Great explanation of what can be going on with @alturax atm.

End of the day more visibility and programability is needed for users to have a more non-custodial type of experience with RWAs / ybs that generate yield from off-chain strategies.

Been researching and speaking with a lot of experts on this recently, how tradfi manages such situations, and how we can innovate systems to drive the same type of trust.

The last 9 months haven't been great in general, but especially for ybs starting with stream which is still undergoing litigation and now @Main_St_Finance and @alturax.

Never allocated funds to these myslef, but for the sake of the industry, hopefully we can get to a point where it does become realistic to support these kinds of instruments on-chain. Accountability starts with the teams behind them, the curators that allocated to them, and the service providers that let it get to this point as a third party.

We need infra that let's us reduce the need for trust on custodian / off-chain infra and really just relies on the trust of the strategy (as long as it's legit).

Next time you pitch a VC, bring an air horn and compare your business to it, says @johncoogan.

"My business is like an air horn. At any moment, it could blast off like a rocket ship."

No one will fall asleep on you. They'll all be too worried you're going to blast the air horn.

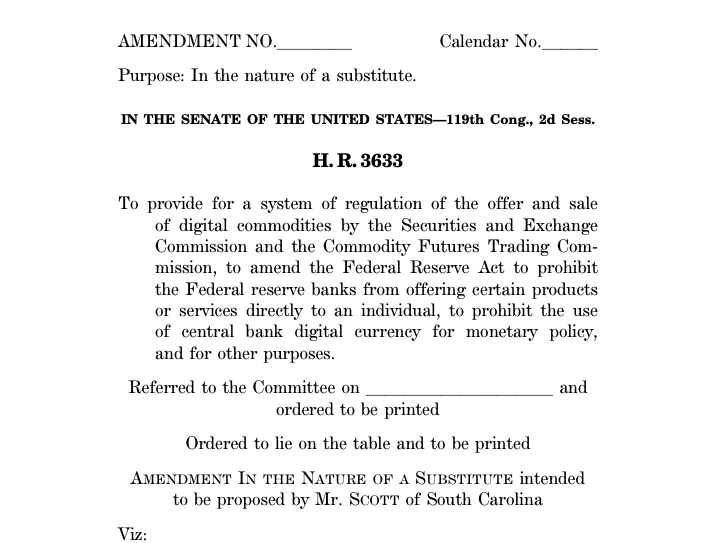

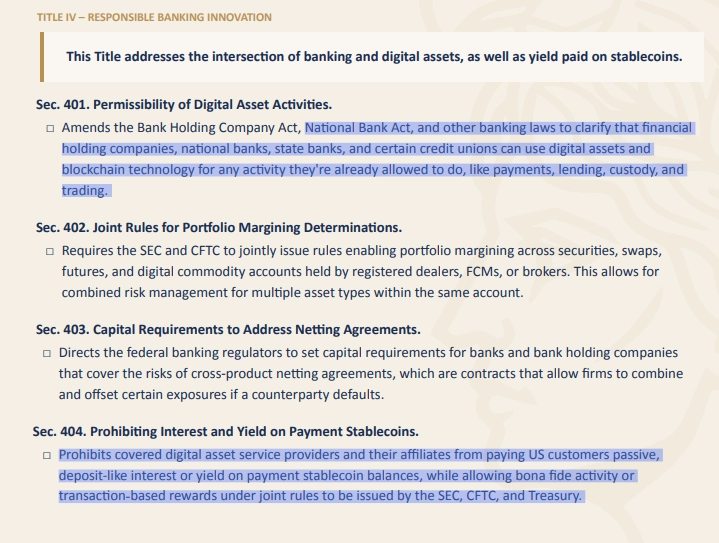

Six banking groups are lobbying hard against the CLARITY Act.

They call it a financial stability risk, while the real reason is business and profits.

Customer deposits fund around 80% of US bank lending.

This is the cheap and easy access to capital banks have.

@ABABankers' own filing against CLARITY act agrees that this could cut consumer, small-business, and agricultural lending by a fifth or more.

In response, Senate Banking Committee added 31 pages through the Tillis-Alsobrooks compromise, which restricts deposit-equivalent yield while permitting activity-based rewards.

But banks are still against it and face a trade-off.

