$MMTLP

NEXT BRIDGE HYDROCARBONS

500 W. Texas Avenue, Suite 890

Midland, Texas 79701

432-684-0018

June 15, 2026

Dear Valued Shareholder,

Thank you for your inquiry regarding shares available through our recently effective S-1 offering. I sincerely appreciate your interest and your continued support of Next Bridge Hydrocarbons.

I want to personally apologize for the delays in this process. As many of you know, we have spent the past three and a half years navigating a complex and often challenging regulatory landscape. While reaching this milestone is an important achievement, there is still significant work ahead of us.

I respectfully ask for your patience as we continue working through the remaining steps. Our team is actively engaged on multiple fronts, and I believe we are approaching several important developments that I look forward to sharing with shareholders in the near future.

Your steadfast support, encouragement, and confidence in the company have helped carry us through an extraordinary journey. We do not take that support for granted, and we remain committed to acting in the best interests of all shareholders.

Thank you again for your patience and trust. I look forward to updating you soon.

Sincerely,

Greg McCabe

Chairman & Chief Executive Officer

Next Bridge Hydrocarbons

🦋⚖️ $MMAT / $MMTLP — Meta Materials Inc.

⚖️ U.S. Bankruptcy Court, District of Nevada

📄 ORDER ON MOTION TO QUASH

📅 Filed: May 27, 2026

⚠️NLA

🚨 BIG PICTURE — WHAT JUST HAPPENED?

Judge Gary Spraker just issued a MAJOR ruling against:

🏢 Citadel Securities

🏢 Virtu Financial

🏢 Anson Funds

These firms tried to QUASH (block) the bankruptcy trustee’s subpoenas seeking trading data tied to:

📈 $MMAT

📈 $TRCH

📈 $MMTLP

The Judge said:

❌ The subpoenas are NOT being fully thrown out.

✅ The trustee CAN obtain important trading records.

⚠️ BUT there will be strict protective-order limitations.

⸻

🧠 LAYMAN’S TERMS

The trustee believes there MAY have been market manipulation or wrongful conduct connected to Meta Materials trading activity.

The trustee is trying to determine:

🔍 Was trading activity harming the company?

🔍 Did it impact fundraising?

🔍 Did it damage the bankruptcy estate?

🔍 Are there potential legal claims worth pursuing before statutes expire?

The Judge basically said:

“The trustee has the right to investigate.” ⚖️

⸻

📌 THE COURT EMPHASIZED RULE 2004 IS VERY BROAD

The Court repeated that Rule 2004 examinations are basically:

🎣 “Fishing expeditions”

📂 Broad investigative tools

🔎 Used to uncover wrongdoing or estate assets

The Judge cited multiple cases saying trustees can investigate third parties to determine whether wrongdoing occurred.

⸻

🚨 HUGE PART — THE COURT ACCEPTED THE TRUSTEE’S THEORY ENOUGH TO ALLOW DISCOVERY

The trustee identified:

📊 11 separate “events”

where Meta or Torchlight allegedly:

💰 Sold treasury shares

📉 Issued dilution

📈 Raised capital

📄 Issued warrants/acquisition stock

during periods where the trustee claims trading manipulation may have affected pricing.

The Non-Parties argued:

❌ “Meta wasn’t actually selling into the manipulated market.”

❌ “The trustee lacks standing.”

❌ “This is too speculative.”

Judge Spraker was NOT persuaded enough to stop discovery. 👀

⸻

⚠️ VERY IMPORTANT — THE JUDGE DREW A LINE

The Court said:

🛑 This is NOT the stage where the Court decides whether Citadel/Virtu/Anson actually committed wrongdoing.

Instead:

✅ The trustee only needs enough justification to INVESTIGATE whether viable claims might exist.

That distinction matters A LOT.

⸻

👀 THE JUDGE ALSO SHOWED SOME CONCERN

This part is important.

The Court acknowledged concerns that:

⚠️ The trustee’s special counsel is involved in OTHER securities litigation against Citadel and Virtu.

