Nebius has announced an investment of £1.7 billion to build out capacity in the UK with three new deployments of NVIDIA infrastructure.

The three new sites will deploy the latest generations of NVIDIA’s full-stack, end-to-end AI factory platform technology and combined will reach 65 MW when fully ramped up in 2027.

In addition to the capacity investment, Nebius is expanding its commercial and AI R&D hub in London and establishing local partnerships with universities and research institutions through Nebius Academy.

Arkady Volozh, founder and CEO of Nebius, said:

"The UK is one of the places where AI is being built, deployed, and adopted at the same time — by startups, by enterprises, and by the public sector. The work is happening here and the demand is here. And we are also here for the long run."

Read the full press release: https://t.co/sihQhjU8Ow

Congratulations to @AnthropicAI on raising $65bn.

When Claude 3.5 launched, their engineers asked Claude which database to use. Claude recommended ClickHouse.

Fast forward a year and we launched ClickHouse Agents. powered by Claude. Here's to building together.

https://t.co/nuosoc1JsZ

REPEAT after me:

I don’t sell $RKLB and $RDW for SpaceX

I don’t sell $RKLB and $RDW for SpaceX

I don’t sell $RKLB and $RDW for SpaceX

I don’t sell $RKLB and $RDW for SpaceX

I don’t sell $RKLB and $RDW for SpaceX

Rocket Lab has been awarded a $90 million contract by the @USSpaceForce’s Space Systems Command @USSF_SSC to design, manufacture, integrate, and operate two geostationary satellites hosting the Heimdall space domain awareness payload produced by Rocket Lab Optical Systems.

Rocket Lab components have long played an essential role in many GEO programs, but this is our first satellite production program for geostationary orbit. The two satellites will be built on our Lightning bus, adapted for the thermal, radiation, propulsion, and station-keeping demands of GEO.

Is the $BE deal bad for $NBIS?

No.

But to paint a fair picture:

The partnership is basically a lease commitment that'll sit on their B/S which in theory constrains their incramental credit capacity for more GPUs.

That's a very bearish stance though, but just saying to paint a fair picture. Imo the main issue isn't in Nebius' potential margin compression.

But really, Nebius are a bet that they can deploy those GPUs at scale. If they can't due to lack of power, then the whole thesis collapses.

Really, their only options were:

1. lose allocation and exit the FY27 cycle

2. build their own gas turbines at worse economics w/ expertise they don't have

3. co-locate w/ utility partners with similar premium pricing + worse control

So Bloom are essentially the best option from a tiny menu.

Then the real thing to monitor for Nebius is if they can price their compute to recover the premiums their paying for power.

I believe they can + will.

Redwire has been selected for a new high eight-figure, multi-year contract by a NATO ally to deliver its next-generation Penguin Mk3 tactical UAS platform. Our Mk3 platform was shaped around operational feedback loops emphasizing modularity, rapid adaptability, sustainment, and scalable deployment.

The contract reflects how NATO allies are increasingly prioritizing combat-proven autonomous systems that can evolve quickly in response to electronic warfare and changing battlefield conditions.

Read here for more: https://t.co/yHcBEaFG5T

Liftoff from Space Launch Complex 40 (SLC-40) at Cape Canaveral Space Force Station in Florida!

Third time’s the charm for @SpaceX CRS 34, and tonight’s launch carries something extraordinary. 🚀

Aspera Biomedicines is sending its second investigation with Redwire's PIL-BOX to the @Space_Station to advance development of rebecsinib, a small molecule ADAR1 inhibitor recently approved by the U.S. Food and Drug Administration to begin first-in-human trials.

By studying their “kill‑switch” cell therapy in microgravity, researchers can observe cellular behavior in ways that are impossible on Earth.

Learn more here: ⬇️

Not sure if people realized this but unless a thesis completely breaks, companies like $NBIS can keep growing.

Just look at $AMZN or $GOOGL over the past 15 years.

If people "trim" it often triggers taxes. And a lot of corrections are typically less than those taxes paid.

By the time a "50% crash happens", it's probably already compounded hundreds of even thousands of percent.

If people need to pay expenses, once you hit 7-8-9 figures, you can always borrow against those assets and keep letting them appreciate.

NFA, just personal opinion. You all do you, but it's highly, highly, dependent on the companies you pick.

Can't do this with something trash like $IREN. But I do believe $NBIS is positioned to be the next hyperscaler.

