QuantumScape’s Hidden AI Infrastructure Thesis $QS

Why the company’s AI infrastructure strategy could become a second multi-billion-dollar licensing platform

My run‑hot thesis

Yes you’re not bullish enough.

Markets are finally asking the right question: what kind of earnings and multiples can a Trump‑era, AI‑powered “run‑hot” regime actually support, and how does that differ from the post‑GFC world of secular stagnation and permanent caution. The answer looks less like a replay of the 2010s and more like a modernised version of the late 1980s and 1990s, when growth, productivity and valuation rose together.

For those who take the long view, not the day‑trading crowd, the run‑hot thesis is a framework for compounding real earnings and productivity over years, not for trading the next headline.

In this sequel, Trump runs the economy hot, nominal GDP grows near 7 per cent a year and S&P 500 earnings grow at roughly 1.5–2 times that pace, powered by an AI capex super‑cycle, full expensing and a deliberate rebuild of productive capacity. If earnings are around US$400 in 2027, that regime produces roughly US$600–650 by 2031, implying 10.5–14 per cent annual EPS growth.

From there, valuation drives the range of outcomes. In the base case, the market believes the story but stops short of mania: earnings near US$600, forward multiples around 22 times and an S&P 500 in the low‑to‑mid 13,000s. A stronger supply‑side bull case, where investors treat this as a durable productivity reset, stretches to 25 times earnings and 15,000–16,000. A euphoric 1999‑style phase pushes the multiple towards 30 times and the index into the 18,000–19,500 band, with dividend reinvestment lowering the hurdle on a total‑return basis.

The alternative, a world that only delivers 10,000 by 2031, is simply the old regime in disguise: slower nominal GDP, middling earnings and flat multiples. The run‑hot thesis says that anchor is wrong. In an AI‑driven, supply‑side American system, investors either price a genuine repricing of productive capacity, or they mis‑price a decade of higher output before it happens.

President Donald J. Trump is calling on the leading U.S. AI companies to build, bring, or buy all of the energy needed for building and operating data centers, ensuring American consumers are protected from price hikes.

@PierrePoilievre “To be clear” = virtue signal loading…

“Affordable” = we know you are poor, here’s $5 for the month”

“For Canadians” = for everyone not born here.

“We will build” = we will regulate how you should build. And then deny it still

“We will invest” = We will siphon your taxes

@MikePMoffatt lol. The problem is industry experts are just realizing this has been happening. Everywhere across Ontario

Fees on top of other fees just for your local council to recite the land acknowledgement before deciding to slowing down development and progress.

Lots of work to do.

Citi: Physical AI Summit

> According to a Wednesday morning note by Citi analyst Heath Terry, the robotics industry is moving past the experimental phase and into commercial rollout, though he warned that scaling these operations is still a major hurdle.

> Terry informed clients that enterprise demand is surging due to labor shortages, the reshoring of manufacturing, and supportive regulations. However, he noted that growth is still being dragged down by data scarcity, a shortage of skilled talent, restricted battery life, and expensive deployment costs.

> At the event, Instawork pointed out that even if the industry accumulates tens of millions of hours of real-world data by 2026, it would only be a fraction of a percent—mere fractions, not whole percentages—of the massive data volume needed to build high-performance robotics.

> While digital AI allows large language models to capture most of the value through easily replicated foundation models, embodied AI derives its value from unique, real-world data, specialized hardware, and strict safety certifications. Consequently, adapting to new tasks or environments typically requires compiling entirely new datasets from the ground up.

> Furthermore, power supply, battery longevity, and chip architecture are becoming major bottlenecks. Attendees noted that current semiconductor platforms are built for data center processing rather than real-time edge inference on mobile systems.