⚠️ Rule 2004 discovery cannot simply become a shortcut for outside litigation.

⚠️ Discovery should benefit the bankruptcy estate — not unrelated lawsuits.

So the Judge imposed guardrails.

⸻

🔒 PROTECTIVE ORDER INCOMING

The Court ordered the parties to negotiate a STRICT protective order.

That order must:

🔒 Limit use of produced data -THIS bankruptcy

🔒 Limit use to trustee-related litigation

🔒 Restrict dissemination of data

🔒 Restrict access to trustee + approved professionals only

🚨 RESPONSE DEADLINE:

📅 June 18, 2026 — Protective order must be submitted to the Court.

⸻

🚨 BIGGEST DEADLINE OF ALL

📅 JUNE 25, 2026

The Judge ordered Citadel, Virtu, and Anson to PRODUCE:

📊 Market-wide trading data

📈 For the 161-day schedule identified by the trustee

📂 Under the Rule 45 subpoenas

unless modified by the protective order.

That is the MAJOR headline here. 🚨🚨

⚖️ WHAT THIS MEANS PRACTICALLY

The trustee now gains access to a significant amount of trading data that the Court believes may help determine:

🧩 Whether viable claims exist

🧩 Whether wrongdoing occurred

🧩 Whether the estate suffered damages

🧩 Whether litigation should be filed before limitation deadlines

This does NOT mean:

❌ Anyone has been found liable

❌ Manipulation has been proven

❌ The trustee automatically wins anything

BUT…

✅ The investigation survived.

✅ Discovery survived.

✅ The Court largely sided with allowing investigation over shutting it down.

SIGNIFICANT legal victory for the trustee!

