🚨The Senate Banking Committee has advanced the Clarity Act on a 15-9 vote. Sens. Ruben Gallego (D-Ariz.) and Angela Alsobrooks (D-Md.) joined Republicans in advancing the landmark crypto legislation.

Today, we released a staff study of deposit flows at three banks that failed in 2023. #FDICResearch used detailed data to analyze depositor behavior in the weeks surrounding the failures of Silicon Valley Bank, Signature Bank, and First Republic Bank.

https://t.co/4HR4hHkACb

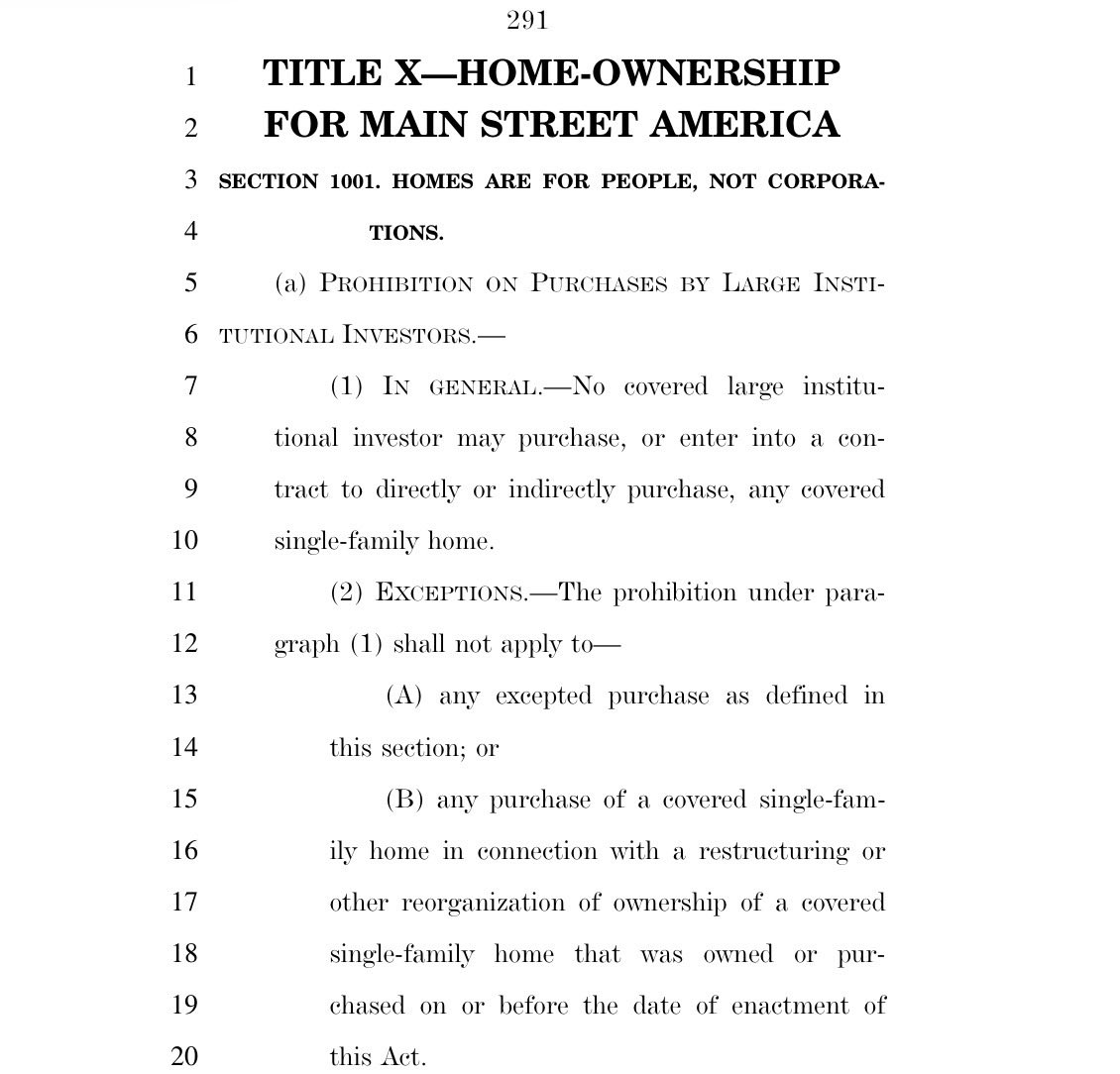

News: House Republican leadership has posted the text of their bipartisan amendment to the Senate’s 21st Century ROAD to Housing Act

