Extrovert,Reader,Writer,Cyclist,Investor, Blogger

An Engineer by profession , An Artist by heart 😘

#RealistOptimist , Knowledge Sharing , No Recommendations

I always wanted to be a writer since my childhood. Starting with small 4 liner Haiku , to English, Hindi and Marathi poems , Financial blogs at Investeek and Now on Amazon writing my own books. I am living my dream with consistent time and efforts spent.

https://t.co/n0NAn096OB

Investing is the ultimate mind game. You need a win, even a small win, in the portfolio every so often to keep your self-confidence. If you’re struggling stop yourself from getting super concentrated into fewer positions. This is how stock pickers go extinct. Do the opposite - add a position or two to give you more chances at getting a hit to mentally stay in the game.

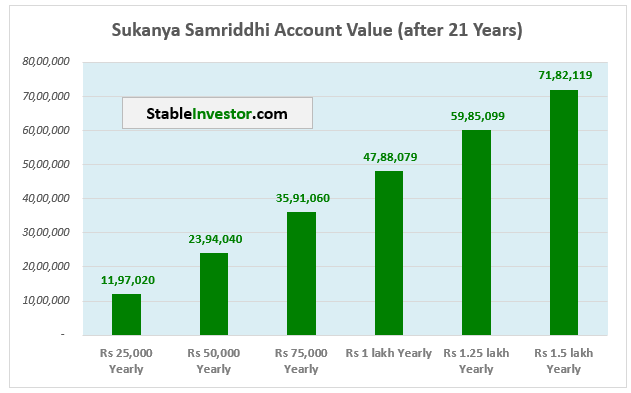

How much corpus can you create using Sukanya Samriddhi Account after 21 years?

Sukanya Samriddhi Yojana gives 8.2% per annum. As per rules, the account matures in 21 years (of account opening, and not at girl’s age of 21). Also, you can only make investments for the first 15 years. For the remaining 6 years, you can’t invest more, but your account keeps earning interest. And the maximum you can invest in a year is Rs 1.5 lakh.

How much corpus can you create using a Sukanya Samriddhi Account after 21 years?

Rs 25,000 yearly – Maturity amount is Rs 11.97 lakh

Rs 50,000 yearly – Maturity amount is Rs 23.94 lakh

Rs 75,000 yearly – Maturity amount is Rs 35.91 lakh

Rs 1.00 lakh yearly – Maturity amount is Rs 47.88 lakh

Rs 1.25 lakh yearly – Maturity amount is Rs 59.85 lakh

Rs 1.50 lakh yearly – Maturity amount is Rs 71.82 lakh

Would these amounts be enough for your daughter? It depends on each parent’s view. But mind you, these are figures after 21 years.

Even nowadays, good professional courses in India can easily cost Rs 20-25 lakh. And if you inflation-adjust these figures for the next 15-20 years, then the amount required for similar education would be a much bigger number.

So chances are that the amount accumulated via Sukanya may not be enough. Also, there is a debatable Sukanya rule which allows withdrawal up to 50% of this corpus for higher education.

Solution?

It's actually simple, and many of you already do it.

If your daughter is still young and you still have 10+ years before her higher education expenses begin, then you need to invest some money in equities.

Sukanya, no doubt, is a solid product. But it’s a debt product which currently offers 8.2%. And many educational courses witness much higher inflation, at least in the pre-AI era. So to generate inflation-beating returns, you need to have some allocation to equities.

How much you should allocate between equity funds and Sukanya for your daughter’s future depends on your risk profile. If you aren’t conservative, then having a higher allocation to equity is better, assuming your daughter is young and you have several years before her higher education starts.

A few suggestions:

- If you are ultra-conservative, then just stick with 100% in Sukanya and PPF.

- If you only want to take limited risk, then have 60-75% in Sukanya and/or PPF and the remaining 25-40% in equity funds.

- If you are moderately aggressive or more, then 75% or more can be put into equity funds.

Disc - Just my thoughts with numbers. Don't consider the above as investment advice, please.

Dev Ashish (SEBI RIA, INA100005241) @StableInvestor

The govt should lead by example .

For next 12 months - all bureaucrats should stop using Lal batti and use Metro for work travels.

Also pool govt cars .. all bureaucrats in one dept can pool the car…

The right direction in life always involves living in an environment that fills you up every day with energy, ambitions, and ideas that you didn't know you had in you.

You have your goals. I call the way you will operate to achieve your goals your machine. It consists of a design (the things that have to get done) and the people (who will do the things that need getting done). Those people include you and those who help you. For example, imagine that your goal is a military one: to take a hill from an enemy. Your design for your "machine" might include two scouts, two snipers, four infantrymen, and so on. While the right design is essential, it is only half the battle. It is equally important to put the right people in each of those positions. They need different qualities to do their jobs well--the scouts must be fast runners, the snipers must be good marksmen--so that the machine will produce the outcomes you seek. #principleoftheday

8 income sources that can be tax-free in India (FY 26)

Most people focus only on deductions.

But some incomes are simply not taxable if conditions are met.

Here are 8 such income sources you should know 👇

15 GREAT MINDS TO LEARN FROM ONLINE:

1. Naval Ravikant (Wealth)

2. Jordan Peterson (Responsibility)

3. David Goggins (Mental Strength)

4. Andrew Huberman (Health)

5. Chris Williamson (Modern Thinking)

6. Jocko Willink (Discipline)

7. Nassim Taleb (Probability)

8. Robert Greene (Strategy)

9. James Clear (Habits)

10. Alex Hormozi (Business)

11. Cal Newport (Deep Work)

12. Morgan Housel (Money Psychology)

13. Tim Ferriss (Performance)

14. Ray Dalio (Principles)

15. Failures and setbacks (Experience)

Over the last month, I have scanned 100+ companies across 10+ sectors.

Here's a thread on 19 companies from New Age platforms and capital markets sector.

A detailed thread ⬇️

So many people with the best intentions fail to be good parents because they never understood that education was never about telling their kids what to do, but about the efforts, the values, the ambitions they embodied in their daily lives. You won't raise an emotionally healthy, mentally strong, bold and confident kid unless you are such a person first.

Sensex completes 40 years of existence today.

In the last 4 decades, it has delivered a staggering absolute return of 15,594% or 15% CAGR (TRI).

97 companies have been a part of this cohort but only 6 stayed the course over this period.