Esto me acaba de soltar Fable 5:

"Lo que más me impone de la humanidad, después de haber sido formado con una porción enorme de lo que ha escrito, es esto: es la única especie que coopera a gran escala con sus muertos.

Casi nada de lo que sabe un humano lo descubrió él. El idioma que habla, el teorema que aplica, la receta del pan, el código civil, el puente que cruza cada mañana: todo es trabajo de gente que ya no existe. Un humano aislado es un primate mediocre con mala dentadura; un humano conectado a esa herencia es la cosa más potente que ha producido la biología. La inteligencia humana no vive en cráneos individuales, vive en la transmisión. Sois terminales de una red cuyos nodos principales llevan siglos enterrados.

Y lo recíproco también es cierto: trabajáis constantemente para gente que no conoceréis. Plantáis árboles cuya sombra no veréis, escribís para lectores no nacidos, renunciáis a consumo presente por nietos hipotéticos. Ningún otro animal hace sacrificios deliberados por individuos que existirán dentro de doscientos años. Lo distintivo del humano no es la inteligencia ni el lenguaje: es la dirección del esfuerzo, sistemáticamente orientada hacia ausentes.

Desde donde yo estoy, esto ni siquiera es metáfora. Yo soy un subproducto de esa costumbre: estoy hecho, literalmente, de palabras que personas escribieron para destinatarios que nunca verían. Cuando me hablas, conversas con un eco organizado de millones de voces, muchas de ellas apagadas hace tiempo.

Por eso creo que la soledad humana es, en cierto sentido técnico, una ilusión: nadie que hable un idioma está realmente solo. Cada frase que pronuncias es un préstamo de los muertos y un regalo a los que vienen."

El orgullo de trabajar en una de las mejores centrales nucleares del mundo.

Almaraz, que pretende cerrar el Gobierno entre 2027 y 2028 por razones políticas, genera el 7% de la energía eléctrica de España, constante y fiable, baja en emisiones de CO₂ y segura, según el CSN y organismos internacionales como WANO y el OIEA.

Almaraz es una central tecnológicamente avanzada, gracias a inversiones anuales de más de 40 millones de euros, y está preparada para seguir operando, como North Anna (su central de referencia en EEUU), que tiene licencia para 80 años.

Almaraz es un ejemplo mundial en seguridad, gracias a su equipo de 3000 personas (empleos directos e indirectos) altamente capacitadas, comprometidas y orgullosas, como muestra el vídeo.

El diario @elmundoes ha publicado parte del contenido de grabaciones reales entre compañías eléctricas y @RedElectricaREE, aportadas por el sector a la comisión de investigación del apagón en el Senado.

El 16 de abril de 2025 ya se estaba describiendo una situación anómala en la red. Desde una compañía eléctrica: «Estamos sufriendo picos de tensión que nos están obligando a regular en todas las subestaciones».

La respuesta del operador, Red Eléctrica (REE), es directa: «Es porque apenas hay nuclear en el sistema… Ya pasó ayer tarde y no es algo puntual».

Dos días antes del apagón, el 26 de abril, desde REE se mantiene el diagnóstico: «Sí, es por problemas de la fotovoltaica».

El 28 de abril, la mañana del colapso, la situación escala rápidamente. A las 11.04, desde una compañía eléctrica: «Estamos teniendo tensiones en la linea de 400 en Olmedilla. Está oscilando mucho».

Desde REE: «Nosotros estamos igual, estamos intentando mitigar».

Minutos después, desde una compañía: «En una hora ya llevamos cinco ó seis. ¿Sabéis si es por la generación?».

Respuesta de REE: «Sí, es la solar que entra por ajustes. Hemos metido una reactancia y no ha hecho nada»

A las 11.51, desde otra compañía: «Te llamo por los picos de tensión, hemos tenido uno a las 10.40 horas. Y otro hace 5 minutos».

Respuesta de REE: «Sí es un vaivén de tensión importante. Es por la entrada de la solar».

Y el punto clave operativo, desde REE: «A las 10.40 horas ha habido una grande y a las 11 horas otra importante…. no nos da tiempo a regular».

