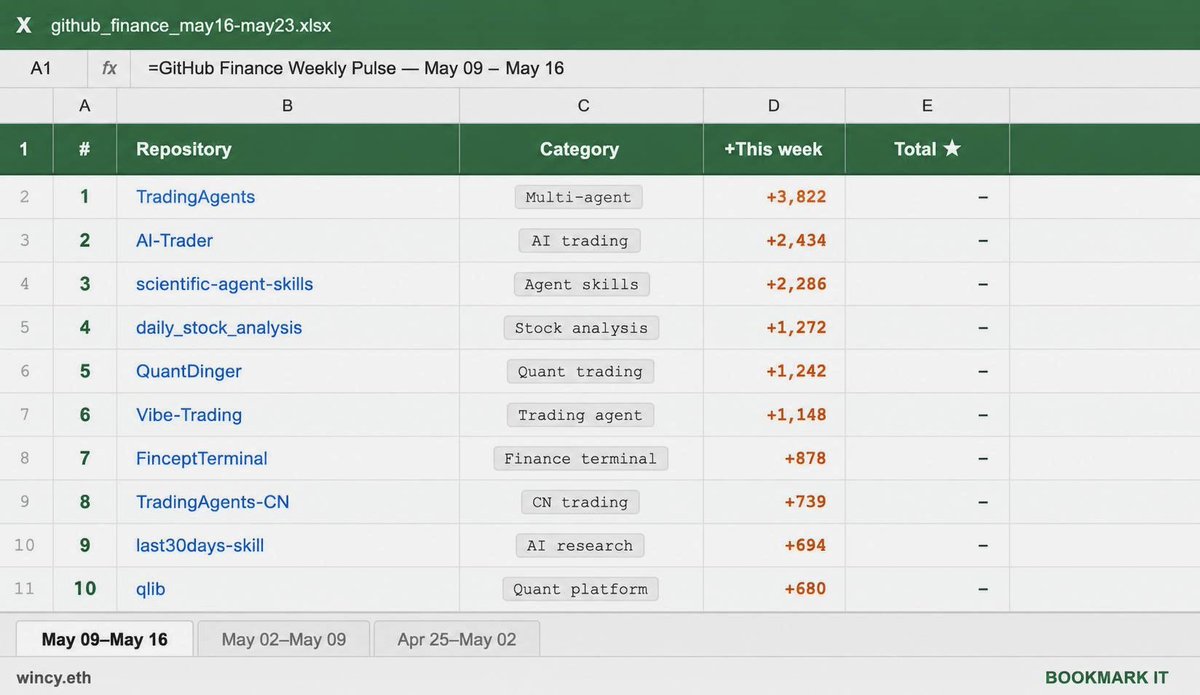

the fastest growing GitHub repos in finance this week:

1. TradingAgents (+3,822 ★)

multi-agent LLM trading framework built for financial research and execution. combines analyst agents, sentiment models, portfolio reasoning, and provider integrations into a single trading stack.

2. AI-Trader (+2,434 ★)

fully automated agent-native trading system. built around autonomous decision-making, price fetching, execution, and monitoring workflows. focused on end-to-end AI-driven trading infrastructure.

3. scientific-agent-skills (+2,286 ★)

plug-and-play agent skills for finance, research, science, engineering, and writing. integrates with multiple agent frameworks and supports web research, bioinformatics, cheminformatics, and analysis pipelines.

4. daily_stock_analysis (+1,272 ★)

LLM-powered stock analysis platform covering US, Hong Kong, and Chinese equities. combines market data, real-time news, AI dashboards, automated reporting, and multi-channel notifications with near-zero operating cost.

5. QuantDinger (+1,242 ★)

AI quantitative trading platform for crypto, stocks, and forex. includes live trading, strategy backtesting, market analytics, and broker integrations. built for traders experimenting with AI-assisted quant workflows.

6. Vibe-Trading (+1,148 ★)

personal AI trading agent focused on algorithmic trading and backtesting. combines lightweight automation with agent-style portfolio management and strategy experimentation.

7. FinceptTerminal (+878 ★)

modern open-source finance terminal inspired by Bloomberg-style workflows. provides market analytics, investment research, trading tools, and AI-powered financial infrastructure in one interface.

8. TradingAgents-CN (+739 ★)

Chinese-enhanced version of TradingAgents. adapts the multi-agent LLM trading framework for Chinese financial markets, datasets, and workflows. rapidly growing among Chinese quant and AI communities.

9. last30days-skill (+694 ★)

AI agent skill for researching trends across Reddit, X, YouTube, Hacker News, Polymarket, and the broader web. designed for signal discovery, narrative tracking, and internet-wide monitoring.