The humanoid robotics theme is an emerging trade I see right now and almost nobody is positioned for it correctly IMO. 🤖📈

Pay attention... most people only really know $TSLA.

Optimus is real and Tesla is the demand creator that legitimizes the entire sector, but the second order trade is interesting too.

Here's the chain... simplified drastically...

Every humanoid robot needs eyes. Lidar and vision is the layer that lets a robot actually understand the world it is walking through. $OUST is the cleanest public lidar pure play, $MBLY is the vision and ADAS leader pivoting hard into robotics, $AMBA is the edge AI vision chip that processes everything in real time, and $AEVA, $ARBE, $CGNX round out the perception layer.

Every humanoid needs precision motion. Harmonic drives, actuators, and motion control are the unsexy compounders most retail will skip right over. $VPG is the precision sensor and load cell pure play, $NOVT is motion control built specifically for robotics, $ALNT is precision motion components, and $RR is the optical sensor name that quietly shows up everywhere.

Every humanoid needs a brain. The compute that runs on board has to be cheap, low power, and reliable. $LSCC is the low power FPGA that ends up inside countless edge devices, $INDI is the automotive and robotics semi nobody has on their radar yet, $AMBQ is the analog compute play, and $MRAM is the next gen memory built for exactly these workloads.

Every humanoid needs a logistics use case. The first commercial deployments are not going to be in homes, they are going to be in warehouses. $SYM is the automated warehouse pure play, $ZBRA owns enterprise scanning and tracking, $SERV is sidewalk delivery robotics that doubles as data collection, and $KITT is the autonomous platform play.

Every humanoid needs an industrial pedigree. The companies that already build robots for factories will be the ones supplying components and software to the humanoid OEMs. $ISRG is the surgical robotics gold standard, $KLIC is the precision assembly tooling, $HG is the heavy machinery name pivoting into robotics, and $BOT is the basket ETF if you want broad exposure in one click.

And on the speculative high beta end... $ATOM is robotic software with real adoption, $XPEV has its own humanoid program coming, $AUR is autonomous trucking which is the same playbook applied to the road, and $NEO is the small cap optionality play.

Pick the chokepoints.

Own the picks and shovels... then wait.

Will share more ideas to followers soon. NFA.

Quick take: $NBIS vs $IREN (post earnings)

Power was the original bull case for IREN.

Nebius just crushed it with 3.5 GW contracted (already beating their 3 GW target) and is guiding 4 GW by end-2026, all financed WITHOUT brutal dilution.

Execution through revenue growth & cash in hand - clearly a huge difference.

What separates them is the full-stack AI cloud: not just raw power + GPUs, but deep engineering, expanding margins, and a real software moat.

Power will commoditize - execution and full vertical integration will decide the winner.

Nebius is building like the next hyperscaler. IREN is just chasing the next big thing.

Facts in front of you.

