Some of the best interactions I’ve had here have been when my For You timeline ends up with Chinese or Korean or Japanese trading or tech content, or Japanese self-care/self-health (chill, do some movement, relax, be present)

There’s some quirk in physics where, if there’s a small hole in a bag of mulch it will leak all over your vehicle.

But if you rip a giant hole in the bag and try to dump it out into your landscaping, almost none will fall out.

A top quant lost his job due to an AI reasoning model replacing him at his company. He kept applying to different companies and tried his hand at macro writing but to no avail.

Eventually he swallows his pride and talks to his school friend who is now a plumber.

"I understand your old position was a finance maths guy. Why don't you come to our company and apply for a plumber position? You will earn half your old salary but the overtime and the union benefits make up for the rest. But remember, when you apply, tell them that you completed only seven elementary classes. They don't like educated people."

So it happened. The quant got a job as a plumber and his life significantly improved. He just had to seal a screw or two occasionally, and his salary was good enough and he had zero stress.

One day, the board of the plumbing company decided that every plumber had to go to evening classes to complete "basic financial literacy" certification. So, our quant had to go there too. It just happened that the first class was retirement planning. The evening teacher, to check students' knowledge, asked

“If you invest half your money in stocks and half in bonds, how do you calculate the portfolio return?”

The person asked was the quant. He jumped to the board, and then he realized that he had forgotten the formula. He started to reason it, and he filled the white board with He defined a filtered probability space (Ω, ℱ, {ℱ_t}, ℙ) and posited two correlated geometric Brownian motions for the risky and “risk-free” assets. He invoked the Radon-Nikodym derivative to switch to the risk-neutral measure ℚ, then switched back because the question was about realized returns, not prices.

He filled the whiteboard with stochastic discount factors, covariance matrices, CRRA utility functions, and pages of Itô calculus. He derived the wealth process under a self-financing strategy:

dW_t = W_t[(w R_s + (1−w) R_b) dt + w σ_s dB_t^s + (1−w) σ_b dB_t^b]

Then he solved the HJB equation for the optimal allocation, noted that Merton’s solution collapses to a constant weight under log utility, and circled w = ½ as the given constraint.

He invoked the linearity of expectation. He cited Markowitz (1952). He drew a small efficient frontier in the corner for context.

Finally, exhausted, chalk-dusted, eyes wild, he arrived at:

R_p = ½ R_s + ½ R_b

Then forty plumbers, in perfect unison, slammed their wrenches on the desks and roared:

“YOU FORGOT THE VOLATILITY DRAG, YOU FUCKING TOURIST!!”

The bitter lesson in 26 words:

Don’t be distracted by human knowledge, as AI has been historically.

Instead focus on methods for creating knowledge that scale with computation, like search and learning.

The coreutils Rust rewrite story is pretty funny.

Coreutils are tools like rm, mv, mkdir, etc. Unlike binutils, this isn't a fertile ground for memory safety bugs. But, the rewrite was completed, and in the spirit of progress, Canonical decided to switch.

🡇

REPORTER: You mentioned that, staying on as Fed governor, you intend to keep a low profile. Could you give us a little more detail on what that looks like?

JEROME POWELL: *ducks down*

It's up: https://t.co/7t1JT7w6nB

New puzzle every day. Guess the transform from the chart (winsorize, z-score, gaussian rank, lag, etc). Endless mode if you want to keep going.

Lmk what you think.

@experquisite@krobbn Thre is only one time zone: UTC. There is only one precision time: 64 bit nanos_utc (since epoch). There is only one date format, and it starts YYYY-MM-DD.

Love seeing people tackle equity perps in public.

The “arbitrage condition” in the last paragraph is well identified: the asymmetry of private gains but public losses (limited recourse + ADL mechanism) should be a familiar theme.

It also reflects the choice of pricing mechanism — a single, market-clearing rate that prices all risk collectively.

When risk is priced collectively but participants can take differentiated exposure, the rational move is to take more risk than the market-clearing rate prices.

Perp markets, by design, forgo idiosyncratic risk pricing. Without better mechanisms, credit quality deteriorates reflexively, and “sensible” leverage gets crowded out.

TradFi offsets that pressure through collateralisation, recourse, regulation, credit support, and counterparty-specific pricing — but even that fails sometimes (see Archegos).

None of these AI slop startups seem to be run by finance people, they are run by LLM people who don't understand that hedge funds don't just run pattern recognition on candlesticks, and don't appreciate the instability of distributions in financial data.

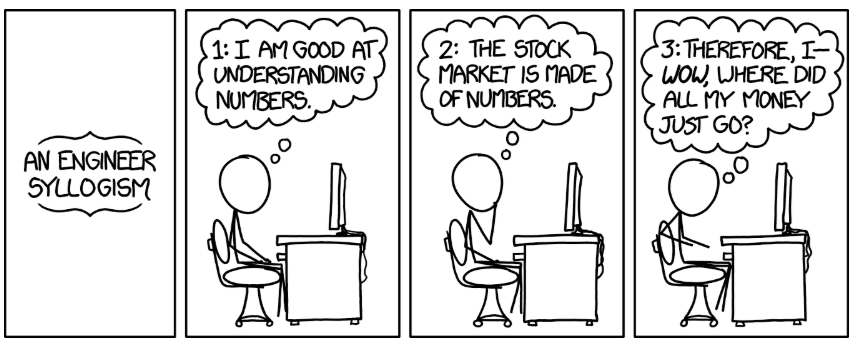

This xkcd is still true

Some day @Cboe and all of us will look back on this everything-is-a-casino era with embarrassment and disgust.

How institutions squandered decades of trust and probity by chasing degenerate gamblers with self-serving lies.

Just awful.

@liquiditygoblin@steiner_marwin Aah Orc I’d not thought of them for years…

Good to know re: splines, starting point for FAFOing got to be something relatively robust to idiot-usage first (or at least where it’s pretty easy to understand pointy edges / pathologies / etc). Will look at the think *hat tip*