10. qlib (+680 ★)

Microsoft’s AI-oriented quant investment platform. covers the entire quant pipeline from data collection to alpha generation, portfolio construction, and execution. still one of the strongest open-source quant ecosystems available.

bookmark this and start today.

Finding on-chain alpha on @DecibelTrade, but are you still doing this?

❗️ Manually searching wallets

❗️ Guess work on Trader's Performances

❗️ Using random tracking bots

Time to Stop and Switch to Copin.

NEW: Major investigation dropping February 26 on one of crypto’s most profitable businesses where multiple employees abused internal data to insider trade over a prolonged period of time.

The recent $ETH rally has sent this whale’s deep into the green 📈

His $678M $ETH long (5x) is now up $38M — a 28% ROI, with liquidation safely down at $2,066.

The wins don't stop there—he is sitting on another $11M in profit from his other positions: $95M Long on $BTC & $74M Long on $SOL

[Attack of the MM (1): Market Maker Inventory-Based Quoting Systems]

Have you ever experienced the following situation?

You buy a small-cap altcoin, and shortly afterward the price consistently moves against you—as if a “market-making cartel” were deliberately targeting your position.

Is this really manipulation, or some conspiracy by the “whales”?

This article introduces the market maker quoting system and demystifies the so-called “whale conspiracy.”

Conclusion first: prices frequently moving against retail traders is not subjective manipulation. Instead, it is a natural outcome of inventory-based pricing under the Avellaneda–Stoikov framework, specifically quote skewing and toxic order flow protection mechanisms.

Let’s explain this step by step.

Once upon a time…

1. Inventory: the Core Concept

Market makers are not directional traders.

Under proper hedging, spot price movements should, in principle, have minimal impact on total PnL. In this setting, holding inventory is a passive consequence of providing liquidity rather than an intentional bet.

However, inventory matters:

Inventory accumulation expands exposure

The larger the position, the greater the risk to adverse price moves

Retail order flow directly alters the market maker’s inventory

When retail traders submit buy or sell orders, they disturb the market maker’s inventory balance.

The market maker must react to the risk introduced by inventory changes.

In short:

You break the equilibrium → the market maker must protect itself → the protection mechanism is the quoting system.

2. Quote Skewing

Suppose a market maker is aggressively hit by buy orders.

Economically, this means:

The market maker is selling

Inventory becomes short

Downside risk increases if prices rise further

At this point, the market maker’s objectives are:

1,Rebalance inventory as quickly as possible

2,Protect the exposed short position

The market maker will:

Shift quotes downward->Attract selling interest, Discourage further buying, Ensure that the current short exposure does not immediately incur losses, Buy time for hedging or rebalancing

This is quote skew, not manipulation.

3. Spread Widening

If inventory imbalance continues to deteriorate, quote skew alone is insufficient.

The market maker will also:

Widen the bid–ask spread

Reduce execution probability

Lower the rate of inventory accumulation per unit time

The goal is twofold:

Reduce short-term execution risk

Increase spread capture to compensate for inventory risk

4. Reservation Price and the Mathematics Behind Quotes

Each trade between retail traders and market makers occurs at the Reservation Price, which arises from inventory-based pricing models.

In simplified form:

Reservation Price=Mid Price−γ⋅q

Where:

q: current inventory

γ: risk aversion coefficient

(Yes, the full expression is uglier—but we’ll spare you.)

When retail traders trade aggressively, inventory ( q ) changes rapidly, causing the reservation price to shift accordingly.

Under the Avellaneda–Stoikov model:

Optimal quotes are symmetrically placed around the reservation price

Inventory is forced toward mean reversion to zero, Optimal spreads increase with risk

If this part is unclear, that’s fine.

The takeaway is simple:

When retail traders buy aggressively and prices move against them, it is because their own order flow has altered the market’s risk pricing.

5. Why Retail Traders Are Especially Vulnerable

Retail traders typically exhibit the following characteristics:

Almost always submit market orders

Trade in concentrated size

Poor timing concealment

No hedging

No order slicing or time-weighted execution

These issues are magnified in illiquid small-cap altcoins, where:

Liquidity is thin

Your order may be one of the few aggressive trades within minutes

There is little natural offsetting flow

In large-cap markets, opposing flows may naturally neutralize inventory.

In small-cap coins, you are effectively the market maker’s entire counterparty.

6. The Market Maker’s True Objective

Professional market makers are not trying to “liquidate” retail traders.

Their objective function is closer to:

maxE[Spread Capture]−Inventory Risk−Adverse Selection

Inventory risk is penalized exponentially, making protection mechanisms essential.

7. A Practical Trick: Exploiting the Quoting Mechanism

If you’ve read this far, you probably harbor dreams of becoming a “whale” yourself.