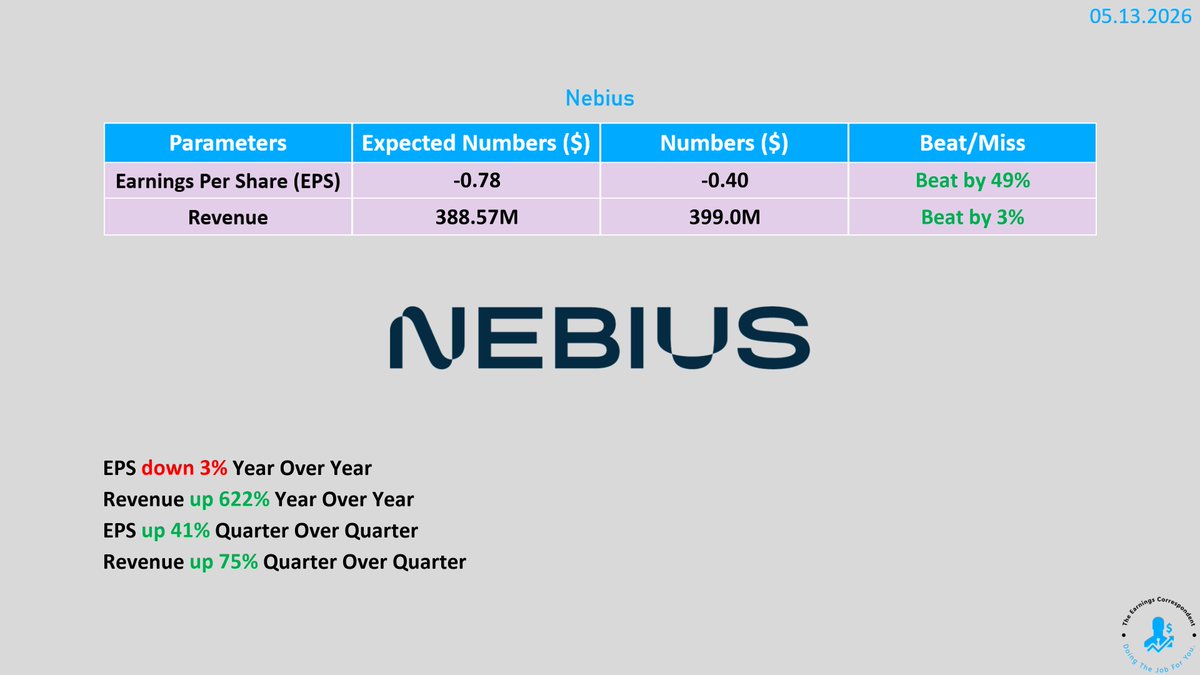

$NBIS ABSOLUTELY CRUSHED EARNINGS 🔥

EPS: $(0.33) vs $(0.77) est

REV: $399.00M vs $371.40M est

Adjusted EBITDA: $129M vs $(53.7M) prev year

Net Income: $621M vs $(104.3M) prev year

Raised Contracted Power Guidance to over 4GW by year end

Expects to significantly increase capacity in place in Q3

🟩 +12.44%

$NBIS Q1’26 EARNINGS HIGHLIGHTS

🔹 Revenue: $399.0M (Est $388.57M) 🟢; +684% YoY

🔹 EPS: $2.11 (Est $(0.78)) 🟢

🔹 Adjusted EBITDA: $129.5M

🔹 Net Income From Continuing Operations: $621.2M

🔹 Adjusted Net Loss: $(100.3)M

Other Metrics:

🔹 Operating Cash Flow: $2.26B

🔹 Purchases Of PP&E & Intangibles: $2.47B

🔹 Cost Of Revenue: $103.8M, 26% of revenue

🔹 Depreciation & Amortization: $212.0M

🔹 Shares Outstanding: 253.9M

Business Highlights:

🔹 Pennsylvania AI Factory: Secured up to 1.2 GW of power and land

🔹 Core Business: AI cloud

🔹 Consolidated Businesses: Nebius, Avride, TripleTen

Commentary:

🔸 “Nebius today also announced that it has secured up to 1.2 GW of power and land for a new, owned AI factory at a site in Pennsylvania.”