🚨Breaking news: 🦋

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

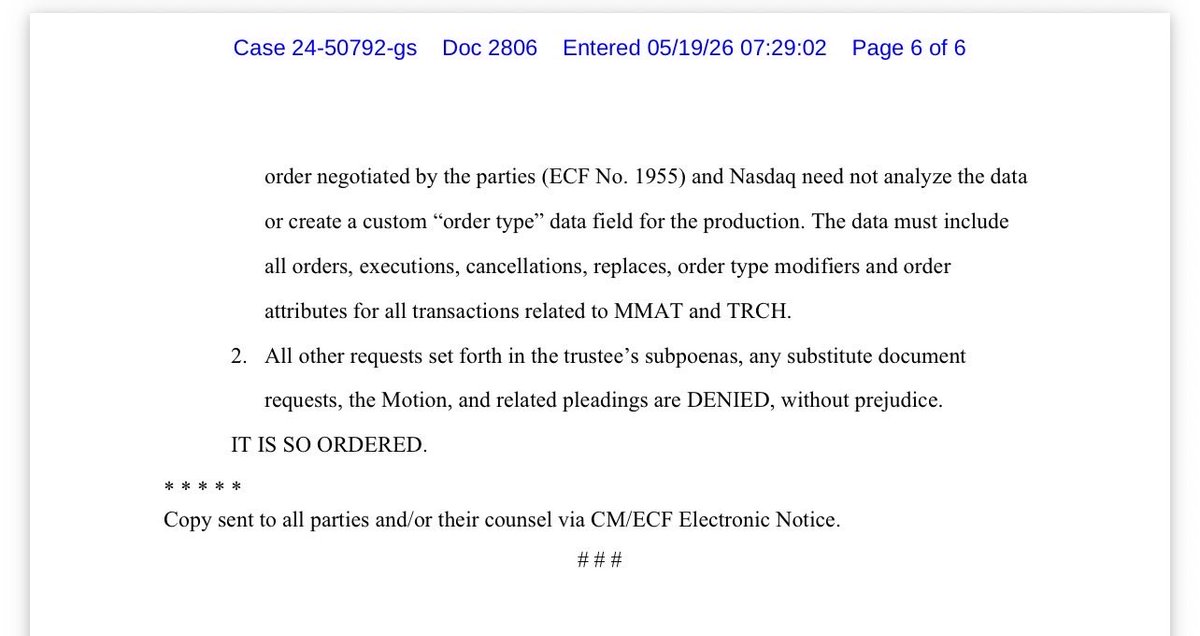

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

FINRA ORDERED BY JUDGE TO RELEASE 25 MILLION TRADING RECORDS, INCLUDING SHORT INTEREST DATA 🚨

MAJOR WIN FOR RETAIL & PUBLIC COMPANIES🏆

For the first time in history, a judge has ordered FINRA to produce 25 million trading records along with short interest data to determine whether the halt of $MMTLP was unjustified and expose if naked short selling occurred

This will shed light on how private equity and hedge funds may have coordinated activity that impacted retail shareholders

Repost to spread the word, this is huge🚨 $MMAT $GME $AMC $AVIS $BYND

META MATERIALS BANKRUPTCY PROCEEDING

Case No.: 24-50792-gs

U.S. Bankruptcy Court – District of Nevada

Hearing: FINRA Motion to Quash (Status & Scheduling Conference)

Date: March 17, 2026

Time: 1:30 PM (PDT)

Quick summary:

🧾 Big Picture (⚠️ Not legal advice)

This hearing is about whether FINRA has to hand over a large amount of documents/data to the Meta Materials bankruptcy trustee (Lovato).

•Other firms (Citadel, Virtu, Anson, Nasdaq) are already involved

•The judge is trying to coordinate all of these fights together

•The key issue:

👉 How much information FINRA has to give, and how hard it is for them to do it

⸻

⚖️ FINRA’s Position (Norris)

😭😭😭😭😭😭😭😭😭😭

FINRA is basically saying:

•“What the trustee is asking from us is WAY bigger than what they asked from others” 😭

•Other firms were only asked for:

•Limited trading data

•Short time period (160 days)

•But FINRA is being asked for:

•Emails

•Texts

•Internal communications

•Multiple categories of data (9+ categories)

👉 Their argument:

•This is too burdensome (too much work)😭

•Some of it is legally protected (privileged)

•They want:

•More briefing (extra legal arguments) (stall)

•A chance to argue this separately (stall)

⸻

🧑⚖️ Trustee’s Position (Burnett / Brust)

The trustee is pushing back hard: (Note - this was compelling and I think the Judge was agreeing)

•“We already argued all of this months ago” ‼️‼️

•“There are thousands of pages of filings already”

•“The judge has MORE than enough information”

👉 Their key points:

•FINRA already:

•Investigated market manipulation

•So their files are highly relevant

•The trustee has been trying to get this info for over a year ‼️‼️‼️‼️‼️‼️‼️

•Delays are:

•Costing money ‼️

•Risking statute of limitations deadlines‼️

👉 Bottom line:

•“Stop delaying—just rule already”

⸻

🔥 Key Dispute (This is the REAL fight)

It comes down to:

1. Burden

•FINRA: “This is huge and unfair”😭😭😭😭😭

•Trustee: “You’re different because you investigated this”

2. Scope

•FINRA = broad request (communications, internal files)

•Others = narrow (just trading data)

3. Privilege

•FINRA claims:

•Investigative files are protected

•Some data (like CAT data) legally cannot be shared

⸻

🧑⚖️ Judge’s Take

The judge is trying to balance both sides:

•Acknowledges FINRA is a bit behind compared to others

•Decides to allow:

👉 Short additional briefing (to be fair to FINRA)

But also:

•Clearly agrees with trustee that:

👉 “This needs to move forward and get decided”

FINRA asked for 2 weeks. The judge said no- 10 days.