Retail traders suffer because they trade: Too fast&Too visibly In concentrated size

So let’s reverse that.

Example:

Suppose Dave wants to build a $1,000 long position.

Instead of going all-in, Buy $100->The market maker skews quotes downward->Buy another $100 at a lower price

Quotes skew further downward

Continue incrementally

Result:

Lower average entry price

Reduced adverse quote impact

You partially use the market maker’s inventory mechanism instead of fighting it

This is only half of the story.

Beyond inventory-based pricing, order book dynamics and toxic order flow detection are another major source of price divergence from retail expectations.

In the next installment, I will:

Explain how market makers process order flow

Analyze order book microstructure

Speculate (imaginatively) on the microstructural causes of the infamous “10/11 incident”

To be continued.

Hyperliquid is built on a foundation of onchain transparency. A recent article made several claims that are factually incorrect:

+ Solvency: Every dollar is accounted for; the author failed to count native HyperEVM USDC.

+ Integrity: Testnet functions are exactly that - testnet only for testing. They cannot be executed on mainnet.

+ Transparency: Hyperliquid is more transparent and decentralized than all other major venues for perps trading. The entire state is independently maintained by a permissionless validator set and verified through BFT proof-of-stake consensus by each node. Every order, trade, and liquidation is available in real time during execution. Anyone can run a node and index the chain’s state and transitions. No major perps platform comes close to this guarantee for users.

See our response to the writer’s individual points below.

Claim: The system is undercollateralized by $362M

False: The Hyperliquid blockchain state is fully and verifiably solvent. The author excluded the HyperEVM USDC (a publicly announced and much anticipated integration), which exists in parallel to the Arbitrum bridge. Every USDC in circulation on HyperCore is accounted for transparently, by summing up the balances of https://t.co/Fk2lhZvpXD and https://t.co/pGBPcsJUTl. At the time of writing, this amounts to 3.989B + 362M = 4.351B USDC on HyperCore. USDC on the HyperEVM can be computed by subtracting 362M from the 421M on the HyperEVM USDC contract (https://t.co/ohiJm3WzN8), totaling another 59M USDC on HyperEVM.

The sum of the Arbitrum bridge and native USDC balances can be compared against the sum of user balances on HyperCore. As highlighted in the introduction, this exercise of verifying complete system solvency against user balances is uniquely possible on Hyperliquid compared to competitors.

The current Arbitrum bridge was an important stepping stone in bootstrapping the Hyperliquid network and will be deprecated as the migration to native USDC is complete, bringing Hyperliquid to parity with other major L1s.

Claim: There is retroactive volume manipulation via TestnetSetYesterdayUserVlm

False: This is a testnet-only function to allow for comprehensive testing. The author states that “the function’s presence is the problem…capability alone violates the trust model.” Testnet-only features that enable more rigorous testing of edge cases do not undermine the chain’s integrity. The fee schedule on Hyperliquid interacts in a complex way with inputs: user volume, aligned quote token status, maker vs taker, HIP-3, etc. It’s important to test these interactions on testnet, and therefore the testnet chain has a set of admin testing functions that do not exist on mainnet. The related TestnetAddMainnetUser action is to mark a testnet user as having corresponding mainnet state, to avoid DDOS and other attacks that are “free” on testnet. None of these functions are callable on the mainnet state.

While the execution source is not available, anyone can verify every trade onchain by running a node, and sum up the values to confirm that volume numbers are reflected accurately in onchain state. Similar to onchain solvency verification against the sum of all user account values, this is possible on Hyperliquid but not on most competitive platforms.

Given that this code path is entirely unreachable on mainnet, future development work will entirely compile out this testnet-only logic on mainnet nodes to avoid any possible misunderstanding or misinterpretation.

Claim: Some users have special privileges such as fee exemptions or retroactive volume manipulation used to influence the airdrop

False: Like system solvency, user balances, and individual trades, the fees paid by any address is available onchain. Each trade along with its fees paid or rebates received are transparently indexed by nodes, API servers, and third party analytics providers. There are no such mechanisms to distort fees, and no such mechanisms could have influenced the HYPE airdrop. Furthermore, the genesis distribution of HYPE is fully available onchain, and users can verify the historical behavior of every such address.

Claim: “CoreWriter” godmode can mint tokens, move user funds without signatures, crash random validators and basically do whatever it wants

False: The CoreWriter spec is fully documented here https://t.co/TTMWI5pDBB and replicable in the open source HyperEVM execution. CoreWriter is a way for smart contracts on HyperEVM to send HyperCore actions as part of HyperEVM block execution. It supports various actions that are normally sent by EOAs such as staking and placing orders, but has no such features to “mint tokens, move user funds without signatures, crash random validators and basically do whatever it wants.” This is a fundamental misunderstanding of how HyperCore interacts with the HyperEVM.