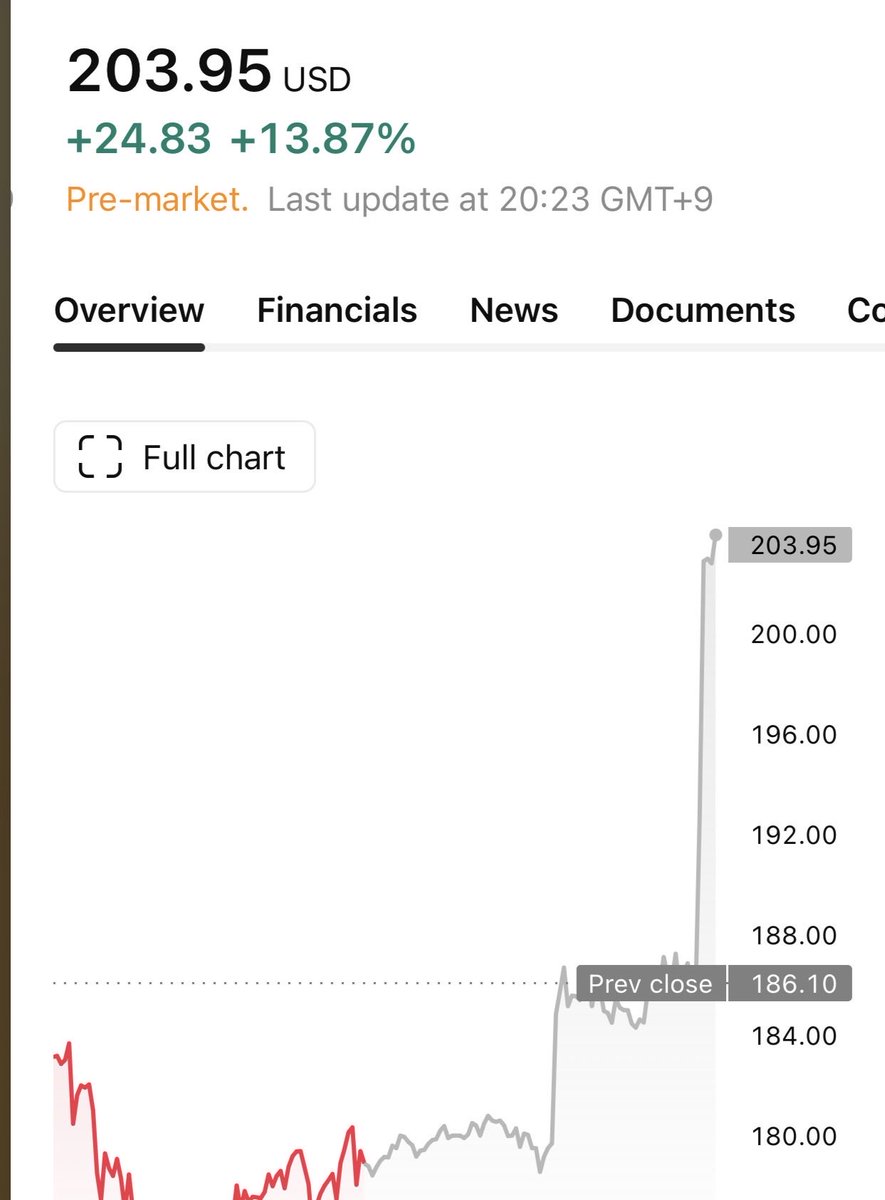

$NBIS earnings were stellar and it’s now trading $200+ premarket.

