huh.. seems like I'm kinda a Codex OG?

Almost started using it at the same time than @ajambrosino

Looking back, it really came a long way, impressive what codex became vs almost 1 year ago

Those post had $XFAB shoot up +30% in a few minutes and the stock market had to pause trading for 3 hours.

Crazy influence.. and hype?

Btw, trading is open again since a few minutes ;)

$XFAB (photonics + power semis) is an interesting long idea at $1.28B MC, that I took positions in.

Given EU CHIPS act 2 is today as the catalyst for European photonics players.

> 800 VDC power semi exposure to $NVDA push through $NVTS + $POWI

> Silicon Photonics / CPO exposure with $NVDA as evaluation stage for high volume manufacturing (optical transceivers/switches)

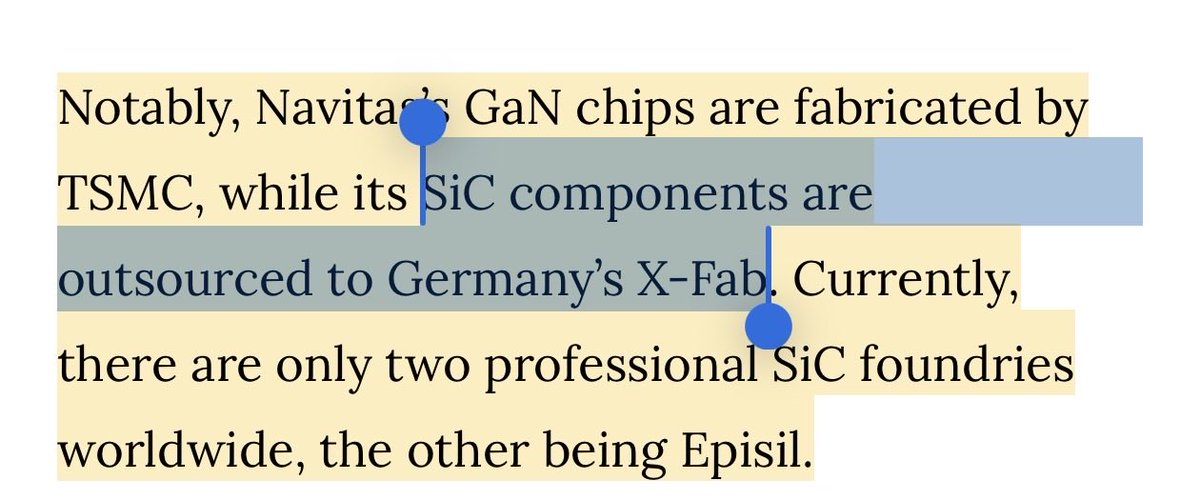

> The only high-volume SiC foundry in the US.

> One of the critical MEMS foundries

> ~1.29 P/B, which was around what $SOI was sitting at when I went long. Depressed valuations due to legacy drag

> ~6.5-8.5 fwd p/e 2028 personal est.

> backstopped by Government:

- EU CHIPS act, $128M Euros

- US CHIPS act $50M PMT (department of commerce).

With likely more coming (just signals critical importance to Western supply chains).

So at a certain point with all the grants, they’re just getting the capex funded by the Governments.

EU CHIPS act 2 is coming out this week, and I’m gonna go ahead and guess $XFAB might get included given they were before, and this package is specifically targeting photonics.

~$1.3B MC seems compelling to me if it can pull a Soitec reversal (low p/b, very high growth segments, auto legacy drag).