Claim: Chain can freeze via governance, and no undo function exists

Misinterpreted: The chain freezes during network upgrades. There is no undo function because the validators adopt a new binary at that height. This is analogous to how other networks perform hard forks at future heights determined by social consensus.

Suspicious activity on POPCAT in Nov 2025 did not cause the L1 to freeze, nor were any user funds frozen. The L1 was entirely operational, and any observer can see the blocks that were produced during this time. The Arbitrum bridge was automatically locked after the incident due to abnormal variation in account balances. As explained above, the Arbitrum bridge is not as secure as natively minted USDC, and therefore requires several conservative automated locking mechanisms as safeguards. The Arbitrum bridge’s locking mechanism is audited and open sourced, and the bridge is being deprecated with the transition to native USDC.

Claim: A single private key can set any oracle price instantly: no timelock, no limits

Misinterpreted: The author is likely mistaking the HIP-3 oracle updater logic with the validator-operated perps. HIP-3 oracle updates are indeed set by a single address, but this is up to the deployer to configure. The updater address need not be an EOA. For example, current HIP-3 deployers use a combination of MPC and CoreWriter architecture.

For validator-operated perps, multiple validators can submit oracle price updates. The final prices are a robust weighted median across major centralized exchanges. There is no timelock and no limits explicitly because these limits make the system less, not more, safe. The events of 10/10 show the danger to solvency if ADL is not accurately triggered in a timely manner during high volatility. Hyperliquid was one of the only venues without performance degradation or a network outage during this time. If Mango Markets or a similar protocol with oracle rate limits were active during 10/10, they would have likely accrued bad debt. Further decentralization will involve other validators actively running independent and open-sourced oracle update binaries.

Claim: 8 undisclosed addresses control all transaction submission

False: Some transactions are already sent directly from the validators. Some such as orders are not, in order to minimize MEV, but a future upgrade will incorporate this logic for all transactions in a mechanism that is both MEV- and censorship-resistant. The careful consideration of MEV is in response to trader and researcher feedback based on predatory behavior observed on other chains. There is almost unanimous agreement that toxic transaction ordering degrades the end user experience. Ultimately, the validator set is permissionless, and there is no guarantee that validators in the mainnet set are always fully aligned with the ecosystem. A major milestone in decentralization will be solving this problem, including a multiple-proposer block building setup.

Claim: There is a liquidation cartel with unfair advantages

Misinterpreted: Only HLP may backstop liquidate users, and HLP subvaults are the only addresses in this set. However, depositing into HLP is permissionless, so HLP is a community-owned liquidity vault supporting the protocol. The fact that HLP has privileges is no different from other protocol liquidity vaults.

Relatedly, all liquidations are first attempted against the order book, which handles the vast majority of liquidated positions without backstop liquidation. This allows users to keep any remaining collateral, and allows all other users to compete in providing the best price to the liquidation flow, benefitting the liquidated user.

Claim: There is a hidden lending protocol with $1M+ supplied and no documentation

False: Portfolio margin, borrow lend, and the HLP supplied value were all publicly announced and are currently in pre-alpha rollout. The current documentation can be found at https://t.co/vvE8EhpIhX and has been progressively fleshed out over the past several weeks.

Claim: ModifyNonCirculatingSupply allows changes to token supply

False: The full supply of HIP-1 tokens on HyperCore is fixed at deployment. The non-circulating supply is a purely informational number that can optionally mark addresses as “non-circulating” for display purposes. Whether an address is marked as “non-circulating” does not affect execution. This is an example of onchain information that might make more sense offchain, but is not a vulnerability.

Thank you to the author for spending the time to verify the execution of Hyperliquid. The fact that this investigation could be done at all proves the transparency and decentralization that Hyperliquid has already achieved. Concretely, Hyperliquid is the only major perps venue where the entire state and every input diff is transparently available to anyone running a node.

A similar analysis on any of the other top perp DEXs is impossible. For example, Lighter uses a single centralized sequencer whose execution logic and ZK circuits are unavailable. Aster uses centralized matching and even offers dark pool trading, which is only possible with a single centralized sequencer without verifiable execution. Other protocols with some open source contracts do not have a verifiable sequencer.

On Binance, Lighter, Aster, or similar exchanges, it is impossible for anyone other than the sequencer to see a full snapshot of onchain state including order books, positions, and other user information. The centralized sequencer can also upgrade its software without any constraints. On Hyperliquid, the entire state is onchain, which means there are 24 validators executing the same state machine under BFT consensus rules. There is plenty left to do on the journey towards greater decentralization, but it’s important to highlight just how far Hyperliquid and its ecosystem have come compared to competitors.

