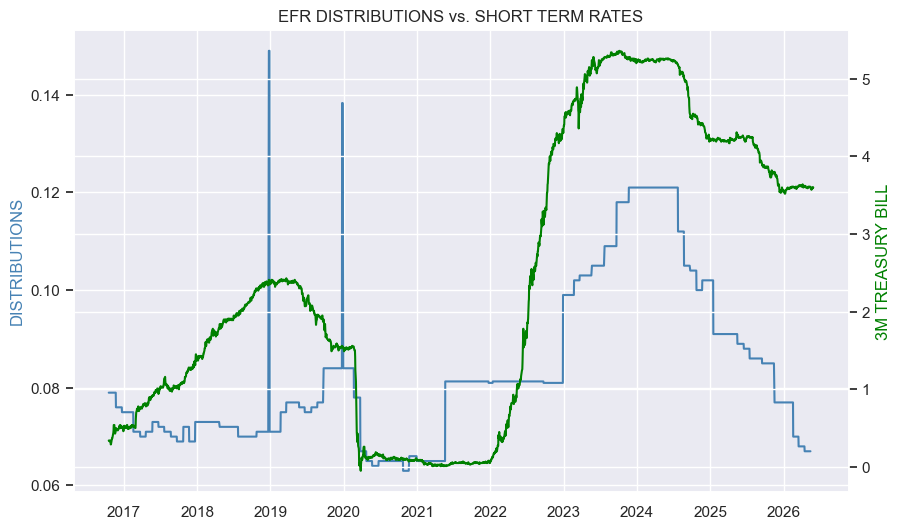

Eaton Vance continued to cut CEF distributions with floating-rate exposure like $EFT, $EFR, $EVG, $EVF, $EVV though the cuts were marginal. A fund like EFR has been cutting for a couple of years now and its distribution is back to its level prior to the inflation spike in 2022.

The fact that EFR is still cutting is a bit unexpected for two reasons. One, the last cut happened about half-a-year ago and it takes a quarter for the Fed cut to make its way through accruals so the fund is cutting despite short-term rates no longer being a headwind to net income.

The second unexpected dynamic is that the fund is still cutting despite distributions being back to 2021 levels i.e. when short-term rates were zero vs. 3.6% today. The potential explanation for both is the same dynamic that’s been weighing on BDCs and CLO Equity CEFs which is loan refinancings to tighter spreads.

@kkmaway@Noahpinion And likely come from places where the comforts of modern life are rather scarce. May not be pretty but heating, cooling and running water…

11% exposure to Software is no walk in the park for #BSL#CLOs with 10x leverage, diversity of ~85 across 30+ industries. Remember that in 2015-2016, CLOs with double-digit Oil & Gas exposure got pretty banged up, downgraded with junior tranches that ultimately defaulted.

Q1 results for CLO Equity funds are coming in. These are less interesting than for their BDC counterparts as we get monthly NAVs from the sector. However, it is still useful for the commentary we get from management and the dynamics they see impacting performance.

$ECC largely blamed lower loan prices, particularly in the software sector, for the drop in the NAV which fell 27% during the quarter and bounced 9% in April as loan credit prices rose. ECC software exposure was 11% which is roughly half that of BDC exposure (and less on an NAV basis due to lower leverage).

Recall that management blamed a loan refinancing wave (driven by tighter public spreads from CLO demand) for the weakness in the NAV over the previous year. Over Q1, the culprit was wider spreads (i.e. lower loan prices) which pulled the NAV lower. This illustrates the concave profile of CLO Equity - big moves in spreads either way drive the NAV lower.

@UrbanKaoboy The few #CLOs overexposed to energy were issued in 2013-15 when there was high O&G issuance, had RP4 and 15% max 1-industry limit (pretty standard for the vintage) but actual portfolios had 11-12% O&G, very high. By the time energy blew up they still had plenty of RP left. 1/