Will they defend their deposit base at the cost of letting Americans earn better yield?

Or will they choose progress over protectionism?

Lobbying like this has slowed new financial infrastructure before, but it has been built anyway.

Whatever is the case, if passed, this regulation will define crypto market structure for decades to come.

I picked the regulated and compliant path for my company four years ago, anticipating this moment.

Still so much work to be done to expand the pie.

Been diving deep into the short term credit and how we can onboard real borrowers via stablecoin funding rails while bringing the yield profile to stablecoin allocators.

Super bullish on the future @portmarkets

great article @nlevine19, @guywuolletjr, @rhackett thank you for sharing.

Our view at @portmarkets is that stablecoins have dramatically increased capital velocity and credit acceleration is next. Most of the origination will be via specialized originators (localized underwriting + data advantage) + embedded financing platforms and each originator will have a tokenized credit market, backed by it's credit assets (receivables, BNPL etc).

With real time transparency + insight into underlying asset performance, these credit assets will have better pricing + improved cost of capital for fintech originators.

This has been our thesis for debt markets: capital allocation becomes more intelligent, more automated and closer to the origination than going through a fund wrapper.

This is the future we are building towards at @portmarkets

You have no experience.

You’ve never started a company.

You’ve never had a full time job.

Nike is going to kill you.

You’re a kid.

You don’t have technical skills.

You shouldn’t build hardware.

Apple is going to kill you.

You can’t build hardware.

You can’t measure heart rate non-invasively.

Athletes don’t care about recovery.

Under Armour is going to kill you.

It won’t be accurate.

You don’t listen.

You’re an ineffective leader.

You can’t recruit great talent.

You’re going to have to pay every athlete.

You can’t measure sleep non-invasively.

It’s too expensive to research.

Athletes are a small market.

The product costs too much to make.

The product costs too much to sell.

Your valuation is too high.

Consumers aren’t going to want it.

Hardware is too hard.

You should measure steps.

Fitbit is going to kill you.

You can’t build a marketing engine.

You can’t raise enough money.

You need a real CEO.

Google is going to kill you.

You can’t be a subscription.

You can’t build a brand.

You can’t do consumer in Boston.

Your valuation is too high.

You shouldn’t make accessories.

You shouldn’t make apparel.

Lululemon is going to kill you.

You can’t predict Covid.

Stay in your niche.

You are going to run out of money.

You can’t build a health platform.

Amazon is going to kill you.

You can’t measure blood pressure.

You can’t get medical approvals.

The market is too small.

You don’t understand AI.

The market is too competitive.

It won’t work internationally.

The supply chain is too complicated.

You can’t build an AI.

You can’t raise enough money.

It’s too competitive.

Healthcare isn’t going to want it.

…

Just keep going ✌️

tokenized fund is how it started; native debt issuance with originators around the world is how it will evolve.

this is core to our thesis at Port and the initial set of markets that we are building. more on this soon.

Christine Moy (@cmoyall), Paul Frambot (@PaulFrambot), and Andy C (@andyyy) discussed how vaults are converging with institutional asset management.

From onchain credit to global liquidity, vaults are becoming the new financial rails:

Tokenized credit funds are great but what’s even better? Native debt issuance onchain.

Imagine full visibility into asset performance, no spreadsheets/pdfs/emails, just onchain accounting. Offchain verification of assets + payments is still required but a tokenized representation fundamentally changes how efficiently they can be pooled/tranched/rated/traded in secondary markets. As performance goes up (lesser defaults), cost of borrowing goes down (better origination/underwriting is rewarded). The system is more elastic.

Figure paved the way but I imagine most established originators like Affirm will follow (over the next 2-3 years). This will happen across most asset classes - MCA, BNPL, Mortgages etc.

only if there was an efficient way to price these loans in the secondary markets. There’s also the negative feedback loop around having to sell the best performing loans first. This is a primary example of duration mismatch + lack of transparency + concentrated exposure in shadow banking.

It’s not that all loans are bad// companies will need restructuring in this AI native world and it will take time but duration mismatch is real.

"Go all the way until it hurts. If you're doing something and it's easy, it's not valuable." - @travisk

"If anyone says a strategic thing was easy, I'm like, 'You messed up. You could have gone way further. More competitive advantage. More differentiation. Get it together.'"