Decentralization is progressive, and Hyperliquid will ultimately be fully open sourced. Hyperliquid is the most transparent of all major venues, even though this leaks advantages to competitors (all of whom are closed source), who can copy Hyperliquid’s innovations more easily. We think this is the correct tradeoff to balance value accrual to the community, speed of innovation, and upholding the values of defi.

The HyperEVM execution is open source, and Sprites, an independent community member, maintains a full archival node that powers many important integrations. HyperCore will follow the same path as soon as it reaches feature completion.

Despite an improving Fear & Greed Index, Perpetual DEX activity is fading.

Both trading volume and number of open positions are declining across all wallet tiers — from sharks to whales to super whales.

Right now, Super Whales (avg trade size $10–100M) are still leading the market, holding $245M in total OI across 13 positions.

Overall, liquidity and leverage are clearly receding — likely a mix of risk-off behavior and the approaching holiday lull.

From a peak of +$19M profit to –$13.4M loss 😬

This whale isn’t backing down. Instead, he’s adding risk. His massive long positions now include:

• $565M on $ETH

• $90M on $BTC

• $33M on $SOL

With the recent market drop, all positions are currently sitting in the red.

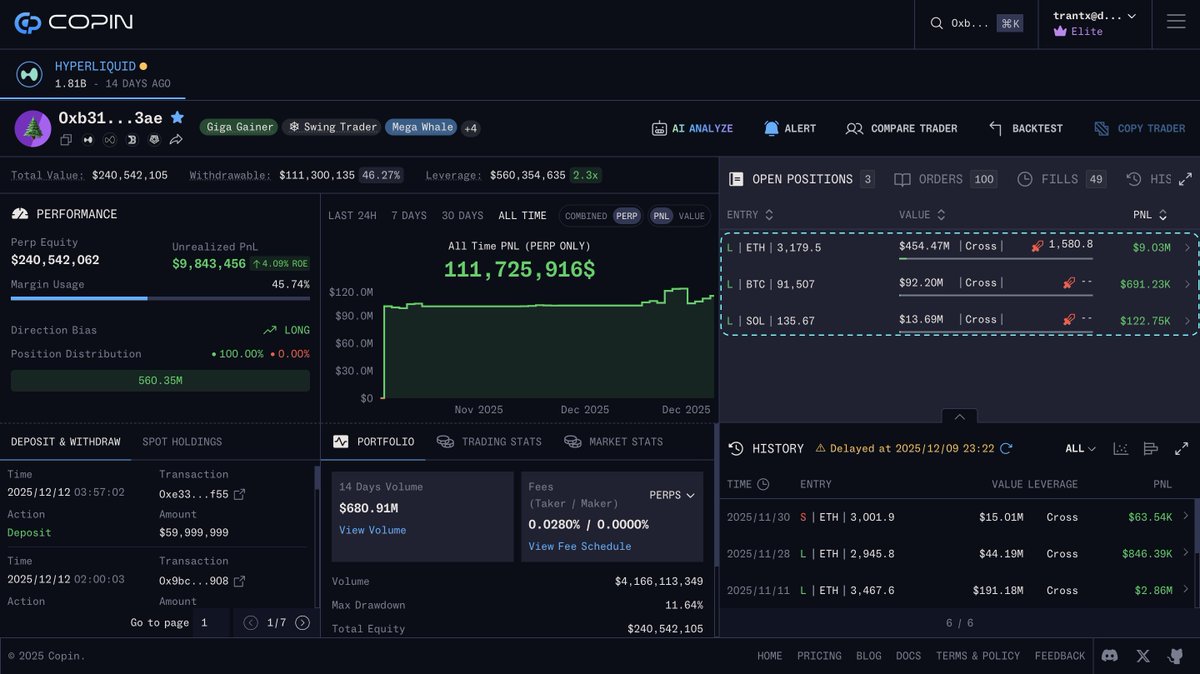

Since our last post, this whale has grown his $ETH position to $454.5M and opened new $BTC and $SOL longs with a combined size of another $115M.

All positions are in the green right now.

He has also deposited another $110M into his account.

Anticipate some BIG moves from this whale.

As $HYPE drops for the 6th straight day down to the $27 range, Fasanara Capital’s massive short just keeps printing 💵

Their $45M $HYPE short (5x) has now generated over $11M in profit, pushing the account’s lifetime PnL to $112.7M.

A wallet to watch during the bear season

Those who can, do

Those who can't, fud

Before writing a paper maybe learn the definition of what you are studying? ADL does not "transfer pnl to HLP." It treats HLP entirely symmetrically with users. **ADL has nothing to do with HLP or backstop liquidations**

ADL did not "destroy $653 million of pnl" either. If you don't understand what you're talking about, you are not qualified to spread lies masked by fancy ML terms to sound smart. It's a shame that these are the "academics" that the industry looks up to.

