Topo Mayor México: “llegó una muchacha de una TV local y me dijo que tenía que decir esto y agradecer a tu presidenta”

“mira mija te voy a decir una cosa tengo 80 años y no me vas a venir a decir que decir, no eres jefa, yo no soy político, soy rescatista” “la mandé al diablo”

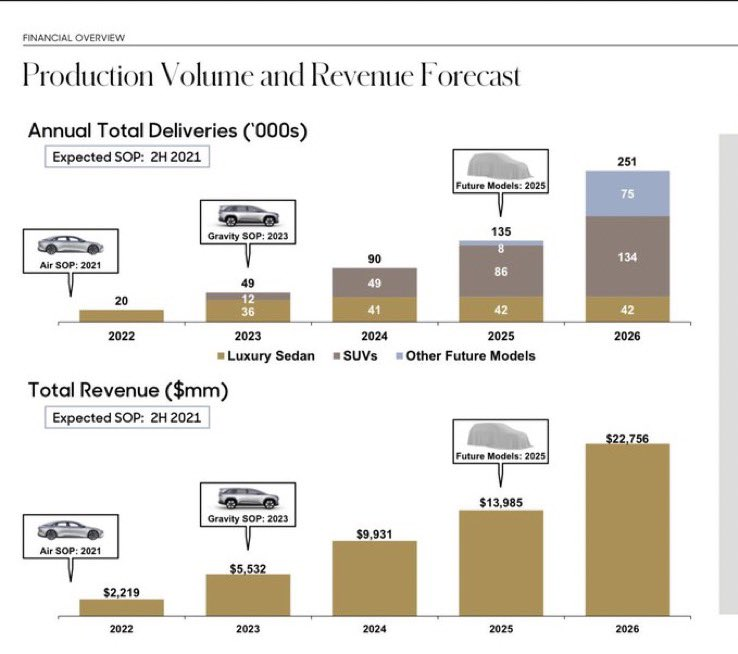

I love looking back at SPAC presentations

Lucid's $LCID forecasted in its 2021 SPAC presentation they'd deliver 90,000 vehicles in 2024

Through the first 9 months of 2024 Lucid delivered 7,142 vehicles

Hoy tuve la oportunidad única de conocer en persona a Jamie Dimon, CEO y Chairman de JPMorgan Chase, uno de los líderes empresariales más importantes del mundo y una persona que admiro profundamente.

Un sueño hecho realidad, a esto vinimos a Georgetown.

My thoughts on software.

The punchline is I think platform SaaS is very interesting here - great businesses, great earnings potential, likely AI beneficiaries, attractive valuations, stocks that have moved sideways for years despite improved fundamentals. The other 80-90% of software names strike me as uninteresting / too difficult.

General view putting AI to the side for now:

1) Market penetration of software is relatively high. COVID forced everyone to digitize overnight. There simply are not large segments remaining to be digitized. Even the largest productivity laggards, government entities, are largely digital.

2) Most end-markets in software are now competitive and have multiple viable vendors. This includes all aspects of software for employees: marketing, sales, customer support, productivity / collaboration, communication, HR / payroll, etc. It also includes all aspects of software for engineers / operations: coding platforms / repositories, security (endpoint / servers / network), databases, monitoring, etc.

It was most certainly not this way 10 years ago, nor even 5 years ago. But today, nearly everyone has competition in nearly all of their product lines.

3) Most new products from existing and new players are evolutionary, not revolutionary.

Wow, you include SMS along with email as part of your marketing platform? Yawn. Your UI is slightly cleaner than the next player? C'mon.

4) The industry has too many engineers creating and sales people selling duplicative products.

Generous compensation packages for new employees made sense up through the demand tsunami created by COVID, and was corroborated by healthy sales productivity.

But this period is over and management teams need to recognize that growth is unlikely to re-accelerate from improved sales productivity and budget accordingly.

I think most sw companies could reduce their headcount by 20-25% and not skip a beat. Most could probably do 30-35% and only lose low ROIC growth.

5) Stock-comp remains out of control.

I get it. It was fun while employees could get amazing pay packages, and shareholders got paid as well since the market just ignored SBC. Win win.

But that's over. Why should investors spent time on software businesses that are unprofitable on a GAAP basis that grow <30% (headed to <25%, headed to <20%) when you can own other fantastic tech businesses that grow at similar rates, have real GAAP margins and stocks that trade on real GAAP profits (semis, mega-cap, etc.)?

Now for the positives:

1) There is a lot of clean-up potential over the next 10 years. Growth is not over but it is mature and investment needs to slow down. There is no urgency to expand rapidly into a neighboring TAM which has a strong incumbent. Rather, rightsize the existing employee base and pursue consolidation where appropriate.

2) I think the protected and interesting businesses are the platforms which sell multiple, strategic products that hook customers and serve as distribution channels for incremental products. These platforms can be horizontal ($CRM, $HUBS, $WDAY, $NOW, ...) or vertical ($ADSK, $ADBE, $VEEV, $PCOR, ...).

3) Valuations for some of these stocks are very reasonable on FCF and all of these companies are under-earning which means multiples could be even lower after a "get-fit" period. Stock comp dampens this argument although stock comp also can be decreased meaningfully over time. CRM has only 10% downside to 16x CY25 street FCF, WDAY has only 11% downside to 21x CY25 street FCF, VEEV has only 5% downside to 20x CY25 street FCF.

And finally some thoughts on AI's impact to software:

1) I don't buy that "AI makes coding easy" will result in everyone building their own software and obviating the need for packaged SaaS. That doesn't pass the smell test. The whole point of buying versus building is it is better, faster and cheaper; and I think that value proposition persists. Especially because it is very tough to get AI to actually work. Will tech-forward companies like Klarna build their own? Sure, but I think that will be how the minority of companies approach it. Furthermore, companies should focus internal development on company-specific AI -> Pfizer should work on AI for drug discovery / testing (on $MSFT, $AMZN, $GOOGL) but just use $VEEV / $CRM AI for their sales people.

2) At least for now, it seems to me we are only seeing AI be a feature, not a product. So, for now, the incumbents are best positioned to layer in AI features and race to get to product stage over time.

3) SaaS companies ought to be able to create value via incorporating AI and that ought to be monetizable - maybe not linearly but over time the revenue will benefit from the value prop (may have to transition from seats to transactions, whatever).

4) SaaS companies only costs are people and AI is, in theory, really good at helping with productivity. So, SaaS companies ought to see engineers code more efficiently, marketers advertise / conduct webinars / write copy more efficiently, sales people put together pitch decks / draft emails / write contracts more efficiently, and customer support handle issues rapidly. All of this can also help in industry rationalization as investment slows while productivity growth continues.

And a couple random thoughts:

1) Everyone is goo goo gaa gaa over AI right now. Like I said, we still only have features (writing assistant, summarization, translation, etc.) from all the effort. If the investment in semis slow down and/or we go through a digestion period, the fundamental story for SaaS platforms will strengthen and the stocks ought to benefit.

2) No one is worried about macro right now, but the stock market is like Florida - macro hurricanes come by pretty frequently. In the next storm, at least from these price levels, I would bet SaaS will outperform given the relatively high predictability of their recurring revenue models.

@Dave_51 Saludos, David. De casualidad tienes en tus registros quién fue el #29 del Caracas en la 05/06? No logro saber a quién le perteneció esta camiseta. Gracias!

@Dave_51 No se si ya la habías visto, pero mira esta belleza que relanzó la Forte hace poco. Creo que las venden en la tienda en La Calendaria. Tengo pendiente ir pronto.