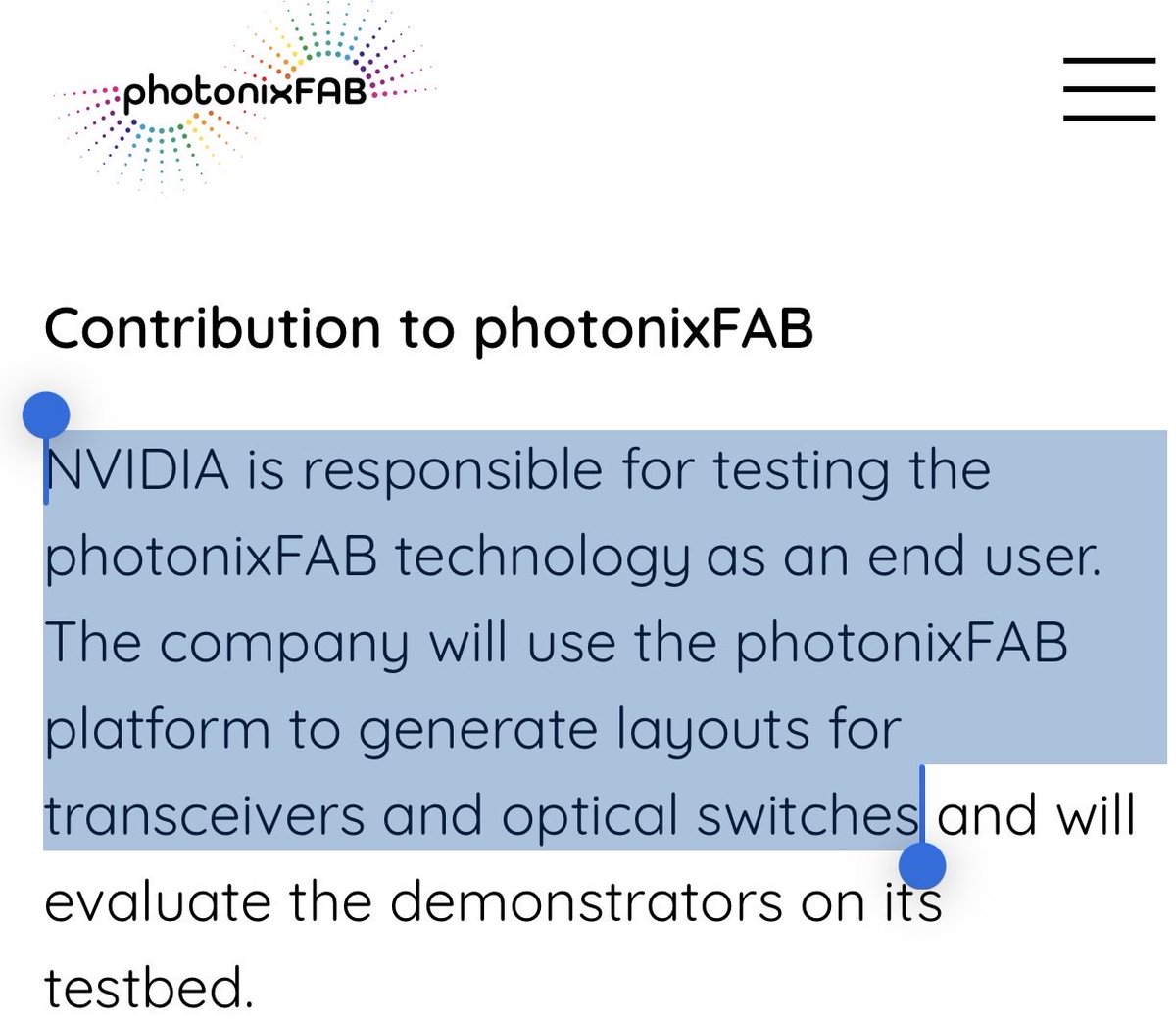

As for the $NVDA silicon photonics relationships it’s under “photonixFAB”.

Markets probably missed this silicon photonics relationship (like $TSEM when I went long) with Nvidia since XFab leads this… Just under a different name.

For power semis, XFAB is named for SiC + $NVTS. In PCN-22181, $POWI explicitly names XFAB as its foundry.

Given its exposure to power semis and photonics as growth, low P/B, gov backstop (of course dyor, just sharing my personal thoughts)

Thought it personally seemed compelling.

Yes, but it is not clear yet that management wants to go full speed in that direction.

In fact, shareholder asks on the 4th June investors to "refuse discharge of management", basically a formal protest vote.. topic:

-> Should LPKF keep funding LIDE through cost discipline, or raise €50-100m to accelerate Advanced Packaging?

Management decided to be cautious with their North Star approach. This shareholder wants to push for faster LIDE push, potentially also involving dillution.