![bc1qDave's tweet photo. [Attack of the MM (1): Market Maker Inventory-Based Quoting Systems]

Have you ever experienced the following situation?

You buy a small-cap altcoin, and shortly afterward the price consistently moves against you—as if a “market-making cartel” were deliberately targeting your position.

Is this really manipulation, or some conspiracy by the “whales”?

This article introduces the market maker quoting system and demystifies the so-called “whale conspiracy.”

Conclusion first: prices frequently moving against retail traders is not subjective manipulation. Instead, it is a natural outcome of inventory-based pricing under the Avellaneda–Stoikov framework, specifically quote skewing and toxic order flow protection mechanisms.

Let’s explain this step by step.

Once upon a time…

1. Inventory: the Core Concept

Market makers are not directional traders.

Under proper hedging, spot price movements should, in principle, have minimal impact on total PnL. In this setting, holding inventory is a passive consequence of providing liquidity rather than an intentional bet.

However, inventory matters:

Inventory accumulation expands exposure

The larger the position, the greater the risk to adverse price moves

Retail order flow directly alters the market maker’s inventory

When retail traders submit buy or sell orders, they disturb the market maker’s inventory balance.

The market maker must react to the risk introduced by inventory changes.

In short:

You break the equilibrium → the market maker must protect itself → the protection mechanism is the quoting system.

2. Quote Skewing

Suppose a market maker is aggressively hit by buy orders.

Economically, this means:

The market maker is selling

Inventory becomes short

Downside risk increases if prices rise further

At this point, the market maker’s objectives are:

1,Rebalance inventory as quickly as possible

2,Protect the exposed short position

The market maker will:

Shift quotes downward->Attract selling interest, Discourage further buying, Ensure that the current short exposure does not immediately incur losses, Buy time for hedging or rebalancing

This is quote skew, not manipulation.

3. Spread Widening

If inventory imbalance continues to deteriorate, quote skew alone is insufficient.

The market maker will also:

Widen the bid–ask spread

Reduce execution probability

Lower the rate of inventory accumulation per unit time

The goal is twofold:

Reduce short-term execution risk

Increase spread capture to compensate for inventory risk

4. Reservation Price and the Mathematics Behind Quotes

Each trade between retail traders and market makers occurs at the Reservation Price, which arises from inventory-based pricing models.

In simplified form:

Reservation Price=Mid Price−γ⋅q

Where:

q: current inventory

γ: risk aversion coefficient

(Yes, the full expression is uglier—but we’ll spare you.)

When retail traders trade aggressively, inventory ( q ) changes rapidly, causing the reservation price to shift accordingly.

Under the Avellaneda–Stoikov model:

Optimal quotes are symmetrically placed around the reservation price

Inventory is forced toward mean reversion to zero, Optimal spreads increase with risk

If this part is unclear, that’s fine.

The takeaway is simple:

When retail traders buy aggressively and prices move against them, it is because their own order flow has altered the market’s risk pricing.

5. Why Retail Traders Are Especially Vulnerable

Retail traders typically exhibit the following characteristics:

Almost always submit market orders

Trade in concentrated size

Poor timing concealment

No hedging

No order slicing or time-weighted execution

These issues are magnified in illiquid small-cap altcoins, where:

Liquidity is thin

Your order may be one of the few aggressive trades within minutes

There is little natural offsetting flow

In large-cap markets, opposing flows may naturally neutralize inventory.

In small-cap coins, you are effectively the market maker’s entire counterparty.

6. The Market Maker’s True Objective

Professional market makers are not trying to “liquidate” retail traders.

Their objective function is closer to:

maxE[Spread Capture]−Inventory Risk−Adverse Selection

Inventory risk is penalized exponentially, making protection mechanisms essential.

7. A Practical Trick: Exploiting the Quoting Mechanism

If you’ve read this far, you probably harbor dreams of becoming a “whale” yourself.

Retail traders suffer because they trade: Too fast&Too visibly In concentrated size

So let’s reverse that.

Example:

Suppose Dave wants to build a $1,000 long position.

Instead of going all-in, Buy $100->The market maker skews quotes downward->Buy another $100 at a lower price

Quotes skew further downward

Continue incrementally

Result:

Lower average entry price

Reduced adverse quote impact

You partially use the market maker’s inventory mechanism instead of fighting it

This is only half of the story.

Beyond inventory-based pricing, order book dynamics and toxic order flow detection are another major source of price divergence from retail expectations.

In the next installment, I will:

Explain how market makers process order flow

Analyze order book microstructure

Speculate (imaginatively) on the microstructural causes of the infamous “10/11 incident”

To be continued.](https://pbs.twimg.com/media/G8-jevhbgAAduLp.jpg)

![bc1qDave's tweet photo. [Attack of the MM (1): Market Maker Inventory-Based Quoting Systems]

Have you ever experienced the following situation?