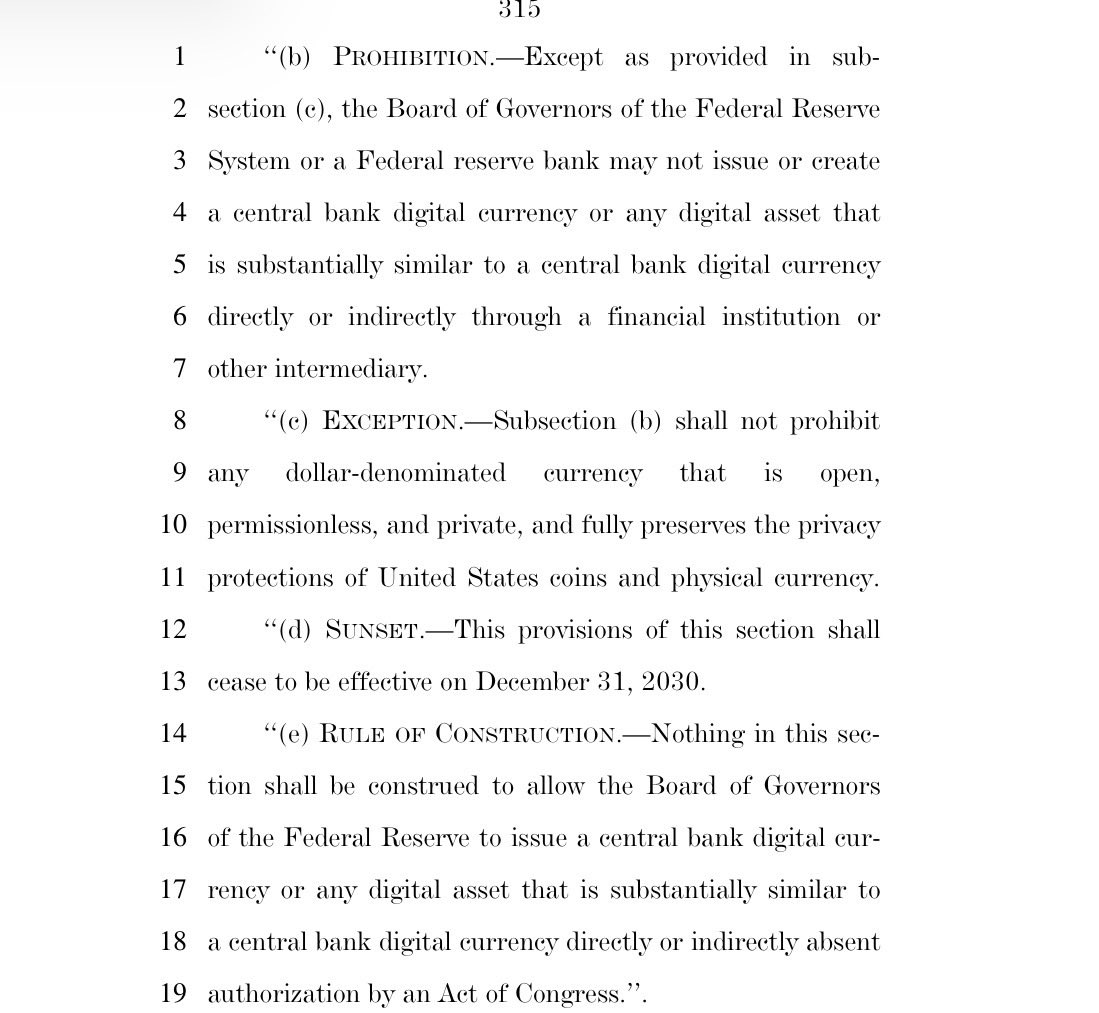

Here’s some of the reworked institutional investor prohibition language, CBDC prohibition and community bank reforms

