@brandonjcarl What useful life or OpEx assumption are you getting to flat / negative GMs? I think can get to ROICs penciling to 12-15% if you assume a 35% GM which you can check two ways: AWS GM and my own math assuming 3rd party operator numbers power cost/server depreciation/DC lease OpEx

The market is currently saying two things that can't be true at the same time: (i) consensus estimates for hyperscale CapEx asymptoting at ~$1Tn annual spend and (ii) consensus estimates in the aeros/recips market implying hyperscale CapEx of ~$2.5Tn annual spend. Who is right?

My simple, chimp brain guess is that the sector with ~$12.5Tn in combined market cap has more research budget to figure out what the right number is than the sector with ~$1Tn combined market cap

Welcome to the most asymmetric trade in modern financial history.

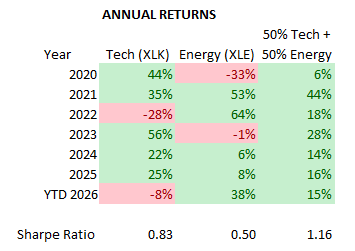

The thread below lays out why. The opportunity exists because capital has chased the AI trade while ignoring the physical assets AI requires to run — assets that have quietly become the best-performing asset class of the decade. Since October 2020 when we first called for the commodity super cycle: QCI Total Return +217%, GSCI Total Return +205%, Gold +140%. NASDAQ trails at +130%. S&P 500 at +85%. The top three are all commodities. Yet oil cannot get out of its own way while copper and the broader atom complex prints fresh highs . That is the dislocation. That is the trade.

Get long. Buckle in. Hang on for the ride.

Forgive the longer posts in this thread — attempting to mimic my old 10-bullet commodity takes. On to it.

Right ... we're going to spend $1.5 trillion across servers and infrastructure annually starting 2027 and 100% of the ~700K non-res electricians in the US (of which only ~200K are industrial/DC trained today) to build data centers. If it seems retarded, is it retarded?

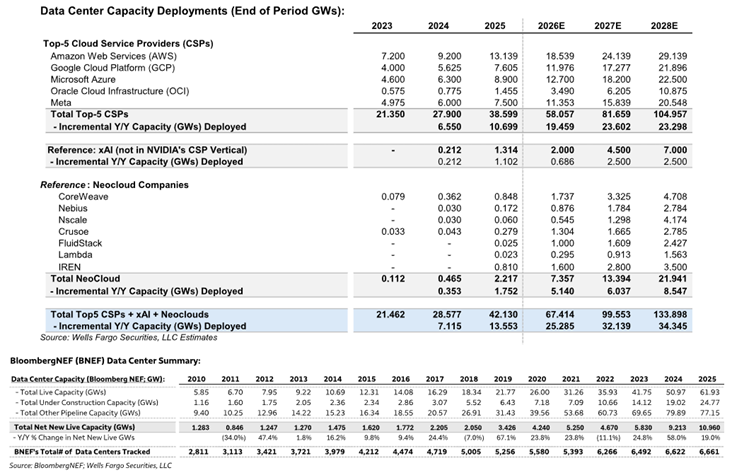

Current and forecasted data center capacity deployments in GWs by company:

Overall, by the end of 2026, 25 additional GW are expected to be deployed. By year end ’27 there should be an additional 32 GW, and by year end we should see an incremental 34 GW, bringing totals to about 134GW across hyperscalers and neoclouds per Wells

Not sure how people didn't see this coming from a mile away. When someone IPOs with no permits, no contracts, no near term slot reservations, or power development experience ... they're not serious people.

Last October, Fermi Inc. was sizzling. It raised $746 million in an IPO and was planning to build 11 GW of power generation for AI data centers. But Fermi’s sizzle has turned to fizzle. (Article linked below in comments.) My latest:

Overton window is definitely shifting. Oil & gas decline curves are way shallower than you might think - and the overbuild boom from Shale era is fading with real people managing ever growing conglomerates which have self reinforcing benefits of scale - FCF growth coming.

Food for thought.

The Six Weeks That Killed Climate-First Politics

The past six weeks have done what a decade of speeches could not: they have ended the fantasy that climate targets can sit atop the commanding heights of industrial policy.

Two shocks did the work. Iran turned the Strait of Hormuz from a taken‑for‑granted shipping lane into a visible weapon, proving that a single revisionist state can intermittently hold a material share of global oil and gas flows at risk with drones, missiles and maritime harassment.

The old assumption, that U.S. naval power would quietly underwrite open sea‑lanes, has been exposed as nostalgia. Pax Americana, in energy terms, is over.

At the same time, AI has revealed itself as what it truly is: a horizontal general‑purpose technology, akin to electricity, that will permeate every sector. Data centres and chip fabs are not metaphors; they are industrial plants with energy appetites measured in gigawatts and cooling needs measured in rivers. An economy that wants AI‑driven productivity cannot be run on fragile, intermittent power systems designed to flatter climate metrics rather than maximise resilience.

Donald Trump’s return to the White House is the political forcing function that strips away the pretence. Whatever one thinks of him, his administration is explicitly re‑ranking priorities: energy dominance, reshoring, and hard security first; climate as a constraint, not a veto. He is saying in public what many officials in other capitals still only admit in private.

Put all this together and the conclusion is unavoidable. The world can no longer afford an industrial strategy where “climate alignment” routinely vetoes resource projects, pipelines, mines, grids and nuclear plants while assuming someone else will keep the molecules and electrons flowing. The era in which climate change drove industrial policy ended about six weeks ago. Energy and resource security are back at the top of the pyramid; the only question is how long it will take other leaders to say so out loud.

We're excited to announce 'The Situation Room' by Polymarket is coming to Washington, D.C.

The world's first bar dedicated to monitoring the situation. 🧵