Elon is still deeply optimistic about AI.

He does not seem to see a ceiling yet. For him, AI is still a straight-line acceleration story: more compute, better models, more robots, higher productivity, and eventually a bigger economy.

@Scobleizer There are always momentary dips, even in a rapidly growing economy.

The productivity gains from AI and robotics are so enormous, however, that the macro trend is overwhelmingly up.

I wonder if humanoids is going to spark a new bottleneck/industry for robot cosmetics.

Like a skin bottleneck. Or Aespa KPOP robot makeover as a service.

So if $TSLA Optimus makes tens of millions of humanoids:

Who’s going to make them all look hot?

South Korea is quietly becoming one of the more interesting robotics markets in the world.

Goldman Sachs estimates that Korean companies could account for around 30% of global humanoid robot production by 2035, not only through direct manufacturing, but also through critical components like actuators, sensors, motors, control units, and precision engineering.

That matters because humanoid robots are not just an AI problem. They are also a hardware, manufacturing, supply chain, and industrial execution problem. This is exactly where South Korea already has structural advantages.

The country has deep expertise in autos, electronics, batteries, semiconductors, factory automation, and precision components. In humanoids, that translates directly into actuators, robotic hands, motion systems, sensors, and industrial deployment. The same way Korea became critical to the AI cycle through memory, HBM, and semiconductor supply chains, it could also become critical to the robotics cycle through the physical layer of humanoid robots.

China has the advantage of scale, manufacturing speed, and state-backed industrial policy, while the US has frontier AI, software, and model-layer dominance. South Korea sits in a different but important position. It may become one of the key execution layers for humanoid robots, supplying the advanced components and manufacturing capability needed to turn robotics from a lab demo into a scalable industrial product.

This is also why the KOSPI story may still be underappreciated. Investors are already starting to recognize Korea as an AI memory winner through HBM and advanced semiconductor supply chains, but the market may not be fully pricing in the possibility that Korea also becomes a major beneficiary of the physical AI cycle.

If humanoid robots become the next major technology platform after generative AI, the value will not only accrue to software companies or robot brands. A large part of the value could flow to the suppliers that provide the motors, actuators, sensors, batteries, chips, and manufacturing systems behind the robots.

That makes South Korea interesting because it is not trying to compete only at the narrative layer. It already owns many of the industrial capabilities required for the next phase. If AI was the first wave, humanoid robotics could become the second wave, and Korea may once again sit near the center of the supply chain.

The market may still be valuing Korea like a cyclical semiconductor economy, when it could increasingly deserve to be valued as a strategic supplier to both the AI and robotics supercycle.