⸻

📅 What Happens Next (IMPORTANT TIMELINE)

•FINRA submits extra argument (brief): March 27

•Trustee responds: April 3

•Hearing (big one):

👉 April 20 at 1:30 PM Pacific (4:30 PM Eastern) 💥💥💥

⸻

🎯 Why This Matters

This is actually a critical inflection point:

•If FINRA loses:

👉 They may have to turn over:

•Internal investigations

•Communications

•Potential evidence of market manipulation

•If FINRA wins or limits scope:

👉 A lot of key evidence could stay hidden

⸻

🧠 Simple Analogy

Think of it like this:

•Trustee: “Give me everything—you already investigated the crime”

•FINRA: “That’s like asking for our entire case file—it’s too much and protected”😭

•Judge: “Okay, I’ll give you a short chance to argue that—but we’re deciding soon” ⏰

Ticker: $MMAT

Case: In re Meta Materials Inc.

Date Filed: February 4, 2026

Document: Order Setting Status (Provided below)

Conference re: Litigation Financing

Not legal advice ⚖️

⸻

🧾 Layman’s breakdown

•💰 What this is about:

The bankruptcy judge wants answers about millions of dollars in litigation funding being used by the trustee’s legal team.

•📊 The amount:

Court records referenced about $11–$11.8 million arranged to fund legal actions tied to the bankruptcy.

•🤔 Why the judge stepped in:

The court says it’s unclear how this funding works and notes there doesn’t appear to be a formal motion asking the court to approve the financing under bankruptcy law.

•🧑⚖️ What the judge ordered:

A status conference (court check-in) is set for:

📅 February 20, 2026

🕘 9:30 a.m. 👀

to explain the funding and its terms.

•🧑💼 Who must explain it:

•The Chapter 7 trustee

•The trustee’s litigation law firms

•🎯 What they must address:

How the litigation money was arranged and the terms referenced in the legal contracts filed earlier in the case.

•💻 Attendance options:

Parties can attend in person or by Zoom/phone.

⸻

🧩 Why this matters (plain English)

•⚖️ The court wants transparency about who is funding lawsuits tied to the bankruptcy.

•💼 Litigation funding often signals major legal actions or investigations are being pursued.

•🔎 The judge is making sure everything is properly disclosed and approved before it moves forward.

⸻

Not legal advice. Just a simplified explanation of the court order.

https://t.co/4PxEgKzqAh

Recent disclosures tied to $MMTLP show internal communications between the SEC, FINRA, and the broker-dealer lobby (FIF) coordinating actions around unrecoverable loaned shares and effectively naked short positions.

For readers of InvestorTurf, this is not a revelation. It is validation.

In our prior investigation, “How Wall Street Creates Counterfeit Shares for AMC and GameStop,” we documented how U.S. market plumbing enables synthetic share creation through a closed loop of regulatory failures involving FINRA, the SEC, and the DTCC. The $MMTLP case fits that framework almost perfectly.

Our reporting laid out three core claims:

1. FINRA is structurally conflicted, acting as both regulator and protector of broker-dealers that fund it.

2. The DTCC tolerates chronic settlement failures, allowing phantom shares to persist under the cover of “fails to deliver” and netting mechanics.

3. The SEC consistently defers enforcement, choosing market stability and institutional protection over rule of law and investor protection.

The $MMTLP halt exposed the endgame of that system. When naked short positions became mathematically impossible to close, trading was stopped, not to protect investors, but to prevent forced buy-ins that would have exposed the scale of counterfeit share issuance.

That outcome is not an accident. It is the logical conclusion of regulatory capture.

Why This Was Inevitable Under Gensler

Gary Gensler’s SEC has repeatedly promised reform while presiding over the same outcomes:

• Record settlement failures

• Token fines treated as a cost of doing business

• No criminal referrals tied to systemic naked short selling

If internal communications show regulators coordinating with industry lobbyists while retail investors were locked out of the market, that raises a fundamental question: who is the SEC actually regulating?

InvestorTurf has long argued that the SEC does not function as an independent watchdog, but as a pressure-release valve, stepping in only to manage optics and contain risk when the system threatens to expose itself.