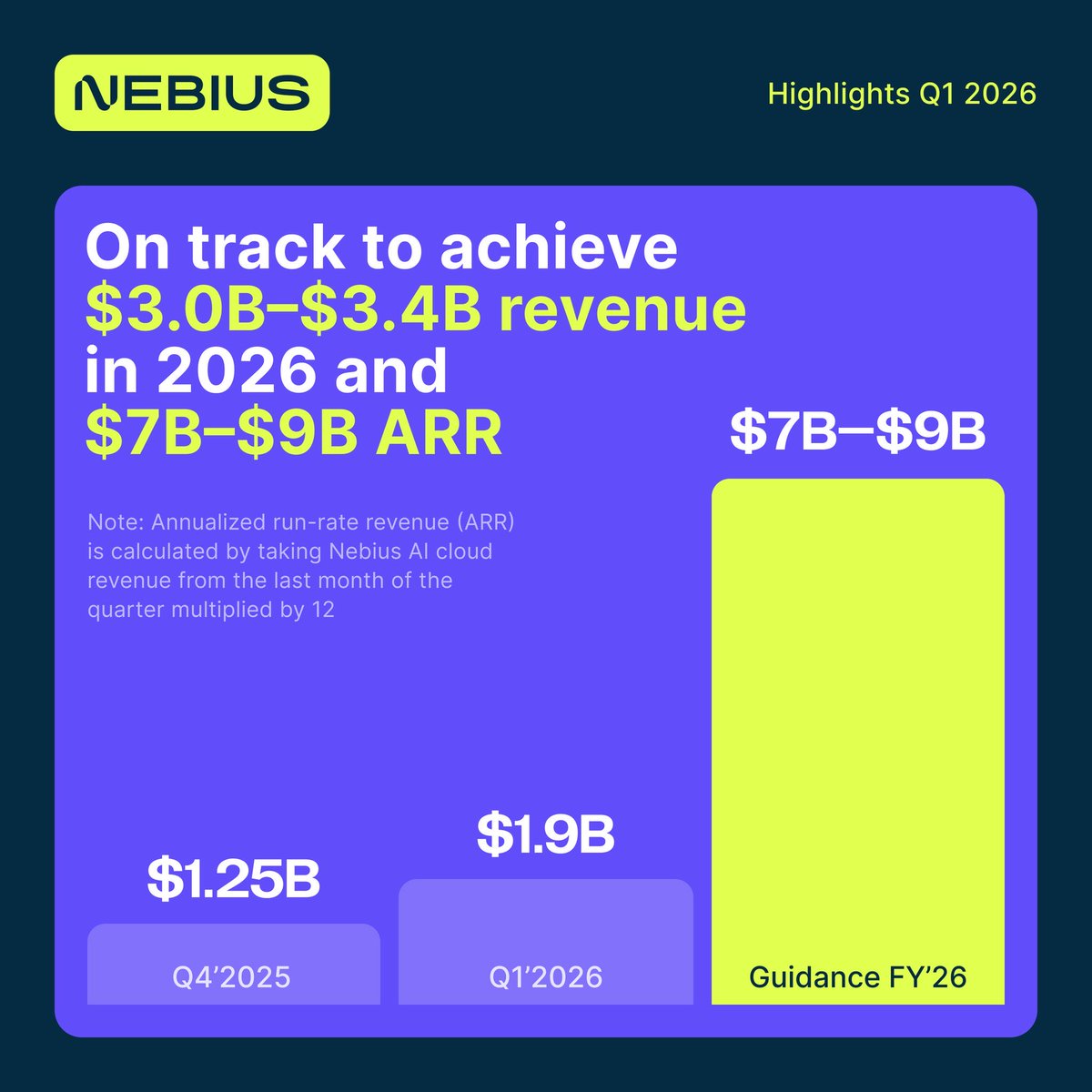

Reiterated $7-9B ARR in 2026. 40% adj. EBITDA margin projections, which is vastly outperforming expectations.

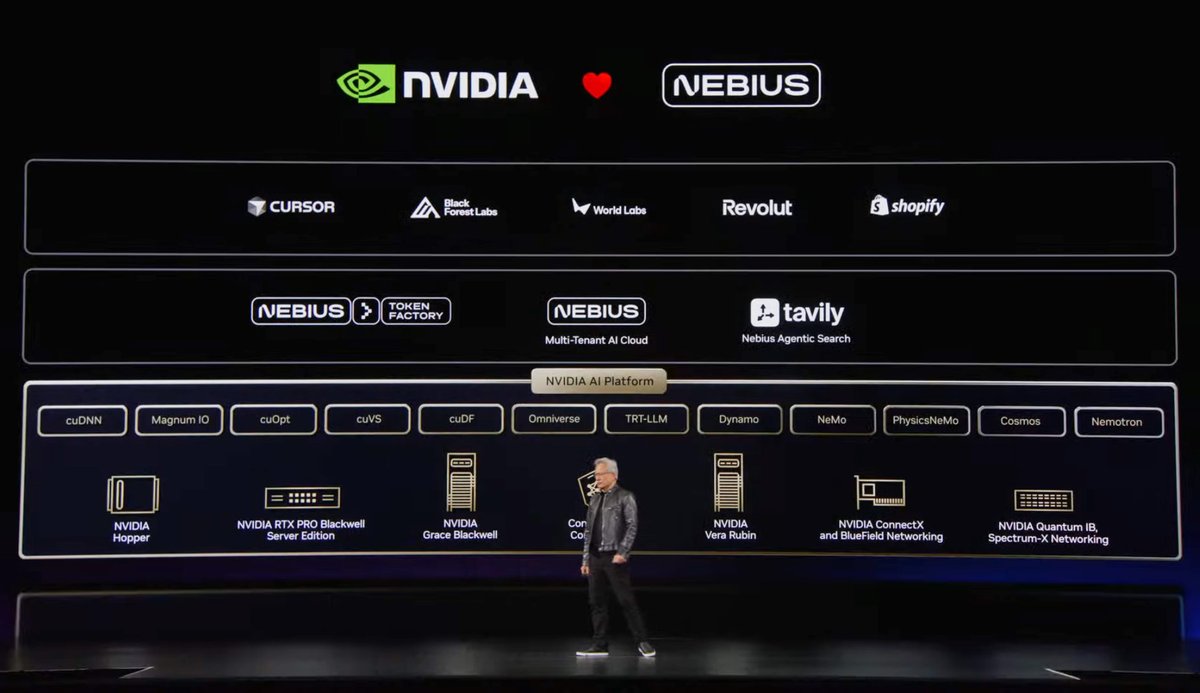

4 GW contracted capacity. $6.3B capital secured by $NVDA off solid financial offering structures.

Glad my high conviction Neocloud pick is performing wonders and happy management is executing so well.

In the words of Jensen: “Nebius will take care of you”