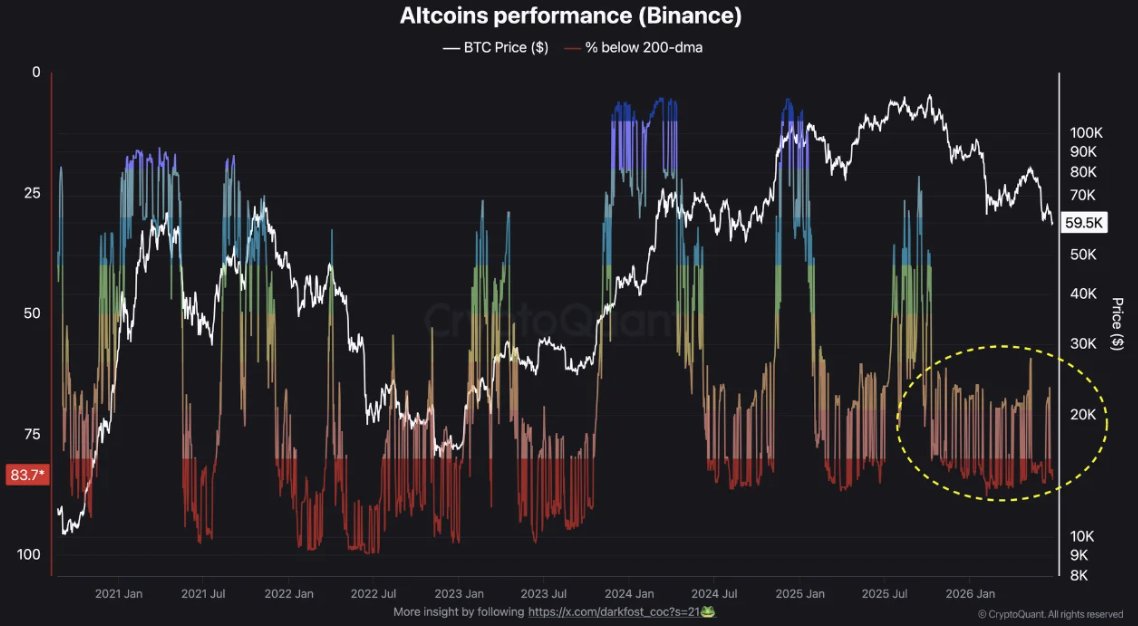

The fact that ~84% of Binance-listed altcoins are trading below their 200-day moving average is not just a technical signal of weakness. It reflects a regime-wide breakdown in trend structure across the entire altcoin complex. In market microstructure terms, the 200-DMA is a proxy for sustained directional participation; when the vast majority of assets sit below it, it implies that reflexive momentum has fully inverted into distribution. Liquidity is no longer chasing upside, it is being systematically unwound.

What makes this more important is that the weakness is no longer isolated to small-cap or illiquid tokens. Even large-cap benchmarks are showing stress: Bitcoin, Ethereum, and Solana have all experienced drawdowns consistent with a broader risk-off phase rather than idiosyncratic corrections. When correlation across majors converges this tightly, crypto stops behaving like a segmented asset class and starts behaving like a single high-beta liquidity instrument. The distinction between “blue chip” and “alt” becomes mostly cosmetic in down cycles.

At the same time, this kind of breadth compression usually signals a deeper narrative transition. The market is no longer rewarding speculation at the periphery, and even core narratives are struggling to attract incremental capital. Platforms like Binance simply reflect that flow reality: fewer sustained bids, faster rotations, and weaker conviction across the board. In that environment, crypto is no longer the “shiny object” absorbing marginal liquidity the way it did in prior cycles.

The structure looks less like a sector rotation and more like a full re-pricing of the asset class. Call it what it is: crypto winter.

84% of Altcoins are trading below their 200-DMA

“Approximately 84% of altcoins listed on Binance are in a state of total underperformance, trading below the key technical threshold of the 200-day moving average.” – By @Darkfost_Coc

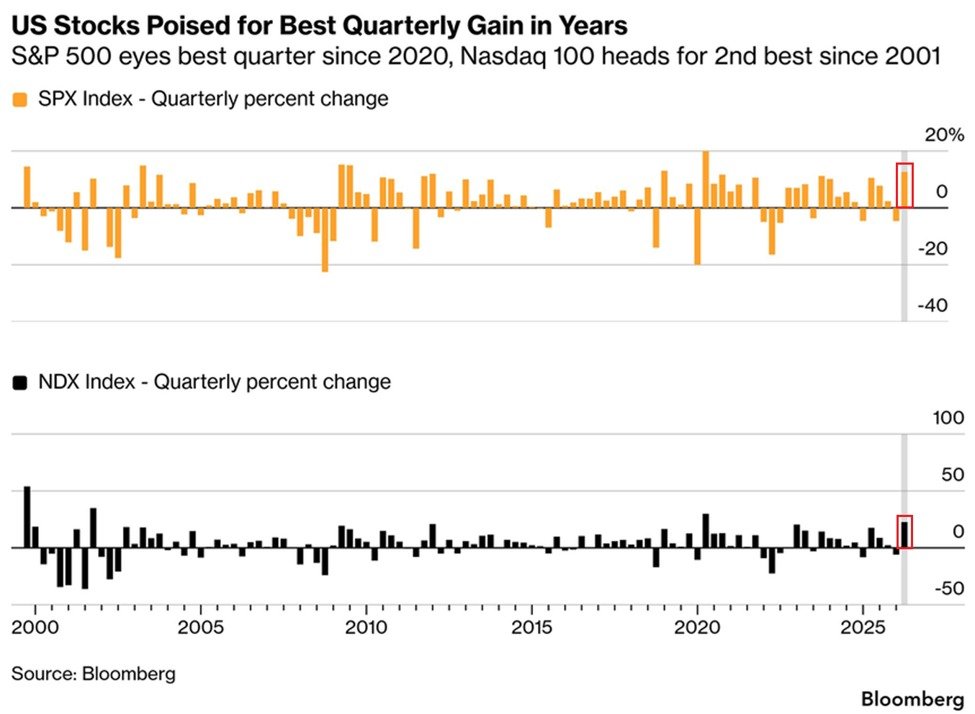

The S&P 500 being on pace for its best quarter since 2020 is not just a simple “stocks are bullish again” signal.

Behind every strong index rally, there is usually one dominant narrative that becomes large enough to pull capital into the same direction. In 2020, that narrative was technology. Not just because tech stocks were popular, but because the market realized that digital platforms, cloud, software, e-commerce, and online services were becoming the safest and most scalable assets in a locked-down economy.