The Legal Implications

If regulators knowingly facilitated or concealed market manipulation, the issue moves beyond incompetence. Conduct of this nature, if proven, would fall under federal criminal statutes, including:

• 18 U.S.C. § 371 — Conspiracy to defraud the United States

• 18 U.S.C. § 1348 — Securities and commodities fraud

• 18 U.S.C. § 1001 — False statements or concealment within federal jurisdiction

• 15 U.S.C. § 78j(b) and Rule 10b-5 — Market manipulation and fraud

These are not abstract theories. They are the exact statutes designed to address coordinated deception in U.S. financial markets.

The InvestorTurf Conclusion

The $MMTLP disclosures do not represent a breakdown in oversight.

They represent how the system is designed to function when naked shorts become too visible.

FINRA shields.

The DTCC obscures.

The SEC delays.

And retail investors are told to trust the process.

If senior officials were aware of unrecoverable synthetic positions and acted to suppress price discovery rather than enforce the law, then accountability must go beyond hearings and resignations. Criminal investigation is the minimum threshold.

Markets cannot survive when regulators protect the counterfeiters.

InvestorTurf has been documenting this pattern for years.

$MMTLP didn’t expose something new.

It exposed what regulators were willing to do when the truth got too close.

$MMAT

⚖️ Meta Materials Bankruptcy Trustee Responds to Citadel, Anson Funds, and Virtu - 1/20/2026:

(Breakdown in layman’s terms. Not legal advice.)

⸻

1️⃣ What the Court Asked the Trustee

The bankruptcy judge asked one narrow question:

Can the Chapter 7 Trustee, standing in the shoes of Meta Materials (MMAT), pursue claims that would be informed by the trading data sought through Rule 2004 subpoenas?

The Trustee’s answer is unequivocally - YES.

⸻

2️⃣ Trustee’s Core Position (Big Picture)

The Trustee argues:

•She is lawfully investigating potential market manipulation

•The subpoenas seek basic trading data

•That data may reveal claims belonging to the bankruptcy estate

•This is exactly what Rule 2004 discovery is for

•The hedge funds are trying to stop discovery before facts are known

In short: You don’t shut down an investigation just because powerful non-parties don’t like where it might lead.

⸻

3️⃣ Can a Company (or Trustee) Sue for Market Manipulation?

Yes. Repeatedly confirmed by courts.

The Trustee explains:

•Corporations can be “sellers” under securities law

•If manipulation depresses the stock price while the company is issuing or selling shares, the company is harmed

•A bankruptcy trustee inherits that right and can sue on behalf of the estate

She cites multiple federal cases confirming this, including:

•Northwest Biotherapeutics (spoofing depressed price during issuer sales → viable claim)

•Profilet v. Cambridge Financial (trustee can bring Rule 10b-5 claims)

•Supreme Court precedent recognizing corporate standing

This is not a novel theory—it’s established law.

⸻

4️⃣ Why the Hedge Funds’ Arguments Fail

The hedge funds (Citadel, Virtu, Anson) argue:

•MMAT supposedly wasn’t a “seller”

•Any fraud was MMAT’s own fault

•Other cases used public data, so discovery isn’t needed

•The Trustee should already know enough to plead claims

The Trustee responds bluntly:

•❌ These are merits arguments, not discovery arguments

•❌ This is not a motion to dismiss or summary judgment

•❌ Trustees do not start with full knowledge

•❌ You can’t demand proof before allowing investigation

She calls their arguments premature, unsupported, and procedurally improper.

⸻

5️⃣ Why Rule 2004 Discovery Is Appropriate

The Trustee explains the purpose of Rule 2004:

•It allows a trustee to investigate first

•To determine:

•What happened

•Who was involved

•Whether claims exist

•Courts explicitly reject forcing trustees to plead claims without discovery

She cites bankruptcy cases warning against “shutting down investigations” based on speculation or fear of liability.

Key point:

Rule 2004 exists so trustees don’t have to guess. 🔥

Blocking it would invert bankruptcy law.

