Thanks @beeple, I’ve been a fan of your art for a long time. This is my new favorite.

When I decided to sell my art I wanted every piece on the blockchain and to accept Bitcoin as payment.

“The Internet of Money” by Andreas Antonopoulos really opened my eyes.

"I skipped school today. I was wondering if I could get a picture with you."

@VP: "Well, I guess you gotta have some excuse to skip school, so I might as well..." 🤣

All-time favorite type of videos: pre-fame bands playing their extremely famous songs to a tiny room of people, because they're not yet known.

A thread of some examples 🧵

1. MGMT playing 'Kids' to a crowd of maybe 25 people on a college quad

Marco Rubio on Donald Trump (2016): “I will never stop until we keep a con man from taking over the party of Reagan and the conservative movement. He’s a con man”

If you watch one thing today, make it this interview from last night in which the former head of M16 explains that Trump is a moron, that Europe must get hugely armed and fast because Russians are coming.

This is moralistic garbage, which is unfortunately the rhetorical currency of the globalists because they have nothing else to say.

For three years, President Trump and I have made two simple arguments: first, the war wouldn't have started if President Trump was in office; second, that neither Europe, nor the Biden administration, nor the Ukrainians had any pathway to victory. This was true three years ago, it was true two years ago, it was true last year, and it is true today.

And for three years, the concerns of people who were obviously right were ignored. What is Niall's actual plan for Ukraine? Another aid package? Is he aware of the reality on the ground, of the numerical advantage of the Russians, of the depleted stock of the Europeans or their even more depleted industrial base?

Instead, he quotes from a book about George HW Bush from a different historical period and a different conflict. That's another currency of these people: reliance on irrelevant history.

President Trump is dealing with reality, which means dealing with facts. And here are some facts:

Number one, while our Western European allies' security has benefitted greatly from the generosity of the United States, they pursue domestic policies (on migration and censorship) that offend the sensibilities of most Americans and defense policies that assume continued over-reliance.

Number two, Russians have a massive numerical advantage in manpower and weapons in Ukraine, and that advantage will persist regardless of further Western aid packages. Again, the aid is *currently* flowing.

Number three, the United States retains substantial leverage over both parties to the conflict.

Number four, ending the conflict requires talking to the people involved in starting it and maintaining it.

Number five, the conflict has placed--and continues to place--stress on tools of American statecraft, from military stockpiles to sanctions (and so much else). We believe the continued conflict is bad for Russia, bad for Ukraine, and bad for Europe. But most importantly, it is bad for the United States.

Given the above facts, we must pursue peace, and we must pursue it now. President Trump ran on this, he won on this, and he is right about this. It is lazy, ahistorical nonsense to attack as "appeasement" every acknowledgment that America's interest must account for the realities of the conflict.

That interest--not moralisms or historical illiteracy--will guide President Trump's policy in the weeks to come.

And thank God for that.

Marco Rubio: “For years to come, there are many people on the right...that are going to be having to explain and justify how they fell into this trap of supporting Donald Trump because this is not going to end well.”

(2016)

Analysis on $MSTR Preferred Stock Target Raise

*MicroStrategy to Target a Capital Raise of Up to $2 Billion of Preferred Stock*

link: https://t.co/MuXKBTFXOa

(Very long post, trigger warning)

First, what is a preferred stock? If you want a good primer, here's a @PrestonPysh video from 12 years ago going through the basics: https://t.co/862SIn9Ydm

So what is a 'Perpetual' preferred stock, and what might it mean for $MSTR??

TLDR: A perpetual preferred stock is a hybrid financial instrument that combines features of debt and equity, offering fixed dividend payments with no maturity date. It sits between debt and common stock on a company's capital structure, meaning preferred shareholders are paid dividends before common shareholders (no dividends for common shareholders in this case) but after debt holders.

In liquidation, they also have priority over common stockholders. While preferred shareholders usually lack voting rights, they benefit from a more stable income stream and greater security in dividend payments. This structure allows companies to raise capital without diluting voting control (!!!!!), while offering investors a balance of income and relative safety.

The most important thing to understand is that as the preferred stock is perpetual, there is no lump sum principal repayment. There will be an annual dividend, and depending on the rate it is issued at, it is equivalent to pulling forward 10-20 years of buying power.

At a 5% rate, you are essentially pulling forward 20 years of cash.

So lets dive into the profile of preferreds:

Preferred stocks are low volatility, and provide less upside than common equity typically. Banks, Utility companies, REITs, etc.

For some numbers:

Globally, there is 3,488 issues of preferred stock worth over $1m outstanding. On average, $555m per issue, worth approximately $1.93 trillion in aggregate.

More specifically, if we narrow it down to parameters that match where $MSTR likely targets, there are currently 306 securities that check the following boxes:

- Exchange listed

- Perpetual

- U.S. listed issuer

- $378m avg. value per issue

- $115.69 billion in aggregate across 306 issues

- Avg. initial dividend rate of 6.283%

So who is the target buyer for preferred stock?

- Insurance companies

- Pension funds

- Mutual funds

- Banks

Notably, preferred stock can be held as Tier 1 or Tier 2 capital on bank balance sheets under Basel III banking regulations.