You buy a small-cap altcoin, and shortly afterward the price consistently moves against you—as if a “market-making cartel” were deliberately targeting your position.

Is this really manipulation, or some conspiracy by the “whales”?

This article introduces the market maker quoting system and demystifies the so-called “whale conspiracy.”

Conclusion first: prices frequently moving against retail traders is not subjective manipulation. Instead, it is a natural outcome of inventory-based pricing under the Avellaneda–Stoikov framework, specifically quote skewing and toxic order flow protection mechanisms.

Let’s explain this step by step.

Once upon a time…

1. Inventory: the Core Concept

Market makers are not directional traders.

Under proper hedging, spot price movements should, in principle, have minimal impact on total PnL. In this setting, holding inventory is a passive consequence of providing liquidity rather than an intentional bet.

However, inventory matters:

Inventory accumulation expands exposure

The larger the position, the greater the risk to adverse price moves

Retail order flow directly alters the market maker’s inventory

When retail traders submit buy or sell orders, they disturb the market maker’s inventory balance.

The market maker must react to the risk introduced by inventory changes.

In short:

You break the equilibrium → the market maker must protect itself → the protection mechanism is the quoting system.

2. Quote Skewing

Suppose a market maker is aggressively hit by buy orders.

Economically, this means:

The market maker is selling

Inventory becomes short

Downside risk increases if prices rise further

At this point, the market maker’s objectives are:

1,Rebalance inventory as quickly as possible

2,Protect the exposed short position

The market maker will:

Shift quotes downward->Attract selling interest, Discourage further buying, Ensure that the current short exposure does not immediately incur losses, Buy time for hedging or rebalancing

This is quote skew, not manipulation.

3. Spread Widening

If inventory imbalance continues to deteriorate, quote skew alone is insufficient.

The market maker will also:

Widen the bid–ask spread

Reduce execution probability

Lower the rate of inventory accumulation per unit time

The goal is twofold:

Reduce short-term execution risk

Increase spread capture to compensate for inventory risk

4. Reservation Price and the Mathematics Behind Quotes

Each trade between retail traders and market makers occurs at the Reservation Price, which arises from inventory-based pricing models.

In simplified form:

Reservation Price=Mid Price−γ⋅q

Where:

q: current inventory

γ: risk aversion coefficient

(Yes, the full expression is uglier—but we’ll spare you.)

When retail traders trade aggressively, inventory ( q ) changes rapidly, causing the reservation price to shift accordingly.

Under the Avellaneda–Stoikov model:

Optimal quotes are symmetrically placed around the reservation price

Inventory is forced toward mean reversion to zero, Optimal spreads increase with risk

If this part is unclear, that’s fine.

The takeaway is simple:

When retail traders buy aggressively and prices move against them, it is because their own order flow has altered the market’s risk pricing.

5. Why Retail Traders Are Especially Vulnerable

Retail traders typically exhibit the following characteristics:

Almost always submit market orders

Trade in concentrated size

Poor timing concealment

No hedging

No order slicing or time-weighted execution

These issues are magnified in illiquid small-cap altcoins, where:

Liquidity is thin

Your order may be one of the few aggressive trades within minutes

There is little natural offsetting flow

In large-cap markets, opposing flows may naturally neutralize inventory.

In small-cap coins, you are effectively the market maker’s entire counterparty.

6. The Market Maker’s True Objective

Professional market makers are not trying to “liquidate” retail traders.

Their objective function is closer to:

maxE[Spread Capture]−Inventory Risk−Adverse Selection

Inventory risk is penalized exponentially, making protection mechanisms essential.

7. A Practical Trick: Exploiting the Quoting Mechanism

If you’ve read this far, you probably harbor dreams of becoming a “whale” yourself.

Retail traders suffer because they trade: Too fast&Too visibly In concentrated size

So let’s reverse that.

Example:

Suppose Dave wants to build a $1,000 long position.

Instead of going all-in, Buy $100->The market maker skews quotes downward->Buy another $100 at a lower price

Quotes skew further downward

Continue incrementally

Result:

Lower average entry price

Reduced adverse quote impact

You partially use the market maker’s inventory mechanism instead of fighting it

This is only half of the story.

Beyond inventory-based pricing, order book dynamics and toxic order flow detection are another major source of price divergence from retail expectations.

In the next installment, I will:

Explain how market makers process order flow

Analyze order book microstructure

Speculate (imaginatively) on the microstructural causes of the infamous “10/11 incident”

To be continued.](https://pbs.twimg.com/media/G8-jevgbMAEeRpW.jpg)

![bc1qDave's tweet photo. [Attack of the MM (1): Market Maker Inventory-Based Quoting Systems]

Have you ever experienced the following situation?

