Sensors & Vision 👇

$VPG provides high-accuracy sensors for force, torque, and weight measurement in robotics.

$OUST develops high-performance digital lidar sensors essential for robot perception.

$ARBE creates 4D imaging radar for robust, all-weather robotic sensing.

$MVIS specializes in compact lidar solutions for autonomous robots and vehicles.

$AUR integrates advanced sensor suites for self-driving trucks and robotics applications.

$KDK develops AI-powered autonomous driving technology focused on long-haul trucking, industrial applications, and defense ground vehicles.

$PONY is a leading autonomous driving company building robotaxi, robotruck, and personally-owned vehicle solutions with its Virtual Driver platform, operating extensively in China and expanding globally.

$CGNX is a global leader in machine vision systems that enable robots to see and inspect.

$INVZ delivers high-resolution lidar sensors for robotics and autonomous systems.

$HSAI is a global leader in 3D lidar sensors, supplying high-performance perception hardware for autonomous vehicles, robotaxis, delivery robots, and industrial robotics applications.

Nobody is really talking about $KEEL and it has over 80% upside to the Street high target that just dropped.

Citizens just initiated it last week with an Outperform rating and a $10 target. The stock sits around $5.80.

KEEL is building AI and HPC data centers on secured power in some of the most power constrained, in demand markets in the country, with a 2.2 gigawatt pipeline and $533 million in liquidity to fund it. First revenue is expected in 2027 as the sites come online.

A funded AI infrastructure play in the right markets at the right time, sitting at half the Street high target. Worth a look.

$KEEL 🔥🔥🔥🔥🚀🚀🚀🚀🚀🚀🚀

$Keel Infrastructure CEO Ben Gagnon ( @CaptainKeel) shared several key updates that reinforce the company's long term AI infrastructure strategy.

• The recent $458M convertible note raise was described as a strategic move to accelerate expansion, not because the company needed cash to survive.

• $Keel now has one of the strongest balance sheets in the sector, with nearly $1B in liquidity, while reducing Bitcoin exposure to less than 15% of its treasury.

• The financing came with a 1.25% coupon and was 7x oversubscribed, highlighting strong institutional demand.

• Ben said he is even more confident than before about signing three major customer agreements by the end of 2026.

• Once a lease is signed, the company expects to announce it within 24 to 48 hours, rather than waiting for an earnings release.

• $Keel continues to prioritize securing the best long term lease economics instead of rushing to pre lease power at lower prices.

• Management believes enterprise AI customers may ultimately pay higher rates than hyperscalers because AI deployment creates significant business value.

• Pennsylvania remains a competitive advantage thanks to faster permitting, abundant skilled labor, and attractive 24/7 power availability.

Key Takeaway

$Keel's strategy remains unchanged. Build a strong balance sheet, secure premium AI data center assets, and wait for high value customers instead of chasing short term deals. Management appears increasingly confident that meaningful catalysts are approaching in the second half of 2026.

Rare earths gets a lot of attention, but the business actually making money at Energy Fuels $UUUU is uranium--the largest and lowest-cost in the US.

Its Pinyon Plain mine ran at ~1.62% eU3O8 in 2025, which management calls one of the highest grades in U.S. history, at an all-in cost of $23-30 per pound.

FY2025 results beat guidance on every line. $UUUU mined ~1.72M pounds of contained U3O8, produced ~1.015M finished pounds, and sold 650,000 pounds at a $74.21 average realized price for $48.2M of uranium revenue.

2026 guidance steps up to 2.0-2.5M pounds mined, 1.5-2.5M processed, and 1.5-2.0M sold.

In June the company said it expected ~1.6M finished pounds by mid-year, already inside the full-year range, then plans to pause its White Mesa mill to rebuild ore stockpiles and restart in Q4.

The selling balances cheap legacy contracts and opportunistic spot sales. In Q1 2026, $UUUU sold 100,000 pounds into the spot market at $95.88 and 410,000 pounds under older contracts at just under $64.

The ramp is showing up in the numbers. Q1 2026 revenue rose 112% y/y to $35.8M, almost all uranium, and operating cash flow turned positive at $8.3M, helped by collecting receivables.

With Pinyon Plain's low costs and finished inventory carried at $36 a pound, well under what uranium now sells for, the segment keeps moving toward profitability.