That rally was built on a simple idea: if the physical economy is disrupted, the digital economy becomes more valuable. Capital moved into companies that could grow without depending too much on physical activity. That is why large-cap tech became both a defensive trade and a growth trade at the same time.

The current rally has a different engine. This time, the dominant narrative is AI. But AI is not only about chatbots, models, or software apps. The real market story is the infrastructure required to scale AI: semiconductors, GPUs, memory, networking, cloud capacity, data centers, power, cooling, and the full compute supply chain behind it.

That is why semis and AI infrastructure have become so important to the index. The market is not only pricing current earnings. It is pricing a multi-year capex cycle where every hyperscaler, enterprise, and AI lab needs more compute. In this cycle, the bottleneck is not user adoption. The bottleneck is capacity.

This is what makes the rally powerful but also concentrated. The S&P 500 can look extremely strong even when the leadership is narrow, because the companies tied to the dominant narrative carry a large weight in the index. When capital clusters around the same theme, index performance can move much faster than the broader economy.

So the real lesson is not simply that 2020 was tech and 2026 is AI.

The lesson is that the market rewards the companies closest to the biggest constraint of the cycle. In 2020, the constraint was digital access. In 2026, the constraint is compute.

That is where the capital is going.

Maybe the real bubble is not where most people are looking.

A lot of people are skeptical of the AI cycle because capex is high, valuations are stretched, and expectations are aggressive. That skepticism is fair. But at least in AI, the capital is being deployed into data centers, chips, power infrastructure, enterprise adoption, and productivity gains that are still being tested in the real economy.

Crypto is different. When one of the largest corporate Bitcoin holders needs a “Digital Credit Capital Framework” to enhance liquidity while also disclosing that it may sell up to $1.25 billion in Bitcoin, the question becomes whether the market is underpricing balance sheet complexity. The narrative is still long-term Bitcoin exposure, but the structure increasingly depends on credit, liquidity management, preferred instruments, and market confidence.

Maybe the bubble is not simply “AI is overhyped.” Maybe the bigger risk is in assets where the bull case depends less on cash flow and more on financial engineering, reflexive liquidity, and everyone continuing to believe the treasury narrative.

For me, still long bitcoin:native, but short $MSTR and $STRC

Strategy announces a Digital Credit Capital Framework designed to strengthen Digital Credit, enhance liquidity, preserve long-term Bitcoin exposure, and support long-term value creation. $MSTR $STRC https://t.co/AUoUCtem53

Strategy announces a Digital Credit Capital Framework designed to strengthen Digital Credit, enhance liquidity, preserve long-term Bitcoin exposure, and support long-term value creation. $MSTR $STRC

https://t.co/P770rd7fva

Apollo on AI and the next phase of the software cycle.

The most important point here is not that AI will kill software. I think the better framing is that AI is changing the economics of building software.

Before AI, the cycle from idea to product was expensive, slow, and highly structured. A product manager or product owner had to talk to customers, define requirements, map the business process, translate that into user stories, coordinate with design, think through the architecture, then work with engineering to build the first version. After that, the team would go back to the customer, collect feedback, improve the product, fix edge cases, and keep iterating until the product actually solved the problem.

That cycle created a lot of value for software companies because execution was scarce. Not every enterprise customer had the internal resources to turn an idea into a usable application. The supplier had pricing power because the customer needed external software vendors, consultants, or SaaS platforms to bridge the gap between business needs and technical execution.

AI compresses that cycle.

With AI coding tools, the distance from idea to prototype becomes much shorter. A customer can describe the workflow, write a detailed prompt, generate an internal prototype, test the logic, and only then hand it to an engineering team for refinement. This does not remove the need for engineers, architecture, security, compliance, or production-grade systems. But it does reduce the scarcity premium around building the first version of an application.

That matters because a lot of enterprise software value historically came from turning business processes into software. If that process becomes cheaper, faster, and more accessible, the margin structure of software starts to change. The supply of basic software creation increases massively, and when supply becomes abundant, pricing power naturally comes under pressure.

This is similar to any commodity-like supply chain. When the supplier controls a scarce input, the supplier captures high margins. But when that input becomes easier to produce, buyers gain leverage. In software, AI is making certain types of application development feel less scarce. That is not bearish for all software, but it is clearly bearish for undifferentiated software.

The chart on public software revenue growth is important in this context. Average LTM revenue growth has declined sharply from the 2020–2021 software boom period. I do not think this necessarily means “the end of software.” A better interpretation is that software valuations are moving back toward a more realistic equilibrium after years of pricing in unusually high growth, high margins, and strong recurring revenue certainty.