So it will be interesting to see if/how management even want to embrace that opportunity you are pointing out!

Is $AXTI InP position defensible, or can InP be replaced?

With the run this stock had, I had a look at the basic assumption, namely: if it runs based on their InP access and tech, can they defend that position?

In short: InP is hard to replace for many high-speed optical applications, but AXTI is not immune to substitution or competition.

Why InP matters:

Silicon is excellent for waveguides and photonic integration, but silicon is an inefficient light emitter. For telecom/datacom wavelengths such as 1.3 μm and 1.55 μm, InP-based materials are very important because they can generate and amplify light efficiently. That is why silicon photonics often still needs InP lasers, either bonded, integrated, or externally coupled.

But there exist also a few subtition paths:

1. Other InP suppliers: Sumitomo, JX, Freiberger, Coherent/internal capacity, Xiamen Powerway, etc.

2. Hybrid platforms: InP-on-silicon, InP-on-GaAs, transfer printing, bonded III-V dies.

3. Different optical architectures: silicon photonics with remote lasers, thin-film lithium niobate modulators, GaAs in some wavelength bands, etc.

4. Vertical integration: Coherent/Lumentum-type players may internalize more of the supply chain.

So basically, it is not a "lock-in" kinda situation for $AXTI but it does look good.

Interesting drama for $LPK on the 4th June!

A shareholder asks investors to "refuse discharge of management", basically a formal protest vote.

The topic is about capital allocation, and critical for the thesis around CPO bottleneck that @aleabitoreddit has shared. The vote is about:

-> Should LPKF keep funding LIDE through cost discipline, or raise €50-100m to accelerate Advanced Packaging?

Management decided to be cautious with their North Star approach. This shareholder wants to push for faster LIDE push, potentially also involving dillution.

So, very interesting to see how other investors vote and what the consequence and decision will revolve around. I am quite sure it will provide valuable hints as to what to expect in the '26 from LPKF in terms of market capture of the CPO opportunity with LIDE (the core thesis behind the price run of the $LPK)

CPO will boom, so $LPK will profit?

Well maybe, but there is some assumptions and gaps to bridge here. Basically:

i) CPO adoption

does not automatically imply

ii) glass substrate adoption

does not automatically imply

iii) LIDE adoption

does not automatically imply

iv) LPKF revenue explosion

- A more accurate investment chain is:

AI scale drives need for CPO / optical I/O

↓

Some CPO and AI packaging architectures may benefit from glass

↓

If glass substrates/interposers require high-quality TGVs and microstructures

↓

If LIDE is qualified as the preferred production process

↓

Then LPKF may capture a valuable bottleneck equipment role

LPKF is therefore a second-order bottleneck thesis, not a direct CPO supplier. LPKF becomes interesting if LIDE becomes a required production tool for glass substrates/TGVs in AI/HPC advanced packaging. This remains to be seen.

Why is the earning call from $NVIDA yesterday good news for companies involved in CPO?

Well, NVIDIA expect $20 billion in standalone Vera CPU revenue this year, which is a surprise. This is completely outside the prior $1 trillion Blackwell + Rubin GPU forecast.

For context, Vera CPU are designed for agentic work and agentic AI workloads are ramping much faster than most models assumed. These workloads are more CPU-intensive (orchestration, multi-step reasoning, simulation, tool use) than pure GPU training/inference. The CPU-to-GPU ratio in next-gen AI factories is rising, and standalone CPU-only deployments are happening sooner and at larger scale than expected.

So how does that connects to CPO? Well it is demand that is rising much faster than expected. Demand that will increase the need for solutions to scale operation for data center, such as CPO. But obviously, the more obvious winners of this acceleration should also be CPU-companies, and CPO is a second-order beneficiary. So from a CPO perspective:

- More Vera CPUs = larger, more complex AI factories.

- Larger factories = much higher bandwidth, lower power interconnects.

-> This directly accelerates the shift from copper/pluggable optics → CPO at scale.

So overall, this agentic CPU demand is good news for $SIVE but also companies like $ARM $MU $TSM etc

@oguzerkan That's not why. It's rather a consequence of degrowth regulation. And this is coming from a general regrowth mindset in the eu.