Only ~$23M of minimum contracted revenue is left for 2026, so the cheapest legacy pricing is nearly delivered. The rest of the year sells at spot, near $96 a pound in Q1, or under newer, higher-priced contracts, and realized prices step up from here.

Those low contracts justified restarting the mines. The six long-term contracts now run to 2032, each setting a minimum price and a maximum while still leaving room when spot climbs.

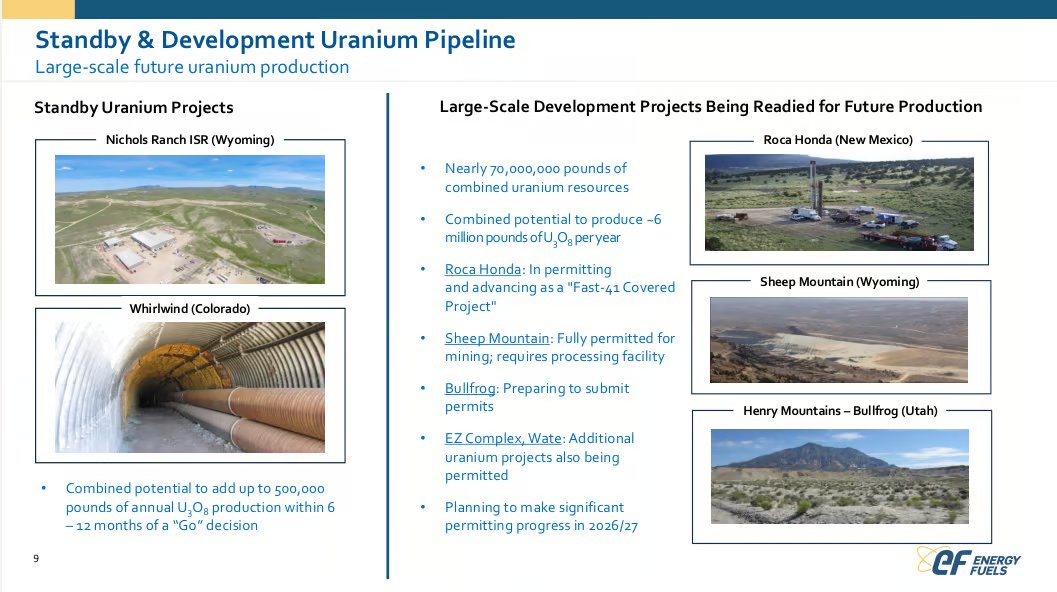

The U.S. still imports most of its uranium, and $UUUU is a low-cost domestic producer with a deep permitted pipeline (Roca Honda, Bullfrog, Sheep Mountain, Nichols Ranch). Even if the rare earth plan never lands, the uranium side stands on its own.

The demand side is strengthening too. The IAEA has raised its nuclear forecasts five years running, and the 2026 wave of reactor restarts, life extensions, and new SMRs (small modular reactors) adds tens of gigawatts of new capacity.

Each gigawatt burns 0.4-0.5M pounds of uranium a year, so four new reactors alone use about what $UUUU produces in a year.

Kazakhstan mines ~40% of the world's uranium with sulphuric-acid leaching, and sulphur costs have spiked in 2026, squeezing the largest low-cost supplier and supporting the price. $UUUU uses acid as well, but Pinyon Plain's high grades mean it burns far less per pound.

White Mesa is licensed for over 8M pounds of U3O8 a year, well above the ~1.5-2.5M $UUUU plans to produce, so it can run other miners' ore through the mill for a fee when prices make that worthwhile.

Breaking: China just banned exports to America's top rare earth miners

3 stocks worth watching:

$MP: MP Materials

*Operates the only major rare earth mine in the United States. The DoD owns a $400M equity stake

$USAR: USA Rare Earth

*Just opened its first rare earth processing facility in Colorado with $1.6B in government backing

$UUUU: Energy Fuels

*Received a $725M Pentagon loan last week to expand domestic rare earth processing

Currently, China controls 85% of the world's rare earth processing

My top 5 stocks right now:

$NBIS $RKLB $OUST $MU $ASTS

Why I’m bullish:

$NBIS — AI infrastructure upside.

$RKLB — real space execution.

$OUST — lidar adoption story.

$MU — AI memory powerhouse.

$ASTS — massive asymmetric upside.

This is basically my bet on AI compute, space, autonomy, and next-gen connectivity.

