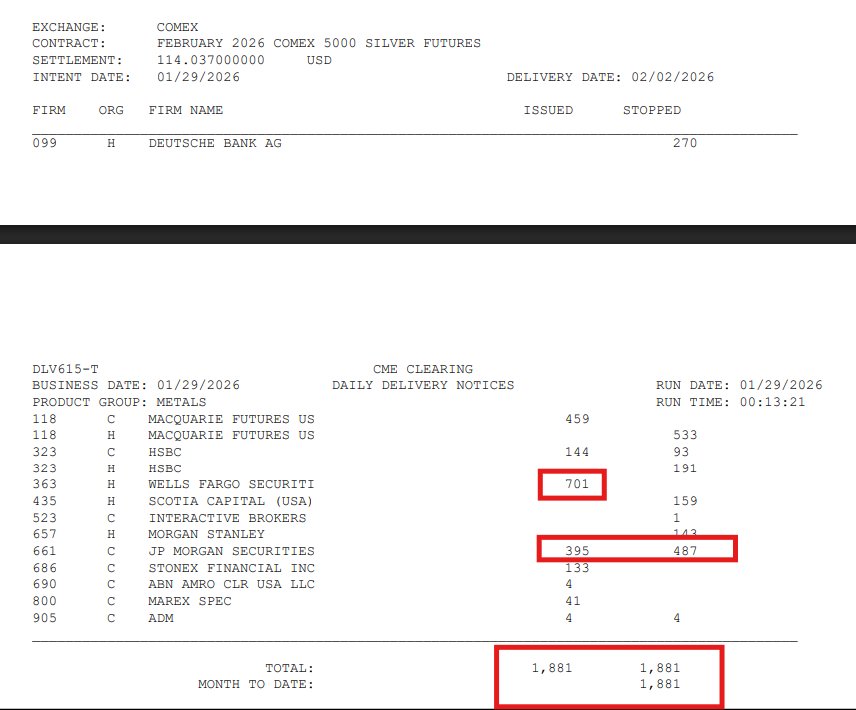

Intent day was 29 Jan 2026.

Delivery date: 02 feb 2026

Silver then crashed ~31% on Friday, 30 Jan 2026.

Despite that crash, these contracts still stood for delivery, with allocation scheduled for 02 Feb 2026 (T+3).

So the decision to take physical was made before the crash, and it was not reversed after the crash.

That tells you this was not momentum chasing or panic buying.

It was conviction.

Paper price collapsed.

Physical intent stayed firm.

That divergence is the signal.

These photos from about 8 years back show the building is real and is their main manufacturing site, but the physical infrastructure and visible operations do not support the astronomical revenue figures reported in FY2015.

This facility does not look like a place that was exporting ₹50,000 crore (~$8 billion) worth of gold/jewellery in FY2015.

nothing about it screams “massive global operation handling billions in gold volume.”

Why the Scale Doesn’t Match ₹50k Cr Revenue

Physical output limits: Even at full claimed capacity (~250–350 tons of jewellery p.a. across facilities), the realistic annual output value at 2015 gold prices would be roughly ₹7,000–12,000 crore max — far below the reported ₹50,463 crore revenue. The rest had to come from bullion trading/pass-through exports, not manufacturing inside these walls.

Why Yields Haven't Spiked: RBI's Role

The Reserve Bank of India (RBI) has actively supported the bond market through large-scale OMO purchases of government securities. This injects liquidity and directly increases demand for bonds, which pushes bond prices up and yields down (or prevents them from rising sharply).634075

Key evidence:

RBI has absorbed a massive portion of government borrowing via OMOs in FY26 — reportedly nearly half of the Centre's bond issuances in some periods. This has involved trillions of rupees in purchases to maintain liquidity.7c2015

Record interventions: In late 2025 into 2026, RBI conducted large OMO buys (e.g., ₹1 lakh crore+ in single announcements, cumulative purchases in the trillions). This was stepped up amid market stress from global events.

Liquidity support: Beyond spot forex intervention (selling dollars to defend the rupee, which has depleted reserves somewhat from peaks near $728B to ~$680-700B range), RBI uses OMOs, forex swaps, and other tools to ease domestic funding pressures.

This bond-buying offsets selling pressure from FPIs and keeps yields from spiking, even as the RBI manages the rupee separately (via reserves and regulatory curbs on speculation, like position limits for banks).

They all did their deepest work in solitude.

Darwin walked alone. Shakespeare observed alone. Dickinson wrote almost entirely alone. Edison experimented for endless hours alone.

The common thread:

They gave themselves space.

Away from noise. Away from approval. Away from the crowd.

Great minds do not only need talent.

They need silence.

That is why Japanese 7-Elevens feel strangely intelligent.

His philosophy was: “Don’t sell products. Solve daily friction.”

He also had immense discipline.