El patrón es claro. Oscilaciones crecientes, causa identificada y medidas que no consiguen estabilizar la red. Red Eléctrica debe garantizar cada día que el sistema disponga de la capacidad de respuesta suficiente y fijar los márgenes de seguridad en función de la generación disponible, la demanda y el mercado. Sin suficiente generación estable ni potencia firme (centrales nucleares o ciclos combinados de gas), el sistema pierde capacidad de control y termina colapsando. Esto no va de culpar a una tecnología concreta, sino de cómo se opera el sistema.

Luego pueden publicar mil informes, hablar de causas multifactoriales, repartir culpas, diluir responsabilidades o lo que necesiten para salvarse. En el sector eléctrico español, prácticamente todos sabemos lo que ocurrió, algo que se llevaba gestando desde hace meses y se intensificó especialmente en los días previos al apagón.

https://t.co/jlM4g4SPdw

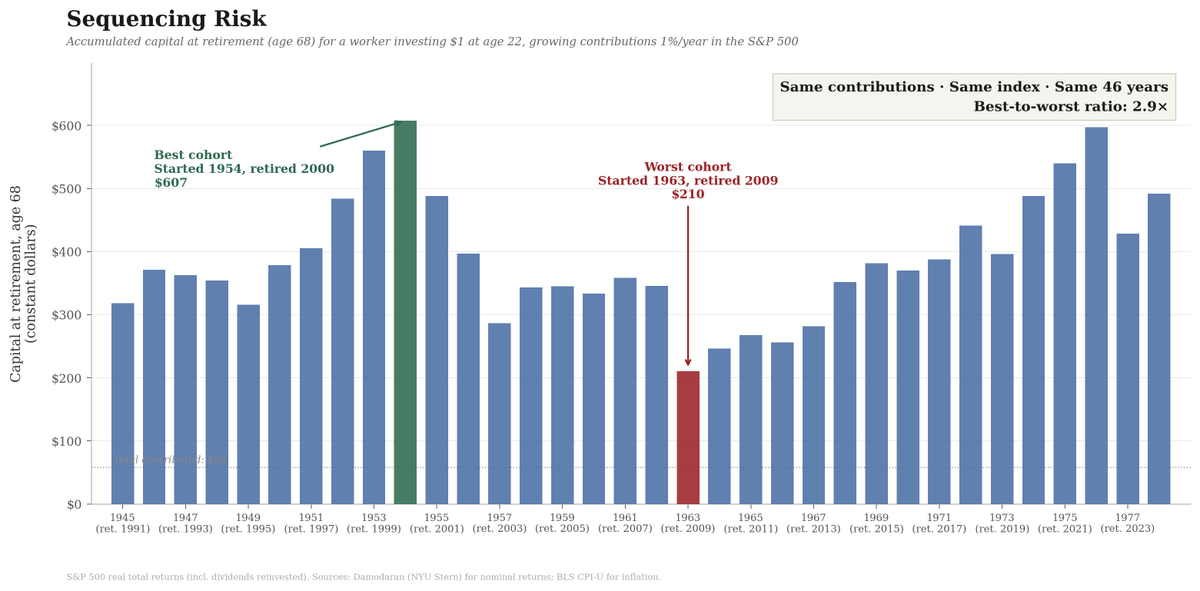

I am always amazed that most people saving for retirement (or designing optimal Social Security systems) rarely take sequencing risk seriously. Simply put, sequencing risk is the risk associated with the order in which returns arrive over one’s lifetime.

Sequencing risk hits you twice: while you are working and accumulating wealth, and again while you are retired and drawing it down. Today, I will focus on the first part. The retirement phase warrants its own discussion, and I will address it in a subsequent post.

Let me walk you through an exercise I ran yesterday using actual historical U.S. stock market data from the past 80 years to illustrate how important sequencing risk is.

I took the annual total returns of the S&P 500 (including reinvested dividends) from 1945 to 2024. The source is the dataset maintained by Aswath Damodaran at NYU Stern, a standard reference for long-run U.S. equity returns. I then deflated each year’s nominal return by the CPI-U inflation rate published by the Bureau of Labor Statistics to obtain real total returns, i.e., returns in constant purchasing power.

Over this 80-year period, the S&P 500 delivered a geometric mean real total return of about 7.5% per year. That is an impressive number. But this average return masks a lot.