⸻

6️⃣ What Claims Could Be Uncovered

The Trustee makes clear she is not accusing anyone yet, but discovery could reveal:

•Securities fraud (spoofing / manipulation)

•Unjust enrichment

•Breach of fiduciary duty

•Naked short selling

•Professional malpractice (if others enabled fraud)

She emphasizes:

She may never bring a lawsuit — but she cannot know that until discovery occurs.

🎯 That uncertainty is the justification, not a flaw. 🎯

⸻

7️⃣ Why the Hedge Funds’ Resistance Matters 🤨 🧐 🤔

The Trustee subtly but pointedly notes:

•The hedge funds are refusing to provide basic trade data

•Data that is routine in market-manipulation cases

•Their resistance itself suggests the discovery is meaningful 👀

This isn’t about burden — it’s about avoidance.

⸻

8️⃣ Trustee’s Bottom Line

The Trustee asks the Court to:

•Reject the motion to quash

•Reject attempts to litigate merits early

•Allow Rule 2004 discovery to proceed

•Let the investigation continue as bankruptcy law intends

Plain English version:

Let me do my job. Don’t let non-parties shut down an investigation before facts are known.

⸻

https://t.co/SBrW719SDj

$MMTLP

Why was award winning journalist Dennis Kneale’s @X account shut down - is it because he’s been exposing market manipulation?

When I asked if X suspended his account Dennis replied “Permanently!! Denied appeal.”

What is going on @support?

The irony of this considering Dennis published a book on @elonmusk leadership last year.

@palikaras

FOIA, especially for SEC Enforcement, is no longer a purely an “in house transparency function”.

It is an operational pipeline that can be influenced by vendor economics, tool design, contractor staffing, and risk posture.

1) FOIA, what it became over time, and why it creates leverage points

FOIA (enacted 1966, effective 1967) created a right to obtain agency records, subject to exemptions, with courts empowered to review withholding decisions.

FOIA gets “teeth” and process layers

Post Watergate reforms strengthened timelines, standards, and judicial review, FOIA becomes a real compliance machine, not just a principle.

Later reforms emphasized a “presumption of openness” and the “foreseeable harm” standard, limiting withholding to cases where an agency can reasonably foresee harm or where disclosure is barred by law.

The OPEN Government Act created OGIS (FOIA ombuds), adding a dispute resolution and oversight layer.

FOIA operational reality TODAY:

FOIA is now a high volume production workflow, requests come in, triage, search, redact, apply exemptions, negotiate scope, litigate. This creates natural pressure to standardize and outsource.

2) FOIA industrialization, software platforms, and outsourcing to private equity funded companies who also control broker dealers and the factual data backbone.

FOIA workflow tools TODAY:

A large portion of federal FOIA case processing is handled through commercial platforms like FOIAXpress, which markets itself as FOIA/Privacy Act case management, including tracking, correspondence, redaction, reporting.

AINS rebranded to OPEXUS, and its FOIA tooling is positioned as core GovTech infrastructure.

I wonder... who owns AINS and who OPEXUS...?

Private equity ownership of AINS/OPEXUS:

1. Gemspring Capital acquired a majority interest in AINS (the company associated with FOIAXpress), meaning FOIA workflow infrastructure can be controlled by PE incentives (growth, margin, upsell, renewals) while still embedded inside government.

2. OPEXUS is majority-owned by the private equity firm @thomabravo , which acquired it as part of a 2025 transaction in which OPEXUS merged with Casepoint.

wait... they ALSO own Casepoint?

What Casepoint does:

Casepoint offers an end‑to‑end platform for legal hold, data collection, processing, review, and production, focused on litigation, investigations, regulatory matters, and FOIA/public records workflows.

Its system is used to manage large, multi‑source datasets securely at enterprise scale, with built‑in analytics and active learning to accelerate document review and surface relevant information

FYI, Thoma Bravo is one of the world’s largest software-focused private equity firms, managing over about 181 billion USD in assets across more than 75 portfolio companies and they just raised a new $24.3 Billion private equity flagship fund. https://t.co/mYgYunrk53

Ownership structure

Thoma Bravo holds a majority stake in the combined Casepoint–OPEXUS company following its acquisition of OPEXUS from Gemspring Capital and its investment in Casepoint.