Late Thursday afternoon (May 7), an 18-year-old male was found shot in the alley behind the Tenleytown CVS on the 4500 block of Wisconsin Avenue.

The victim was taken to a hospital. Details are still coming in.

#Tenleytown#TenleytownDC

Here are finance jobs broken out from the monthly payrolls report. They're at the lowest level since September 2022 and have contracted for three out of four months reported this year.

Hugely consequential decision allowing Morgan Stanley to transfer $85 billion of broker-dealer assets to its insured bank. Precedent setting and reminiscent of similar moves in 2007-08.

This is the first time I can recall the Fed ever approving a regulatory action by 4-3 vote.

New: Wall Street and community banks told the Trump administration that investigating millions of existing customers for immigration status wasn't practical. The White House is watering down its plans. https://t.co/SXqW1Lz3L9

@moultano I felt my blood pressure rising midway through these paragraphs and had to stop. I can't handle this right now. It will just make me too upset to finish the paragraph.

Bloom was very contemptuous of popular culture so doubt that he would ever have glanced at Twitter.

I'd always thought that Norman Mailer would have been terrific on Twitter, however. he loved adversarial situations & was very verbal, quick. he'd have loved some respite from those long, dense novels into which he poured his life's blood & which generally are not read today by younger writers.

I have said before and I will say again: The filibuster is one of the few things holding the country together. Making a trifecta truly winner-take-all in a highly polarized, increasingly unstable transcontinental empire would be an unmitigated disaster for the country.

🚨SCOOP: The White House is considering pulling its support for the crypto market structure bill entirely if @coinbase does not come back to the table with a yield agreement that satisfies the banks and gets everyone to a deal, a source close to the Trump administration tells me.

The White House is said to be furious with Coinbase’s “unilateral” action on Wednesday, which it apparently was not notified of in advance, calling it a “rug pull” against the White House and the rest of the industry. The White House does not believe that one company speaks for the entire industry, the source continued.

“This is President Trump’s bill at the end of the day, not Brian Armstrong’s,” the source said.

This is my attempt to break down the interest groups involved in crypto market structure legislation, and why getting a bill is so difficult.

TL;DR: Community/regional banks and Coinbase are locked in a zero-some competition. If one wins, the other loses.

🚨NEW: Senate Banking staff just had a call with crypto leaders, I've heard--and relayed that TradFi's demands to alter stablecoin yield rules are gaining traction in bipartisan negotiations on market structure bill.

Sen Alsobrooks' proposal to restrict yield to transactions, not deposits, is viable. There are also other options on the table that could involve restricting yield to 'regulated financial institutions'. Getting more clarity there.

As a sign of current vibes, if it wasn't already evident: Senate staff told crypto leaders they "need prayers" to get this bill over the finish line by Jan 15th markup, one source with direct knowledge told me. Hoo boy

We have made it all but impossible for young families to join the middle class in America. Let alone to save money and build wealth.