> Summit data revealed that the most commercially successful robotics companies—spanning humanoids, warehouse AMRs, self-driving trucks, and construction automation—shared a common playbook:

1. They started by addressing a specific, high-pain labor challenge rather than pursuing general-purpose capabilities;

2. They adopted a 'Robotics-as-a-Service' (RaaS) model to lower customers’ upfront procurement barriers;

3. They prioritized safety and reliability over model complexity.

> According to Terry, recent returns on investment are being generated by task-specific AMRs and specialized platforms from firms like Locus Robotics and Dexterity, rather than highly publicized general-purpose humanoids. While humanoid robotics continues to capture substantial venture backing, the immediate financial upside remains firmly rooted in these dedicated, purpose-built systems.

This really resonates with what I discussed in my article. The training cost per hour runs at over $100. It's still to expensive. While the cost curve is becoming favorable, this area is mostly in a "hype" phase and will not see meaningful shipments until 3-5 years out.

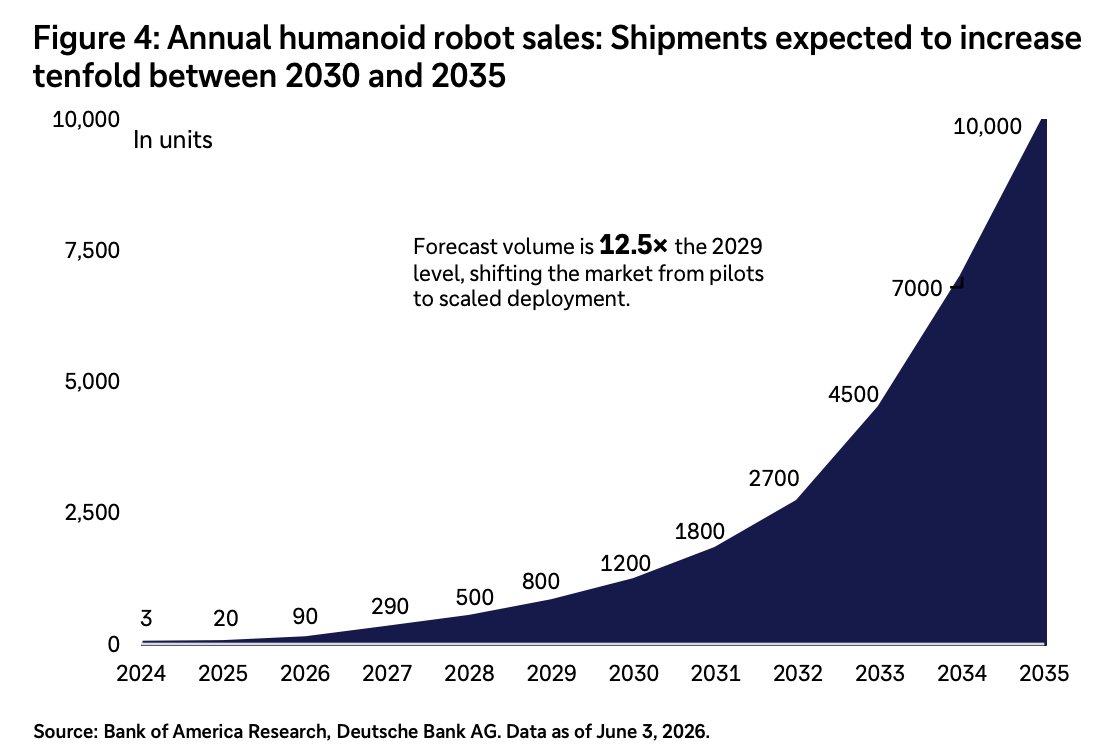

According to Deutsche Bank:

> Current Shipments: Global installations sit at roughly 2,500 units in 2026 (up from 500 in 2025), with broader autonomous deployment still largely unproven.

> Gradual Adoption Curve: Meaningful commercialization is pushed out to post-2027. However, a massive inflection is forecasted over the next decade: annual shipments are expected to jump tenfold, rising from 1.5 million units by 2030 to ~10 million units by 2035.

> Costs: Industrial systems currently cost between USD 50,000 and USD 250,000 per unit, while consumer models are trending below USD 25,000.

Technical Capabilities & Constraints

> Primary Barriers: Limitations are currently defined by hardware constraints—specifically power, dexterity, and reliability—rather than AI capabilities.