Though I feel some are starting to wake up

@kimmonismus The speed and scale at which AI will basically change everything, is also why some people are confused that interest rates as high as they were during the 08 crisis, don't cause a market crash

Ai-induced growth will outgrow high interest negative impact

Exactly.

The interesting part is the category shift: $TE is starting to trade less like generic solar and more like scarce US energy supply-chain capacity for AI/data centers.. so basically: the AI-power narrative

Next proof point is whether G1 margins repeat and G2 Austin gets financed cleanly

$TE is up over 25% today as the market starts recognizing T1 Energy’s push to become a scaled U.S. solar manufacturing platform.

The market is starting to treat domestic solar capacity as part of the AI power buildout, not just another clean energy trade.

CPO will boom, so $LPK will profit?

Well maybe, but there is some assumptions and gaps to bridge here. Basically:

i) CPO adoption

does not automatically imply

ii) glass substrate adoption

does not automatically imply

iii) LIDE adoption

does not automatically imply

iv) LPKF revenue explosion

- A more accurate investment chain is:

AI scale drives need for CPO / optical I/O

↓

Some CPO and AI packaging architectures may benefit from glass

↓

If glass substrates/interposers require high-quality TGVs and microstructures

↓

If LIDE is qualified as the preferred production process

↓

Then LPKF may capture a valuable bottleneck equipment role

LPKF is therefore a second-order bottleneck thesis, not a direct CPO supplier. LPKF becomes interesting if LIDE becomes a required production tool for glass substrates/TGVs in AI/HPC advanced packaging. This remains to be seen.

For those going into the LIDE & CPO rabbithole and then came accross $LPK, here is the small but important point:

It is a SME German manufacturer.

Not lying, it's literally what convinced me at the end to invest in it (in addition to all other factors). Germany has been for like 50+ years leading worldwide in niche manufacturer products and tech. They have the knowledge, the people and culture for it.

So, I find it quite exciting to find such a relatively unknown german manufacturer, small/SME, niche tech, IP and positioned to dominate with a semi-monopoly in a area that might become a bottleneck in enabling our AI future. Though still quite speculative.

I'll share later a summary of the deep dive I did on that company.

$AAOI is being hyped as the USA-play for pluggables, which is fair. US centric supply chain will only gain in importance, and pluggables will still matter for 1-2+ years at least.

CPO is the tech that will likely replace it with rising demand in speed, as soon as 1.6T pluggables will not suffice anymore. But realistically this will happen at scale only starting in '27.

Therefore, investing in AAOI and others is still a decent short-term play, and investing in CPO centric plays, like $SIVE makes sense to ensure to be positioned in time.

Both trades make sense, both trade will likelly overlap.

By now, you might have heard that "CPO is the next bottleneck". And somehow heard about InP substrates, waffers, LIDE etc, and many get confused about all that. Understandable.

First step in building conviction is to actually understand what CPO is, and how it even fits in the AI adoption story. Without these absolute basics, you'll get miserable with the price swings.

1) What is CPO:

CPO = co-packaged optics. Instead of placing the optical module at the front panel of the box, CPO moves the optical engine much closer to the switch ASIC or accelerator package.

- Traditional pluggable:

ASIC → long electrical path → front-panel optical module → fiber

- CPO:

ASIC → very short electrical path → optical engine near/on package → fiber

The key benefit is that the electrical path becomes much shorter. That reduces power, improves bandwidth density, reduces signal-integrity issues, and can help future switch chips scale to enormous throughput.

The key disadvantage: Harder thermal management and harder to repair.

2) How does CPO even fit in the AI story:

Well, it is the solution for a problem that people expect to soon have, namely increasing hardware demand. Speed will rise from 400G to 800G to 1.6T and beyond. With that electrical links require more equalization, retimers, power, cooling, and board complexity. The longer the electrical signal has to travel at high speed, the worse the power and signal-integrity problem becomes. And simply said, CPO dramatically reduce this travel. hence a solution for a problem the industry expect to soon have, though current solution are still "good enough" for the status quo.

@aleabitoredditmade made me curious about this topic, so I'll share some easy to understand bits about it along the way.