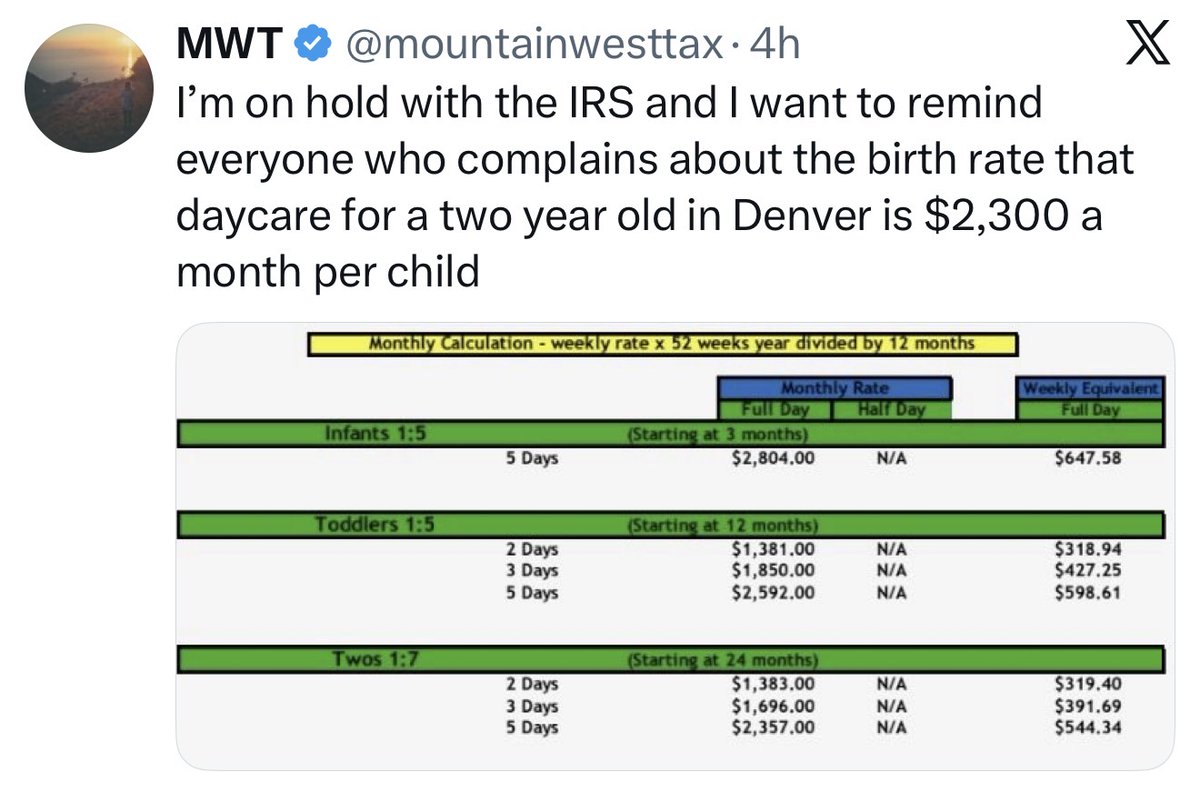

$2300 per month for daycare. $1800 for the mortgage on a starter house, plus another $700 for property tax and insurance. $1000 for a car payment, insurance, and gas. $1000 to $1500 for groceries, $2000 for bare bones health insurance. $500 for utilities and a cell phone.

Add it all up, you’re at close to $10k per month, just for basic essentials. After paying federal and state taxes, you need to gross $150k+ per year.

And that’s just for surviving. It doesn’t include saving for emergencies, retirement, medical expenses (remember, that bronze-tier insurance plan comes with a $10k family deductible!), college tuition. It certainly doesn’t leave anything for charity, home improvements, date nights, or an occasional vacation.

$150k. A number we used to think of as having “made it,” now the bare minimum to afford name-brand diapers and a car that won’t fall apart in a minor fender bender.

Is it any wonder why young people are putting off getting married and starting families? Why the political center is falling and Gen Z is racing for the political extremes, left and right alike?

Are we surprised that the rampart daycare fraud in Minnesota is so offensive to people? When taxpaying American citizens have to take home a middle-management salary just to keep their lights on?

I’m all for pulling yourself up by your bootstraps. On an individual level, it’s great advice—we all have a responsibility to live within our means, take ownership of our lives, and build the lives we dream for our families. No one else will do it for us, nor should we expect them to.

But, on a societal level, if we don’t make it affordable for people—especially young people—to lead decent lives, we’re simply not going to make it.

And I’m not sure we even deserve to do so.