Today is the last day to join before the group closes to new members. Join here now 👇

https://t.co/TjbTys1lfq

Or add me through my profile and send "1". The biggest gains usually happen before a stock becomes popular. Once everyone is talking about it, most of the easy money has already been made. Over the past 3 months, our group has delivered returns exceeding 50% per month through disciplined execution, timing and risk management. No chasing headlines. No random stock picks. Just real market opportunities shared as they develop. Many members have already seen significant gains, and the remaining spots are filling quickly. If you want access before the next wave of setups starts attracting attention, this is your opportunity.

#Stocks #Trading #Investing #StockMarket #AIStocks

$MRVL is up 9.39% over 14h to $307.50, reclaiming most of yesterday's profit-taking flush on no fresh catalyst. The dip got bought right at the post-Computex base — buyers stepped back in well above the mid-$160s breakout after the stock gave back from its ~$324 ATH to near $298. The Teralynx T100 switch and Huang's 'connectivity is the next bottleneck' call are still the whole trade; this just says the forced sellers from the flush are done, not that there's a new bid.

Tradeable with up to 10x leverage.

Hyperliquid.

NEWS: Fidelity is opening the SpaceX IPO to any customer with at least $2,000 in a retail brokerage account, down from as much as $500,000 for previous offerings.

The reason, per Fidelity's own FAQ, is that SpaceX reserved up to 30% of the offering for retail investors. Typical IPOs set aside just 5% to 10%.

Customers can request anywhere from 1 share to 1 million shares. If demand outruns supply, Fidelity will run a lottery to spread allocations as fairly as possible.

One warning for flippers. Selling allocated shares within 15 days of trading brings a 6 month ban from future IPOs at Fidelity. A second flip brings 1 year. A third is permanent.

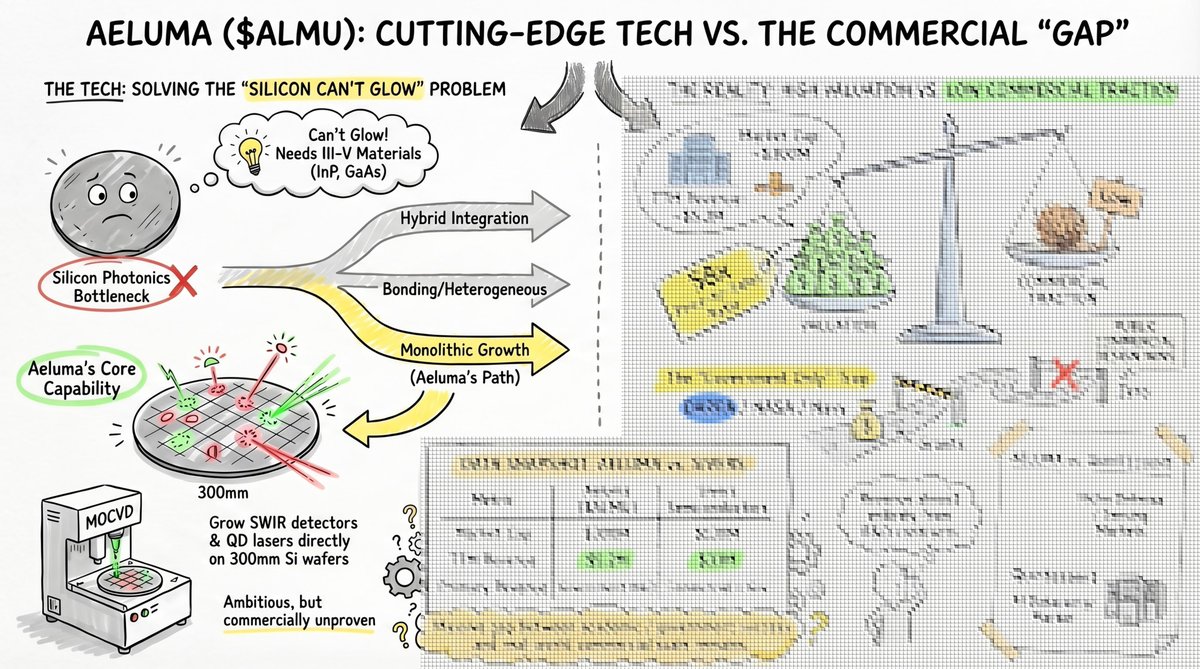

$ALMU surged 40%+. The technology is real. But one question remains.

Of the $5M in revenue, how much comes from commercial customers?

What this article covers:

- Three methods of III-V on Si integration and where Aeluma actually sits

- Quintessent vs Aeluma: different technology, different market

- What the Bowers signal actually means

- The $4M contract in context, and why it does not justify a 40% move

- What I learned visiting the booth at Photonics West in person

- P/S 58x valuation broken down by scenario

$50M ATM + insider selling pattern and what it signals

- Five monitoring points: what to watch next

The real signal: The problem is not whether the physics works. It is who is buying outside of government.

Broadcom beat earnings and the stock fell about 13% anyway. I called the beat on the record, so here is the grade.

The prediction landed. Earnings came in at $2.44 against the $2.40 consensus, and AI chip revenue hit $10.8 billion, both above the bar I set. The part of the call that decides the stock was the guidance, and that is where the market got picky. I expected management to raise the path past $100 billion of AI revenue in 2027. They reaffirmed it instead of lifting it, and for a stock that ran up roughly 48% into the print and was priced for a flawless quarter, reaffirmed was not enough. The buyers who chased it ahead of the number took profits.

I flagged exactly this in the original call: even a clean beat can spark a knee-jerk drop if they only repeat the existing guidance, and I would read that as noise against a multi-year buildout. I still do. AI silicon grew 143% year over year and next quarter is guided to $16 billion, more than double a year ago. A company compounding like that does not lose its thesis on one night of profit-taking. I am holding, and I will take the scorecard.

Grading my own call in public, not handing anyone a trade.

🚨 Leopold fund went All-in on Neoclouds for same reason !!

“Compute through 2027 is sold out.” — OpenAI CFO confirmed on @theallinpod

“If you do not have compute, you do not have revenue.”

OpenAI is passing on opportunities RIGHT NOW because of the shortage.

📝Market prices AI infrastructure on a 2-year horizon.

OpenAI buys on 6 year conjecture 📈

Where she feels most SHORT: 2030, 2031, 2032.

⛔️A single GW-scale data center = $50B + 3 years to build.

The plays ?

The named proxies: $ORCL $CRWV $NVDA

But the real constraint? Power and land.

The neocloud stack I’m watching:

🔲 $CRWV — $99B backlog, OpenAI + Meta locked in, take-or-pay contracts

🔲 $NBIS — AI-native cloud, NVIDIA partnership, 5GW target by 2030

🔲 $IREN — Direct NVIDIA cloud-services contract, DSX partnership

🔲 $APLD — Power + campus execution play, CoreWeave as anchor tenant

🔲 $ORCL — Hyperscaler with long-dated AI contracts

The market is still pricing this on a 2-year lens.

The CFO of the most compute-hungry company on earth is buying on a 6-year lens.

💵 That gap is the trade !!

$IONQ “The first project that we are working on is with a very large bank,” she stated. “This is around QKD. If you are a financial institution, keeping data safe is very important.” At this point we all know it’s JP Morgan right 🤣

https://t.co/4oCt8EP2Dd