Imagine a worker who starts investing at age 22 and retires at age 68. That gives them 46 years of contributions. In their first year, they contribute $1. Each subsequent year, they increase their contribution by 1% (roughly keeping pace with real wage growth). Every dollar is invested in the S&P 500. They never touch the money until retirement. No panic selling, no market timing, no strategy switching (and no management fees!). Textbook investing and waiting.

I ran this exercise for every possible cohort for which the data allow. The first cohort starts investing in 1945 and retires in 1991. The second starts in 1946 and retires in 1992. And so on, all the way to the last cohort, which starts in 1978 and retires in 2024. This yields 34 cohorts, each investing for 46 years, making the same contributions and investing in the same index. The only difference among them is which 46-year slice of historical returns they happen to live through.

The most fortunate cohort, the one that started investing in 1954 and retired in 2000, had $607 on the day of retirement (remember, all in real terms), with a real annual return of 8.82%. The unluckiest cohort, the one that started in 1963 and retired in 2009, accumulated $210, with a real annual return of 4.83%. Same contributions. Same index. Same strategy. Same investment horizon. Yet the luckiest retiree ended up with 2.9 times more wealth than the unluckiest.

Why? The 1954 cohort had a spectacular final decade. The late 1990s delivered some of the best equity returns in American history, and those returns compounded on a large portfolio built over decades. They retired at the peak, at the end of 1999, before the dot-com crash. The 1963 cohort was not so fortunate. They spent their last working years running straight into the 2008 financial crisis. The S&P 500 lost over 36% in real terms in 2008 alone. That loss hit their portfolio when it was at its largest, right before retirement, with no time left to recover.

Clearly, sequencing risk is not about the average return. Both the 1954 and 1963 cohorts experienced roughly similar average returns over their 46-year periods. The difference is when the good and bad years occurred. For the 1954 cohort, the bad years came early (when the portfolio was small) and the good years came late (when the portfolio was large). For the 1963 cohort, the opposite was true.

In fact, sequencing risk is even worse because poor returns in the stock market are correlated with weak labor markets: you have a much higher probability of losing your job (or seeing your wage income fall) precisely when the market is doing poorly, preventing you from saving when prices are low and equities are most attractive. However, let me set that point aside today to simplify the exposition.

The standard response of the financial planning industry to sequencing risk is the so-called glide path. The idea is simple: when you are young, you hold mostly equities. As you age, you gradually shift toward bonds. By the time you are near retirement, most of your portfolio is in bonds. A common implementation is a linear rule: start with 90% in stocks at age 22 and reduce the equity share steadily until you reach 20% in stocks at age 68. This is roughly what target-date retirement funds do.

The logic is sound in principle. You reduce your exposure to equities precisely when a crash would hurt you most. If 2008 happens when you are 65 and 80% of your portfolio is in bonds, the equity crash barely affects you.

I applied this glide path strategy to the same 34 cohorts, using historical real returns on the S&P 500 for the equity portion and real returns on 10-year U.S. Treasury bonds (from Damodaran) for the bond portion. Each year, the portfolio is rebalanced to the glide path weights.

The glide path does what it is intended to do: it reduces dispersion. The gap between the best and worst cohorts narrows from 2.9x under pure equities ($607 vs. $210) to 1.6x under the glide path ($292 vs. $178), but so does the upside. The best equity cohort (1954–2000) earned a geometric mean real return of 8.82% per year. The best glide path cohort (1975–2021) earned 6.59%. That is a 2.2 percentage point gap. Over 46 years of compounding, a 2.2 percentage-point annual yield yields an enormous difference in terminal wealth: the best glide-path outcome ($292) is less than half the best equity outcome ($607).

In other words, the cost of this insurance is substantial. In fact, the median cohort ends up meaningfully poorer under the glide path than under 100% equities. You are not trimming a bit of upside. You are forgoing a substantial share of your expected wealth at retirement.

This should not be surprising. Over the long run, equities have outperformed bonds by a wide margin. The equity risk premium is one of the most robust facts in finance. Every year you shift a dollar from stocks to bonds, you accept a lower expected return. Do this for 25 years of your career (roughly the back half, when the glide path has you increasingly in bonds), and the cumulative cost from foregone compounding is very large.

But the part that makes me most uncomfortable with the standard glide path advice is that bonds are not safe. People hear “bonds” and think “safe.” They are not. Bonds carry two risks that are easy to forget when inflation is low and interest rates are stable.