The market is not saying software has no value. It is saying the old valuation framework no longer applies equally to every software company. In the previous cycle, many software names benefited from the same broad multiple expansion because the market treated recurring revenue, high gross margins, and digital transformation as enough to justify premium valuations. In the AI era, that will become harder. Investors will likely separate software companies that are truly mission-critical from those that are merely convenient.

The winners will likely be companies with deep workflow integration, proprietary data, strong distribution, high switching costs, and products that are embedded directly into how enterprises operate. These companies can still defend pricing power because they are not just selling “software.” They are selling reliability, compliance, data advantage, institutional workflow, and reduced operational risk. That kind of software is much harder to replace with an AI-generated internal tool.

Last, the losers will likely be generic point solutions where AI can replicate enough of the product experience at a much lower cost. If a customer can build a usable internal prototype, automate the workflow, and customize it for their own needs, the willingness to pay for external software naturally declines. So the next phase of software is not collapse. It is dispersion.

Software is becoming easier to build, but durable software is still hard to defend.

That difference will matter a lot more in the AI era.

the rotation out of gold and Bitcoin into semiconductor stocks says a lot about where market conviction is right now.

I still wonder whether there is any meaningful net inflow left into Bitcoin exposure, whether through $IBIT, other Bitcoin ETFs, or even spot BTC, after the 10/10 crash. in my view, that event did real damage to investor trust in crypto. not just short-term sentiment, but the broader willingness to treat Bitcoin as a reliable risk asset during this cycle.

when trust breaks, capital does not just sit still. it looks for the next high-conviction narrative and right now, that narrative is clearly AI.

the AI cycle started with Nvidia and the GPU trade, but it has now expanded into a much broader infrastructure theme. first hyperscalers, then semiconductors, memory, foundry capacity, wafer supply, networking, power, energy and the rest of the AI supply chain. the market is no longer only buying AI as a software story, it is buying the entire physical stack needed to scale intelligence.

that is why the rotation makes sense. Gold and Bitcoin were previously viewed as stores of value or macro hedge trades, but semiconductors are being treated as direct beneficiaries of one of the biggest capex cycles in modern markets. when investors see real revenue, real demand, and real earnings leverage in the AI supply chain, it becomes harder for passive “digital gold” narratives to compete.

for Bitcoin, the problem is not only price action. the bigger issue is confidence. if crypto is losing trust at the same time AI-related equities are producing stronger momentum and a clearer fundamental story, then capital naturally rotates away from BTC and into semis, because liquidity follows conviction.

this is also why I do not see a near-term Bitcoin bull run as long as the AI cycle remains the dominant trade. Bitcoin can still bounce, but a real bull market requires renewed trust, fresh inflows, and a stronger reason for capital to return. right now, semiconductors offer the cleaner story: AI demand, earnings growth, infrastructure scarcity, and institutional momentum.

for now, the market is making its preference clear:

less digital gold. more silicon.

Retail investors appear to be rotating out of gold and Bitcoin into semiconductor stocks:

Since April, US gold and Bitcoin ETFs have posted -$12 billion in cumulative outflows.

Over the same period, US semiconductor ETFs have attracted +$20 billion in cumulative inflows.

This trend accelerated in mid-May, with outflows from gold and Bitcoin funds more than tripling.

At the same time, inflows into semiconductor ETFs have doubled.

Meanwhile, the largest US gold-backed ETF, $GLD, is down -13% since the start of April, while the largest Bitcoin ETF, $IBIT, is down -12%.

Over the same period, the semiconductor ETFs, $SOXX and $SMH, are up +81% and +60%, respectively.

Retail is driving markets like never before.

bitcoin:native bottoms rarely happen in a single move.

They tend to unfold in three phases.

Phase 1: Breakdown.

Momentum turns sharply negative as selling pressure accelerates.

Phase 2: Base Formation.

Price stabilizes, but Momentum remains weak while Bitcoin Impulse turns neutral. Selling pressure is still being absorbed.

Phase 3: Recovery.

Bitcoin Impulse turns positive first, followed by a recovery in Price Momentum. Only then does a sustainable uptrend begin to emerge.

Where are we today?

Bitcoin has likely moved beyond the initial breakdown. But we're still in the base formation phase.

Price is stabilizing, yet Momentum remains deeply negative and Bitcoin Impulse has only just returned to neutral.

But this transition takes time.

The first signal will be whether Price Momentum can escape its extreme negative state.