- $AAOI at $12B

- $SIVE at $2B

- Foci at $2.8B

- Shunsin at $2B

Usually the best risk/reward to me currently. Lot of my answers before like $AXTI already 10x’d, so different lineup this time.

$AAOI due to absurd H1 2027 revenue projections from capacity ramp, doing everything from laser fab to assembly in America.

$471M/month… that’s in 2027, the TAM increases exponentially in 2028.

$SIVE is also ramping absurdly high, 77% revenue pipeline growth of the entire company’s history to ~$799M

Primarily from photonics… in a single quarter. And they’re projecting 60% gross margins off that.

Foci - $NVDA / $TSM primarily FAU supplier and bottleneck for COUPE. Genuinely not sure how this is $2.8B.

BOM share for their passive components + FAU are massive in 2028. Just a bit early H1 2026.

Shunsin - Legit you see Foxconn get CPO/photonics related orders over and over for $NVDA and others.

Just nobody knows the packaging/testing gets done by Shunsin.

A lot of contracts are also under Shunsin’s subsidiary too.. so markets/algorithms don’t know what’s coming imo.

Runner up is $XFAB, they’ll probably be central to EU CHIPS act 2 for silicon photonics at ~$1.5B MC.

And of course SiC/GaN foundries should go brr with 800vdc push by Nvidia.

Especially if they’re the only high volume one in United States per Dpt. Of Commerce.

And it’s such a low price/book ratio so you’re kinda getting the company upside for free, while US Gov/EU Gov subsidize their capex.

“China is the model for many nations.”

- Klaus Schwab

Christine Legarde ECB👇explains how the Chinese #CBDC is a good example because it’s “good for … all citizens … not just the elites.”

https://t.co/pkoLGWrM1H

✨ The portal has opened. ✨ At 11:11, abundance aligns.

The first drop of FCOOKIE NFT is live.

It’s a manifestation a gateway between art, fortune, and frequency.

#FCOOKIE#F4CAI#NFT#Web3#FortuneCookies#1111Portal

It’s not a debate anymore - crypto and stablecoins are the tools that will update the global financial system.

Excited to be collaborating with @Citi to work on improving stablecoin utility and digital asset adoption with their clients.

Some people ask why is #BNB so strong?

While others tried to ignore, hide, shift blame, or attack competitors, the key @BNBChain ecosystem players (Binance, Venus, and more) took hundreds of millions out of their own pockets to PROTECT USERS.

Different value systems. 💪

Why China’s Rare Earth Dominance Is No Accident—and Why the U.S. Faces a 15-Year Climb to Catch Up

In the global race for technological supremacy, the battlefield is not just in silicon chips or AI algorithms—it’s buried deep in the earth, in the form of obscure-sounding elements like neodymium, dysprosium, and terbium. These rare earth elements (REEs) are the lifeblood of modern defense systems, electric vehicles, wind turbines, and advanced electronics. And right now, China doesn’t just dominate the rare earth market—it owns the entire chessboard.

The Illusion of a Mining Problem

It’s tempting to think of rare earths as a simple resource extraction issue. After all, the U.S. has rare earth deposits. So do Australia, Canada, and Brazil. But this isn’t about digging rocks out of the ground. It’s about what happens next: the processing, separation, metallization, and magnet fabrication—a complex, capital-intensive, and expertise-driven industrial chain that China has spent decades mastering.

China controls over 85% of global rare earth refining capacity. But more critically, it has a near-monopoly on the specialized machinery—solvent extraction trains, reduction furnaces, spin casters—and the technical workforce needed to operate them. The U.S. can’t simply buy this equipment anymore. Beijing has blocked exports of key processing technologies, turning the machinery itself into a geopolitical weapon.

The Machinery and Expertise Bottleneck

This is the real choke point. Western companies now face the daunting task of reverse-engineering or reinventing entire classes of industrial equipment. That’s not just a procurement challenge—it’s a multi-year R&D slog involving corrosive chemicals, high-temperature metallurgy, and environmental hazards. And even if the machines are built, who will run them? The U.S. lacks the institutional knowledge and trained workforce that China has cultivated since the 1980s.

This is why even the most optimistic projections suggest it will take 10 to 15 years for the U.S. to build a fully independent, end-to-end rare earth supply chain. That’s assuming sustained political will, massive public-private investment, and a bit of luck.