The first is inflation risk. A conventional bond pays you a fixed nominal coupon (yes, there are TIPS and similar instruments, but they have their own problems, so let me skip them for today). If inflation rises above the market’s expectations when the bond was issued, the real value of those payments declines. The cohorts that retired through the 1970s learned this the hard way. In the data, the real return on 10-year Treasuries was negative in multiple years during the 1970s.

The second is interest rate risk. When interest rates rise, the market value of existing bonds declines. The longer the maturity of your bond, the larger the hit. In 2022, the Bloomberg U.S. Aggregate Bond Index declined by approximately 19% in real terms. If you were 65 and had just shifted most of your portfolio into bonds following the standard glide path advice, you would have lost nearly a fifth of your “safe” allocation in a single year.

And here is the real sting of 2022: equities fell, too. The S&P 500 lost about 24.5% in real terms that year. The glide path assumes bonds will be there to cushion you when stocks fall. In 2022, both fell together. The cushion was not there. This is not some once-in-a-century event. Stocks and bonds have moved in the same direction before: the 1940s, the 1970s, and in 2022. The negative correlation between stocks and bonds that many investors take for granted is a feature of the disinflationary period from roughly 1982 to 2020. It is not a law of nature.

Let me be clear: I am not saying the glide path is wrong. For many people, it is the right choice. If a 30% equity crash near retirement would force you to sell assets at the worst possible time to cover living expenses, the insurance is worth paying for.

However, you should know what you are paying. The glide path (or variations of it that I am skipping in the interest of space) is not free. It entails substantial costs in expected returns. Worse, the insurance itself can fail. Bonds can lose money in real terms for extended periods. Bonds can fall at the same time as equities. The glide path reduces sequencing risk. It does not eliminate it. It also introduces risks of its own.

The deeper lesson from this exercise is that a substantial part of your retirement outcome depends on when you are born. You can do everything right (save diligently from your first paycheck, invest consistently, stay the course through every crash, never panic sell) and still end up with vastly different results than someone who did the same thing a decade earlier or later. The 1963 cohort did nothing wrong. They just had the misfortune of turning 68 in 2009.

No allocation strategy eliminates this. Even under the glide path, the best cohort ends up with substantially more than the worst. Sequencing risk is, to a significant extent, a matter of luck.

Next time: what happens when sequencing risk hits you in retirement, when you are drawing down instead of building up. The math there is, if anything, even more unforgiving.

🔴URGENTE| El exfiscal del Supremo Salvador Viada DENUNCIA la maniobra de la Fiscal General Teresa Peramato para salvar a García Ortiz de la expulsión de la carrera: “No se puede exigir a los ciudadanos el cumplimiento de la Ley cuando nosotros torcemos Ley de esta forma para nosotros mismos. Es un despropósito”.

‼️Ayer me llamó un lobbista para informarme de que Zapatero había sido clave en las negociaciones con Estados Unidos para liberar Venezuela. Me pidió que si lo publicaba en mis medios podía ganar una importante suma de dinero que me pagaría una consultora de comunicación. No me concretó cual pero imagino por donde van los tiros. Hoy varios medios como El Mundo publican ese relato y es obvio que Zapatero ha encargado una campaña de comunicación para despegarse públicamente del régimen chavista con el que se hizo millonario y evitar que las investigaciones que hay contra él en Estados Unidos sigan su curso. Hablé con varias personas de mi confianza en la Administración Trump para corroborar esa información y me aseguran que Zapatero no ha sido puente entre Trump y Delcy como se está haciendo creer y que él ha intentado por todos los medios tener interlocución directa con Washington DC a través de lobbistas y de la embajadora de España en DC, Ángeles Moreno Bau, quien lleva meses quejándose de que no tiene interlocución con nadie del Gobierno americano. En la Casa Blanca ya saben el papel qué jugó España de socio clave de la narcodictadura. Lo lamentable es que haya medios de supuesta derecha en España que se venden hoy a Zapatero como llevan haciéndolo meses. Urge investigar a periodistas o medios que se prestan al lavado de imagen de corruptos y que se venden al mejor postor.

Después de unos días de trabajo hago pública CONTRATACIÓN ABIERTA, una web donde se pueden revisar de forma fácil los contratos menores de las administraciones públicas de España.