Volatile? Yes.

But that’s where the big winners usually hide

$BE was losing $200,000,000 every year before spiking 3200% from $10.

Right now, there's 4 stocks setting up exactly the same:

1. $TE target $110+

AI power buildout burning cash now, margins inflect once Austin G2 scales output

2. $KEEL target $70+

pivoting bitcoin power into AI compute leases, re-rating from miner to infrastructure play

3. $POET target $50+

near-zero revenue today, but $500M+ optical AI supply deal could flip that fast

4. $APLD target $400+

AI data center buildout burning cash now, contracted leases could flip it profitable

♻️ RESHARE this post and write 1 comment, I'll DM you right now my favorite 1000% call option to get for $TE.

$KEEL vs $IREN vs $CIFR

🧢Market Cap

KEEL - 4B

IREN - 21B

CIFR - 10B

💰Revenue TTM

KEEL - 229M

IREN - 750M

CIFR - 224M

📈Stock Price

KEEL - 6.76

IREN - 55.33

CIFR - 28.06

One major difference between the 3 is that $KEEL has not signed any tenants/contracts – yet

#BULLISH

Big News 🚨 by $UUUU

Energy Fuels Announces Definitive Agreement to Acquire VAC for $1.9 Billion Equity Value 👇

Acquisition creates unique, fully integrated mine-to-magnet rare earth platform

• Positions the Combined Company to Capitalize on Surging Demand for Rare Earth Magnets across North America and Europe

• >$2 Billion Annual Permanent Magnet Potential Customer Pipeline Revenue Across Auto, Defense, Robotics, and Data Center Sectors

• Expected to be Immediately Accretive to Energy Fuels' Cash Flow and Margin Profile

• Links VAC's Established Permanent Magnet Business with Energy Fuels' Growing Rare Earth Mining, Processing and Refining Platform

• Company is Pursuing Various Funding Opportunities, including Government Programs, to Complement its Growth Strategy, and Recently Announced a $725 Million Conditional Loan from U.S. Office of Strategic Capital 👇

$Te T1 Energy Receives "A" Grade in Bankability Assessment from Intertek CEA

This is very bullish for TE, here’s why

• Bankability is a big deal in solar. Intertek CEA (formerly Clean Energy Associates) is the gold standard third-party assessor for project financiers, developers, and banks. An “A” grade on their rigorous audit of manufacturing quality, processes, supply chain, and product reliability signals extremely low technical and performance risk. This makes T1’s modules far more attractive for large-scale project financing lenders which love de-risked assets

• The G1 Dallas 5GW facility now sits among the highest rated solar module plants globally. In an industry plagued by quality concerns (especially with overseas supply), this independent stamp of excellence differentiates T1 as a premium, bankable U.S manufacturer

• Higher bankability means easier project approvals, better financing terms (lower interest rates, higher leverage), faster sales cycles, and stronger pricing power. It also boosts eligibility for U.S incentives and domestic content preferences under IRA policies

• T1 is scaling American solar + storage manufacturing. This news reduces perceived execution risk, improves investor confidence, and positions them favorably against competitors especially as demand for secure, high quality domestic supply grows amid geopolitical and tariff uncertainties

This is a strong credibility signal that can accelerate revenue, margins, partnerships, and valuation rerating

News 🚨 by $TE 👇

T1 Energy Receives "A" Grade in Bankability Assessment from Intertek CEA

Independent evaluation places T1 Energy's G1_Dallas facility among the world's highest-rated solar module manufacturing operations.

https://t.co/XthhsCvbMX

Ouster $OUST was added by our algorithm to the US MidCaps Growth Rockets portfolio at the latest rebalance.

Builds the sensing layer physical AI runs on: digital LiDAR + cameras and perception software for robots, warehouses and autonomy. Shipped 25,000+ sensors in 2025, up 48%.

The last two weeks back that up: a new collaboration with FieldAI to put its Rev8 color lidar into general-purpose industrial robots, and a BlueCity rollout across 40+ sites around MetLife Stadium for the 2026 FIFA World Cup.

Loss-making for years, but management guides profitability in 2027.

$TE: AI needs power. Data centres need power. American industry needs power.

Solar and storage are the only energy resources scaling fast enough to meet this moment.

$TE isn’t just building solar panels. They’re building the energy infrastructure America needs to win the next decade.