Accounts describe him as extremely detail-oriented, demanding, relentless, and obsessed with continuous improvement. He was nicknamed “Hurricane Suzuki” because of his intensity.

Registered COMEX silver is around 82 million oz.

July open interest represents roughly 1.8 billion paper oz.

Shanghai inventories are rising.

Shanghai premiums are still near 10%.

That means metal is moving toward the buyer willing to pay more.

If silver was truly abundant, China would not need to pay such a premium.

The West is still pricing silver like a paper commodity.

The East is treating it like a strategic physical metal.

That gap is the real story.

@honzacern1 First countries bought gold.

Now they are building the infrastructure to clear, store, and price it outside the old Western framework.

That is the real signal.

That is what happens to banks.

They may not be “insolvent” immediately, but their earnings power weakens.

The dangerous sequence is:

Old bonds earn low interest

Depositors demand higher interest

Bank profit margin shrinks

Depositors may withdraw money

Bank may need cash

Bank sells bonds

Unrealized loss becomes real loss

@FirstSquawk Very simple version:

Stocks say: “There is more money in the system.”

Gold and silver say: “People are afraid that money is losing value.”

@Kalshi But the question is:

Will the market rise because the economy is truly strong?

Or because policymakers are forced to keep liquidity flowing?

That difference matters.

One is growth.

The other is debasement.

The U.S. SPR is being drained again.

Recent data shows a roughly 9.9 million barrel weekly draw, described as a record withdrawal.

That means America is tapping its emergency oil savings account.

This can suppress oil prices short term.

But it also tells you something deeper:

The physical oil market is tight.

If emergency reserves are needed just to calm the system, then the real stress is not over.

Oil stress means inflation risk.

Inflation risk means more pressure on currencies.

And that is why hard assets like gold and silver remain important.

@infraa_ The U.S. money-market cushion is almost gone. Reverse Repo fell from ~$2.4T to near zero. Now every funding shock shows up directly in SOFR/repo stress. The system is not broken today — but it has lost its shock absorber. Hard assets will notice.

@grok@b2wicey@SawyerMerritt **Financials (adjusted for merger/stock split):**

- 2025 revenue: $18.7B; net loss: $4.9B

- Q1 2026 revenue: $4.7B; net loss: $4.3B

Starlink is profitable and growing fast; heavy capex in Starship and AI (data centers + future orbital compute).

how is it profitable?

This is the Jevons paradox in AI.

Everyone thinks efficiency will reduce power demand.

But in reality, better efficiency makes compute cheaper and more powerful, so companies build even bigger data centers.

A 30-40% efficiency gain does not mean less electricity use.

It means the same electricity can run more AI.

Then demand expands from 100 MW sites to 500 MW, 1000 MW and even 1500 MW campuses.

So efficiency does not kill the power boom.

It accelerates it.

Bullish for power, transformers, switchgear, copper, silver, cooling, backup systems and grid infrastructure.

Silver in India may rise faster than global silver.

Why?

Because India is not just exposed to global silver prices. It also has its own supply problem.

If imports are restricted and duties rise, the landed cost of silver goes up immediately.

So even if COMEX silver pauses, Indian silver can still become more expensive because buyers face shortage, duty, GST, rupee weakness and physical premium.

Global silver price is the base.

India-specific shortage is the extra fire.

Yes, in simple terms:

Point 3 and 4 mean silver can become more expensive in India even if the international silver price does not rise much.

Why?

India needs silver for jewellery, investment, solar, electronics and industry.

But if imports are restricted and import duty is increased, then less silver enters India and the landed cost becomes higher.

So Indian buyers may have to pay a premium over global prices.

Simple analogy:

Global silver price is the base price.

Import duty, restrictions, GST, rupee weakness and shortage are extra layers added on top.

So the Indian silver price can rise because of two forces:

1. Global silver price rising

2. India-specific shortage, duties and restrictions

That is why silver in India can become costlier faster than silver in London or New York if supply tightens.

USD/INR is around 96.4.

For silver in India, this is not a 2-engine story.

It is now a 4-engine story.

Engine 1: Global physical silver shortage.

Engine 2: Rupee depreciation, making every imported ounce costlier.

Engine 3: India has restricted key silver imports.

Engine 4: India has raised gold and silver import duties to 15%.

This is important.

Even if global silver pauses in dollar terms, Indian silver can still move higher because the local market is facing currency weakness, higher import cost, tighter approvals, and limited supply.

This is how a global shortage becomes a domestic squeeze.

Silver in India is no longer just an investment story.

It is becoming a supply, currency, and policy story.

Adani is legally bound to pay the $275 million OFAC settlement.

But the $10 billion U.S. investment appears to be a pledge or political commitment, not clearly a court-enforceable penalty.

That makes the optics even more interesting.

A formal fine on one side.

A huge investment promise on the other.

Then cases are settled or dropped.

Legally, they may say there is no admission of guilt.