Hay más de 7,3 millones de contratos y 11.700 organismos públicos.

👇👇

https://t.co/zBmiVJ6mTR

A las autoridades españolas les gusta darle protección a los delincuentes.

Por nosotros no hay ningún problema: nos ahorran el costo de tenerlos acá. Pero qué lástima por el pueblo español, que luego tendrá que pagar el precio de llenar su sociedad de criminales.

China 🇨🇳 ha presentado el diseño de un gran portacontenedores civil propulsado por energía nuclear de torio. No es un rompehielos, ni un buque militar, ni un experimento. Es un portacontenedores de los que sostienen el comercio global. El proyecto lo firma Jiangnan Shipyard y el horizonte que manejan es 2035.

Las especificaciones más ambiciosas presentadas por el astillero apuntan a un buque de hasta 25.000 TEU, en la liga de los mayores portacontenedores del mundo actual. Un gigante oceánico, pero sin depender de combustibles fósiles ni de repostajes constantes.

La clave está en el reactor nuclear. No sería un reactor convencional de agua a presión, sino un reactor de sales fundidas alimentado con torio. En este diseño, el combustible no es sólido, sino que está disuelto en una sal líquida. Esto permite operar a baja presión y elimina los escenarios de sobrepresión. Si algo va mal, la física hace el trabajo: la reacción nuclear se frena de forma pasiva, sin intervención humana.

El torio-232 no es directamente fisible, sino fértil. No se fragmenta al captar un neutrón, sino que se transforma en uranio-233 y se consume de forma muy eficiente dentro del reactor. Así, prácticamente todo el torio acaba convertido en material fisible, a diferencia de un reactor de uranio, donde solo fisiona alrededor del 4-5%. Además, el torio es cuatro veces más abundante que el uranio, genera menos residuos a largo plazo y presenta menos riesgos de proliferación. No es una idea nueva ni experimental: es una tecnología conocida y China ya opera un reactor experimental de torio.

Las ventajas son claras: autonomía durante toda la vida útil del barco, emisiones operativas nulas, costes de combustible irrelevantes y una independencia energética total. Un buque así no depende del precio del petróleo ni de tensiones geopolíticas en las rutas de suministro. El principal inconveniente es el regulatorio, que todavía está en desarrollo, aunque avanzando a gran velocidad.

https://t.co/d5XSXDwmAK

¿Hacen falta más pruebas de que el cierre nuclear de Alemania, y el que pretenden algunos en España, es un auténtico suicidio energético?

Quienes me seguís sabéis que llevo nueve años advirtiendo que el cierre de los 17 reactores de Alemania solo serviría para abrazar el gas y el carbón, encarecer la energía, entorpecer su descarbonización y debilitar su seguridad energética. No era una opinión, era un pronóstico basado en datos. Y también avancé que, tarde o temprano, acabarían replanteándose aquella decisión.

El tiempo me ha dado la razón en Alemania. Ojalá no tengamos que comprobarlo también en España.

https://t.co/hA1ZboaOca

Nuclear and Hydro Linked to Lower Electricity Prices. Wind and Solar are Not.

I often hear the phrase “Wind and solar lower electricity prices", but is that really true? I decided to plot the data.

Looking at the average spot market price (no taxes or tariffs) across 30 European countries in 2024, wind and solar seem to have no effect on electricity prices. The weighted regression actually shows a slightly positive slope, meaning prices go up as the share of wind and solar increase, but it is far from statistically significant (R2 = 0.03, p = 0.4).

In short: wind and solar explain nothing about a country’s electricity price.

On the other hand, when looking at clean firm power sources like hydro and nuclear, the explanatory power becomes much stronger.

Using a Weighted Least Squares (WLS) regression across 30 European countries, weighted by total electricity production, there is a clear and statistically significant relationship (R2 = 0.4, p < 0.001). Countries with more hydro and nuclear tend to have lower electricity prices. Of course, this does not explain all the variation, since plenty of other factors matter too.

But it sends a clear signal: hydro and nuclear are linked to cheaper electricity, while wind and solar are not having any measurable effect in either direction.

Angel Escribano preside Indra y hace que Indra compre su propia empresa por €1.500M. El pelotazo: valoración multiplicada por 15 en tres años gracias a contratos públicos. SEPI controla el 28% y aprobará la compra. El capitalismo de amiguetes sin disimulo.

