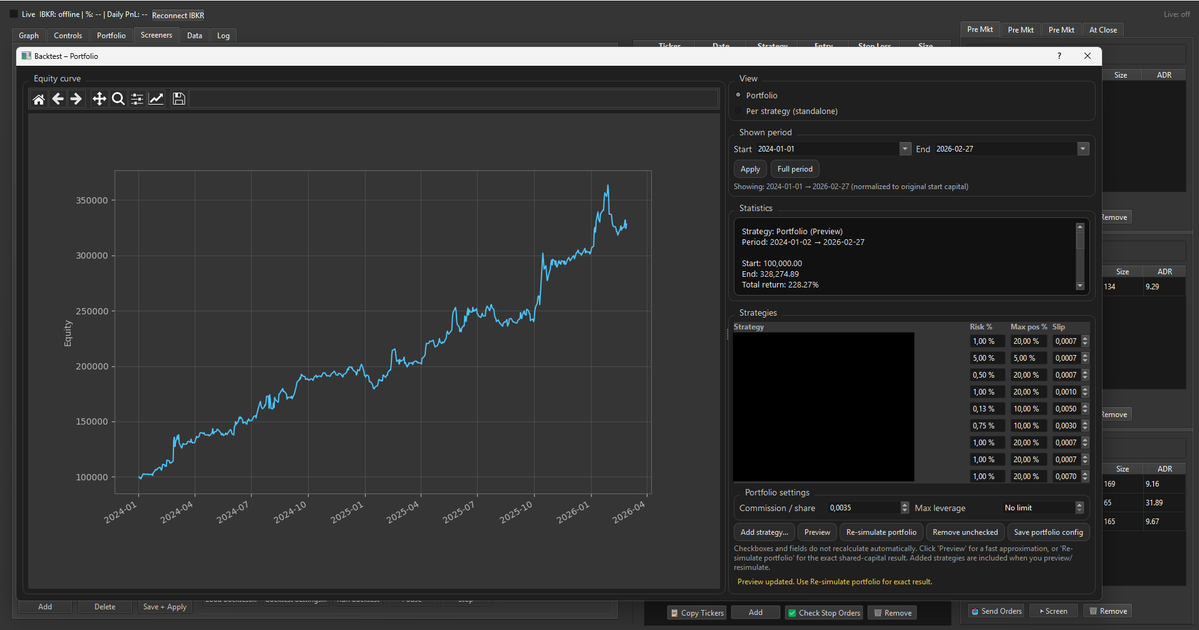

Finally done with the backtest part of my platform. Really happy with how it turned out! Easy to add a strategy and see how it changes the portfolio dynamic with different risk settings etc.

This is 100% correct!

There is a total of 985 stocks trading over 100 mil on a 20 day average currently. So there are plenty of stocks to trade with a big account.

Effectively every single stock in the semiconductor, software, aerospace & Defense, neocloud, memory, photonics, cyber security and industrial metals group that has made a meaningful move trades north of 100mil over a 20day average. And that includes the $MRAM $POST $MXLs of the world.

If we list the 100 biggest winners over the last 12 months I’d venture to say 90% of them trade north of 100 million per day.

But I’ll let you fact check it on your own. Because I already know the answer to that question. And then you’ll quickly realize I wasn’t talking out of my ass at all. My original comment was a fair criticism. If you are trading north of a 10million portfolio, which I would assume you are, then 100mil daily dollar volume is effectively required or slippage is a real issue.

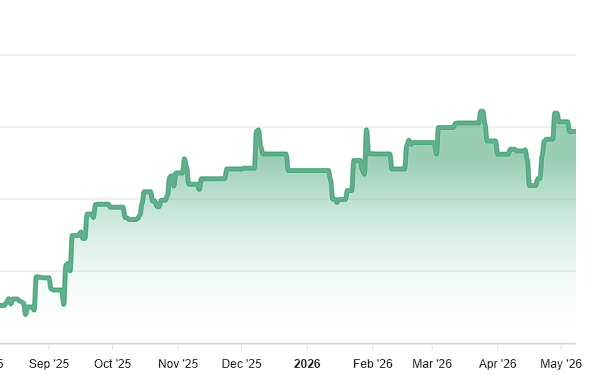

Not overwhelming returns considering the frothiness in the market which most of my systems are designed to capture. But I'm not complaining.

Trying out some new strategies on the daily timeframe:

- taking the other side of a parabolic short setup

- incorperating NAAIM numbers as a regim filter to block trades as @hackertrader do

- delayed EP setup as @PradeepBonde uses

Maybe I can add some of this in the coming weeks.

Tested my portfolio during the tech bubble to see how it performed during that time. My worries were that there could be a huge drawdown during 2000-2001 were all strategies correlated for the worst. The backtest showed more or less the exact performance as now so I'm not going to worry about it.

This is very true for me as well. Have forced myself to implement rules for myself, e.g. after this new function I'm not allowed to add anything new for one week etc.

Here is one bad thing about AI coding

It just never stops. Let me explain. When coding manual in the old days you could feel when you are feeling worn out, tired, lack of ideas and productivity. You stop. Take a break. Recharge.

With vibe coding that is all gone. You have access to a knowledge and productivity that just keeps on going. But it also keeps you locked in all the time. It just doesn't end. It's addicting. Maybe even as much as social media itself.

Building yes. Creating yes. But I can see how it affects my sleep, my desire to go outside and meet people. I love vibe coding. I don't think I have ever loving building things since I have started working with Claude and Codex.

But it's taking a toll. Something I need to learn to dose better. Keep a better balance.

Just my thoughts 🙏🏻

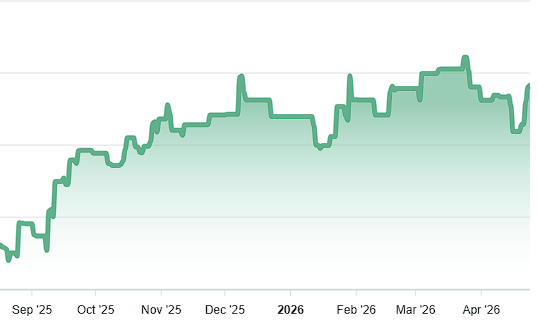

Not verry happy with the performance the recent weeks. Was expecting more in this kind of environment. Have made some adjustments and maybe I do some more the coming week.

@Dan_Trend@simo_vanov@JoachimMo1985 Ok thats good to know - thanks! Yes Python is a great tool for that for sure. Maybe I can combine my platform with Realtest.

@tedbjorling I haven't really deep dived into this yet but spontaneously I think that I need to divide my system to enter the momentum leaders into one fast and one slower system. This would probably mitigate this type of problem.

My main strategies objectives are to capture the moves in the leading momentum stocks but this move I have missed nearly all of those moves. Also my MR short strategies have really had a negative impact on overall performance.

Will try to learn as much as possible from this!