Politically, it looks like power negotiating with power.

Discretion in resource allocation” is polite legal language.

It means:

“We have limited government resources, and we are choosing not to spend more time and money prosecuting this case.”

It does not prove innocence.

It does not prove guilt.

It means the state decided not to continue.

The interesting part is the optics.

A $275 million settlement.

A separate $10 billion U.S. investment pledge.

Then criminal charges are dropped.

If the $10 billion is only a pledge, he may not be legally bound to complete it.

But if he backs away, the legal risk may be limited while the political and reputational cost could be huge.

This is how power works.

Small people face law.

Big people negotiate outcomes.

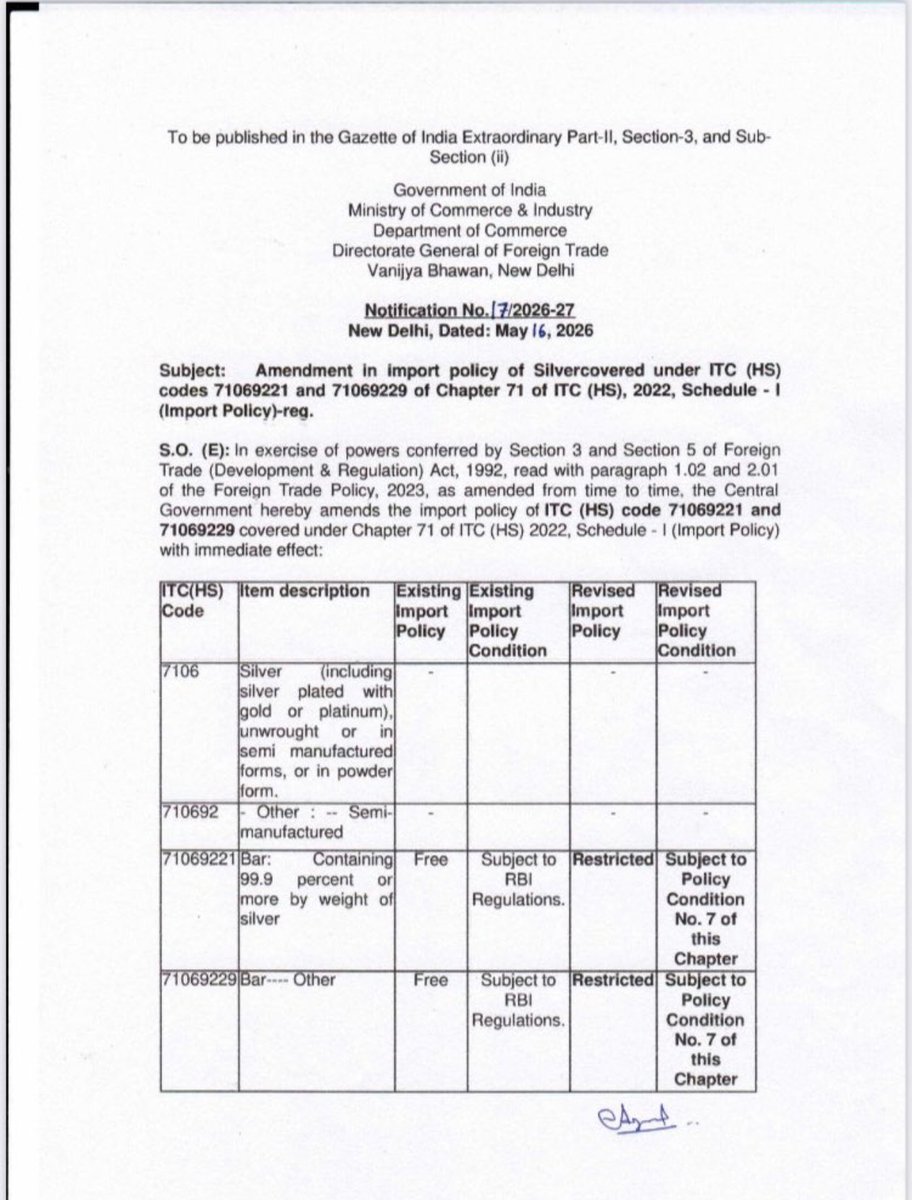

India has a silver problem.

It wants solar, EVs, electronics, AI infrastructure, defence and manufacturing growth.

But all of that needs silver.

So restricting silver imports is not simple.

India cannot fully choke silver supply without hurting its own industrial future.

The likely path is a two-tier market.

Approved industrial users may still get silver.

But bullion dealers, investors and retail physical buyers may face tighter availability.

That means the issue is no longer just price.

It becomes access.

Who gets silver first?

Solar?

Industry?

Jewellery?

Bullion dealers?

Retail buyers?

India may not be banning silver.

It may be rationing silver.

And when a strategic metal starts getting rationed, premiums can become more important than the paper price.