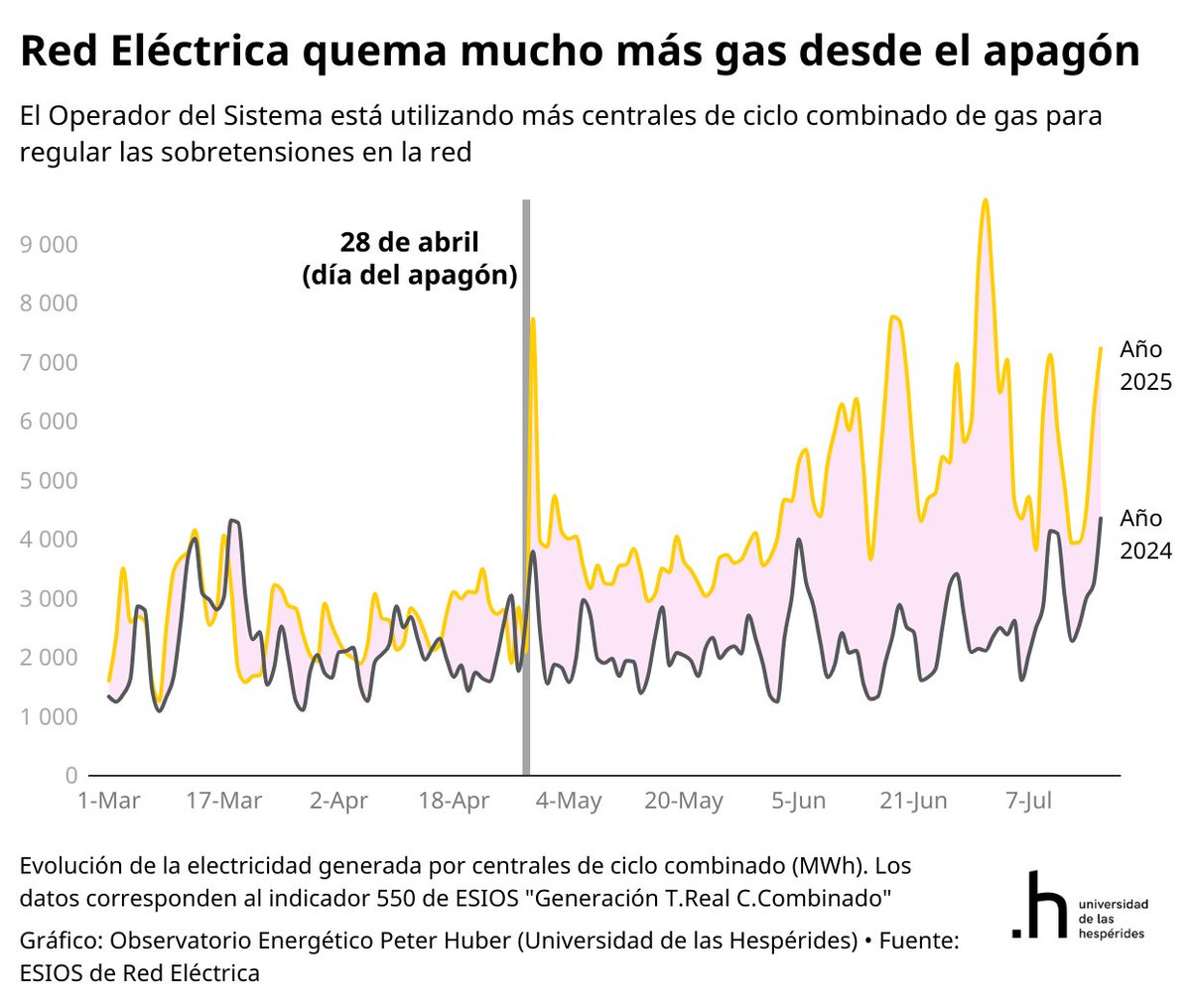

Mirad cómo está operando Red Eléctrica desde el apagón.

Quemando gas como si no hubiera un mañana para controlar las sobretensiones.

Pero tratan de convencerte de que la falta de potencia síncrona no tuvo nada que ver en el apagón... 🤣🤣🤣