You buy a small-cap altcoin, and shortly afterward the price consistently moves against you—as if a “market-making cartel” were deliberately targeting your position.

Is this really manipulation, or some conspiracy by the “whales”?

This article introduces the market maker quoting system and demystifies the so-called “whale conspiracy.”

Conclusion first: prices frequently moving against retail traders is not subjective manipulation. Instead, it is a natural outcome of inventory-based pricing under the Avellaneda–Stoikov framework, specifically quote skewing and toxic order flow protection mechanisms.

Let’s explain this step by step.

Once upon a time…

1. Inventory: the Core Concept

Market makers are not directional traders.

Under proper hedging, spot price movements should, in principle, have minimal impact on total PnL. In this setting, holding inventory is a passive consequence of providing liquidity rather than an intentional bet.

However, inventory matters:

Inventory accumulation expands exposure

The larger the position, the greater the risk to adverse price moves

Retail order flow directly alters the market maker’s inventory

When retail traders submit buy or sell orders, they disturb the market maker’s inventory balance.

The market maker must react to the risk introduced by inventory changes.

In short:

You break the equilibrium → the market maker must protect itself → the protection mechanism is the quoting system.

2. Quote Skewing

Suppose a market maker is aggressively hit by buy orders.

Economically, this means:

The market maker is selling

Inventory becomes short

Downside risk increases if prices rise further

At this point, the market maker’s objectives are:

1,Rebalance inventory as quickly as possible

2,Protect the exposed short position

The market maker will:

Shift quotes downward->Attract selling interest, Discourage further buying, Ensure that the current short exposure does not immediately incur losses, Buy time for hedging or rebalancing

This is quote skew, not manipulation.

3. Spread Widening

If inventory imbalance continues to deteriorate, quote skew alone is insufficient.

The market maker will also:

Widen the bid–ask spread

Reduce execution probability

Lower the rate of inventory accumulation per unit time

The goal is twofold:

Reduce short-term execution risk

Increase spread capture to compensate for inventory risk

4. Reservation Price and the Mathematics Behind Quotes

Each trade between retail traders and market makers occurs at the Reservation Price, which arises from inventory-based pricing models.

In simplified form:

Reservation Price=Mid Price−γ⋅q

Where:

q: current inventory

γ: risk aversion coefficient

(Yes, the full expression is uglier—but we’ll spare you.)

When retail traders trade aggressively, inventory ( q ) changes rapidly, causing the reservation price to shift accordingly.

Under the Avellaneda–Stoikov model:

Optimal quotes are symmetrically placed around the reservation price

Inventory is forced toward mean reversion to zero, Optimal spreads increase with risk

If this part is unclear, that’s fine.

The takeaway is simple:

When retail traders buy aggressively and prices move against them, it is because their own order flow has altered the market’s risk pricing.

5. Why Retail Traders Are Especially Vulnerable

Retail traders typically exhibit the following characteristics:

Almost always submit market orders

Trade in concentrated size

Poor timing concealment

No hedging

No order slicing or time-weighted execution

These issues are magnified in illiquid small-cap altcoins, where:

Liquidity is thin

Your order may be one of the few aggressive trades within minutes

There is little natural offsetting flow

In large-cap markets, opposing flows may naturally neutralize inventory.

In small-cap coins, you are effectively the market maker’s entire counterparty.

6. The Market Maker’s True Objective

Professional market makers are not trying to “liquidate” retail traders.

Their objective function is closer to:

maxE[Spread Capture]−Inventory Risk−Adverse Selection

Inventory risk is penalized exponentially, making protection mechanisms essential.

7. A Practical Trick: Exploiting the Quoting Mechanism

If you’ve read this far, you probably harbor dreams of becoming a “whale” yourself.

Retail traders suffer because they trade: Too fast&Too visibly In concentrated size

So let’s reverse that.

Example:

Suppose Dave wants to build a $1,000 long position.

Instead of going all-in, Buy $100->The market maker skews quotes downward->Buy another $100 at a lower price

Quotes skew further downward

Continue incrementally

Result:

Lower average entry price

Reduced adverse quote impact

You partially use the market maker’s inventory mechanism instead of fighting it

This is only half of the story.

Beyond inventory-based pricing, order book dynamics and toxic order flow detection are another major source of price divergence from retail expectations.

In the next installment, I will:

Explain how market makers process order flow

Analyze order book microstructure

Speculate (imaginatively) on the microstructural causes of the infamous “10/11 incident”

To be continued.](https://pbs.twimg.com/media/G8-jey0b0AE0mXL.jpg)