Corporate setup

The combined company operates under the OPEXUS/Casepoint platform, is headquartered in Washington, D.C., and is led by OPEXUS CEO Howard Langsam, with Casepoint co-founder Vishal Rajpara on the executive team.

SEC contracting for FOIA support:

SEC procurement documents show FOIA handling support contracts, including C2 Alaska and Fors Marsh Group, appearing in SEC “Contract Payment Justifications,” explicitly describing FOIA support for Enforcement and other SEC functions.

USAspending shows @SECGov awards to C2 Alaska. The real ownership is listed above.

So there it is.... dear @SECPaulSAtkins, if you truly want to reduce the cost of your OPEX digital services (reading your recent comments https://t.co/oyLrk8KPJI):

1. You may wish to contact the ThomaBravo member who sits on the OPEXUS Board, and is mandated by his private equity investment thesis and LPs, to squeeze every $$$ dollar out of you, because your SEC organisation is #HOSTAGE to a SINGLE SOURCE supplier, who is controlling directly and indirectly your software stack and perhaps the quality of the service...

2. You may wish to incentivise competition with blockchain tech if you desire to break free from such a monopoly or bring it all under in-house control.

Best of luck. I have lots of faith in your leadership since @POTUS entrusted you, and certainly, we are getting a lot more transparent access to #MMTLP information during your administration. More is needed, especially Gensler's "lost" cellphone messages. THANK YOU!

Last but not least.

Today, January 12, 2026, MMTLP/MMAT shareholders went to the headquarters of the U.S. Securities and Exchange Commission in Washington, D.C. to place a historic market failure formally on the record.

A U3 trading halt and the sudden disappearance of an active market left an estimated 65,000 investors trapped, with no price discovery, no orderly exit, and no clear remedy.

This was not a normal “risk of trading” event. It was regulator-driven.

We now have documented evidence showing how the financial “musical chairs” began before the merger of #TRCH and #MMAT, and before #MMTLP trading even commenced, involving broker-dealers that have yet to be officially named by FINRA.

Led by the tireless @annvandersteel, and supported by American Made Action team, shareholders stood outside @SECGov headquarters to demand three simple, lawful things (among other important asks):

1️⃣ A full, independently audited reconciliation of all issued shares and short positions in #MMTLP.

2️⃣ Disclosure of internal communications between the SEC, FINRA, and market intermediaries relating to the halt and the corporate action.

3️⃣ Public hearings and a DOJ investigation into how this was allowed to occur, including potential regulatory capture and conflicts of interest involving market infrastructure and intermediaries.

This is now part of the historical record.

Retail investors did not stay silent. For more than three years, they have shown up, documented everything, preserved evidence, and asked only for lawful redress.

To @USHouseFSC and @FinancialCmte, this is now squarely in your remit. We are asking you to do your job. Investigate. Subpoena where necessary. Establish accountability. And ensure this never happens again.

In any case...we soon plan to level the playing field, with, or without you. #BlueLedgerAI

Hey @RealAlexJones; are you paying attention, yet?

The #MMTLPARMY are the true, modern day Paul Reveres.

This family of ~100,000+ Investors turned Investigators didn't ask for this but we have had no choice but to take our own initiatives to rally support to get to the bottom of it.

3 years and counting...

We are not going away until this resolved!

@OwenShroyer1776@HarrisonHSmith@realchasegeiser

I hope one of you can see this and flag it to Alex right away! THANK YOU FOR YOUR ATTENTION TO THIS MATTER! The General has spoken!

MMTLP

I need every retail investor no matter what stock/company you’re invested in to REPOST the post below 👇

Click the post 1st, than repost it

SPREAD THE WORD🚨🚨

THIS IS BIG!!! $MMTLP $AMC $GME $GNS $QNTM $BYND $BBBY