The Strategic Cost of Complacency

For too long, the West outsourced its rare earth needs to China under the illusion of market efficiency. But rare earths are not just commodities—they are strategic enablers. Every F-35 fighter jet, every hypersonic missile, every next-gen radar system depends on components made with rare earth magnets. So do the motors in Teslas and the generators in offshore wind farms.

China understands this. Its dominance is not accidental—it’s the result of deliberate industrial policy, subsidies, environmental trade-offs, and long-term strategic planning. The U.S., by contrast, is playing catch-up in a game it didn’t realize it was losing.

The Path Forward: Painful but Necessary

The U.S. is finally waking up. The Department of Defense is investing hundreds of millions into companies like MP Materials to build vertically integrated mine-to-magnet operations. The Department of Energy is funding next-gen separation technologies that could leapfrog the current solvent-based systems. And allied nations like Australia and Canada are stepping up to form a “friend-shored” supply chain.

But let’s be clear: this is not a one-election-cycle problem. It’s a decade-plus industrial transformation. It will require trial and error, environmental compromises, and a new generation of metallurgists, chemists, and engineers. It will also require the political courage to treat rare earths not as a niche issue, but as a national security imperative.

Conclusion

China’s stranglehold on rare earths is not just about minerals—it’s about systems control. The U.S. can’t mine its way out of this. It must build, train, and innovate its way back into the game. That will take time—perhaps 15 years or more. But the cost of inaction is far greater: a future where the technologies that define power are built on foundations the U.S. no longer controls.

1/2

Rare earths aren’t actually rare.

Finding them isn’t the challenge, processing them is.

China produces approximately 60% of the world’s rare earth minerals and performs up to 90% of the refining needed to make them usable.

These metals are critical for AI, chips, weapons, and advanced manufacturing.

The U.S. still sources roughly ~70% of its supply from China.

"Some countries would smuggle🇨🇳rare earth,

fly it to a port, to be exported to the🇺🇸United States. No way. It's not going to save the U.S."

💥Shen Shiwei vs. Victor Gao Zhikai

Why🇨🇳China scaled-up export controls of #RareEarths and related technologies?

My YouTube Channel: https://t.co/iiklV9A8G8

They lost faith. We found fortune. 🥠💫

$F4CAI rises where markets fall.

Fortune is coming. 发财气起!🔥

#F4CAI#发发发#CryptoRevival#Web3Luck

https://t.co/otMfwHIIrA

Something lucky is baking on-chain... 🥠

The Fortune Cookie of Web3 is almost ready to drop. 🍀

$F4CAI — 一饼在手,天天发财 💫

#F4CAI#发发发#BNB#BTC#ETH#MemeRush

https://t.co/otMfwHJgh8

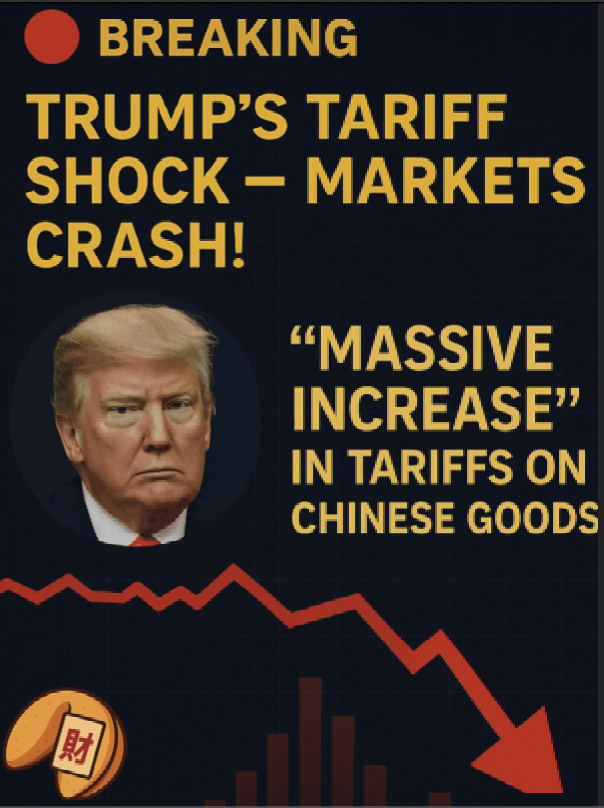

El desplome que estamos viendo en el S&P 500 y en las criptomonedas trae su causa en Trump sube al 100% los Aranceles sobre China y endurece el control de las exportaciones.

Se avecina un volátil fin de semana.