> Uptime Issues: Most platforms operate for closer to 4 hours rather than a full 8-hour shift, tightly constrained by battery density and actuator efficiency. Anatomy of

> Cost: Actuation systems (motors, drives, reducers) are the largest cost drivers, representing roughly 50% of total system costs. This makes upstream component suppliers a significant bottleneck.

Investment Implications

> The Ecosystem Play: Near-term investment value is skewed heavily toward "bottleneck technologies" and supply chain enablers (semiconductors, sensors, actuators) rather than the standalone robot brands. Over time, value and differentiation will shift toward software and AI.

> Capital Intensity: Humanoid-specific funding exceeds USD 8 billion across more than 100 companies, with top funding rounds capturing half of total investments.

> US vs. China: The US leads heavily in the intelligence layer (software, AI models, and simulation). China maintains a massive advantage in the physical stack, accounting for more than 4 out of 5 global humanoid installations in 2025 due to its deep supply chains and state-backed industrial policy.v

@StockDocEM Im over in Ontario Canada and I know a manufacturer here using their turbines.

They are broader than many realize. Another cool site they service is the Ronald Reagan presidential library

$QS I think it’s time for @QuantumScapeCo management and @ironmantimholme to start providing more material disclosure. The technology story is strong and the execution has been real, but the market cannot properly value what it cannot see.

We have been waiting forever for details on the pure-play EV OEM partner. Too much teasing and coy playing. Is it real or not? It’s not unreasonable for the market to disbelieve. Why do shareholders never get this information? The newer talk about U.S. military and data center applications falls on deaf ears without concrete plans behind it. I believe it is real but I’m also losing my patience.

Same with the partners who remain unnamed and the @VW PowerCo commercialization timeline that stays vague. Naming names, putting specifics behind the timeline, and adding color on the OEMs at the JDA stage would go a long way.

Shareholders have been overly patient, and the fundamentals justify far better communication than we are getting. Give us the disclosures the story has earned.

Thanks for your understanding.

“Energy storage solutions to help data center infrastructure handle load spikes, and subsecond scale GPU power fluctuations, is part of the 800 VDC architecture. Stay tuned for more details.”

QuantumScape’s Hidden AI Infrastructure Thesis $QS

Why the company’s AI infrastructure strategy could become a second multi-billion-dollar licensing platform

@PE72190 Hard to say without commercial agreements to forecast revenue. A long term hold.

On the bull case of AI TAM only ($100 share price is possible) not including other segments .

QuantumScape’s Hidden AI Infrastructure Thesis $QS

Why the company’s AI infrastructure strategy could become a second multi-billion-dollar licensing platform

@imnotharsh Hyper scalers are the end user. They need to understand their needs.

Then integrate their IP with the dominate infrastructure players and suppliers. (Nvidida, Delta, Etc)

The integration with OEM battery factories as EV companies pivot to stay competitive is a well timed move

$qs “This is what this agreement is about, turning technology into products”

“Honda Shifts EV battery Focus to Data Center Solutions” https://t.co/DOxFgSKSag

.@Honda R&D Co., Ltd. put our solid-state battery technology through rigorous evaluation. Now we're moving into a multi-year joint agreement together. Hear from QS CEO Dr. Siva Sivaram and Honda's Atsushi Ogawa on what's next. https://t.co/mnMZrqluiz

The first addressable market for $qs will be Data Centres. And that’s a not a bad thing at all.

The tech unlock will come through a TAM equal to the EV OEM market:

QuantumScape’s Hidden AI Infrastructure Thesis $QS

Why the company’s AI infrastructure strategy could become a second multi-billion-dollar licensing platform

If the AI strategy is validated through partnerships or commercial deployments, the market may begin pricing QuantumScape as a multi-vertical battery technology platform rather than a single-market EV company.

If realized, AI infrastructure could become a second multi-billion-dollar licensing platform alongside QuantumScape’s automotive business, leveraging the same capital-light licensing model across two independent end markets.