Preferred stocks are low volatility, low performance, income generating securities. Shown below is the 60-day historical volatility of a preferred stock index. 10% volatility, or about 1/10th of $MSTR currently.

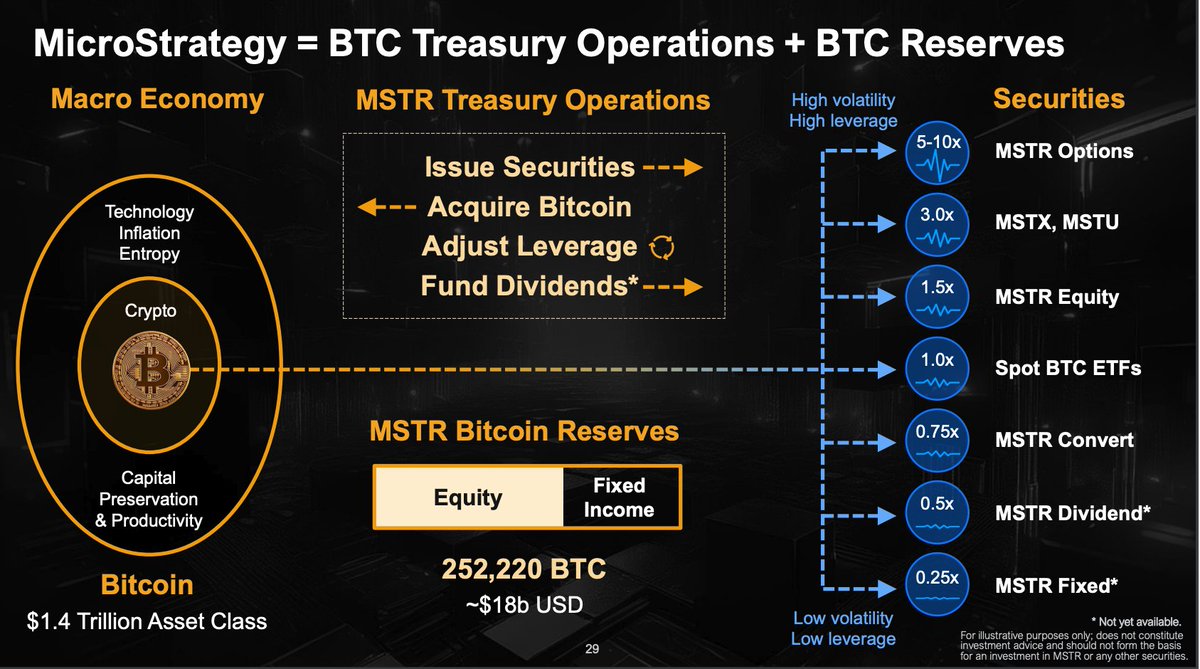

This will be the first time we are seeing what falls under the '$MSTR Dividend*' category that MicroStrategy teased on its Q3 earnings presentation.

Slide 29: https://t.co/FDkL5lIv9l

However, there is an extremely important advantage that $MSTR has compared to nearly all other preferred issuers:

Volatility. (Not to mention subsequent common stock liquidity, performance, and $BTC exposure)

"The perpetual preferred stock may include features such as (i) convertibility to our class A common stock." - MSTR Preferred Stock filing https://t.co/MuXKBTFXOa

What $MSTR can provide to fixed income investors is an indefinite $BTC backed call option

Let's do some option math:

The value of MSTR calls options with the market implied vol (87%), based on a reference price of $332 per share of $MSTR :

+50% out of the money:

- 1-year expiry: $89.56 (26.36% of price today)

- 5-year expiry: $222.13 (65.4%)

- 10-year expiry: $286.28 (84.28%)

- 20-year expiry: $326.42 (96.10%)

Now, let's do something much MUCH further out of the money, just for the sake of the example.

The value of +500% (!) out of the money calls options with the market implied vol (87%), based on a reference price of $332 per share of $MSTR :

- 1-year expiry: $20.93 (6.16% of price today)

- 5-year expiry: $140.97 (41.50%)

- 10-year expiry: $243.16 (71.59%)

- 20-year expiry: $314.73 (92.66%)

Are you starting to understand how valuable an indefinite call option on a ~90% volatility $BTC beta stock can be for fixed income investors??

The right tail 'risk" is massive for an indefinite call option on a hyper-volatile stock.

The path forward for Saylor and Co. is selling volatility, this time, to preferred stock investors. It's not debt that has to be paid down outside of the annual dividend, and even if we generously assume they pay an average preferred rate of ~6% (I would bet they fetch below average), that would only be $120m per year in dividends on a $2 billion raise, for a company that raised > $15b in equity capital alone in 2024. Non-issue.

We have no idea what the pricing will look like i.e. where $MSTR will place the strike, or what the initial dividend rate will be, so we are just sort of approximating for now.

I can't see $MSTR issuing preferred without a conversion option at some ratio to common stock. After-all, volatility is THE product, and BTC Yield is the Key Performance Indicator. The indefinite optionality is THE most interesting product that MSTR can sell to the fixed income market.

Thus, given the immense theoretical value of the imbedded indefinite call, it might make sense to apply a conversion ratio less than 1.0 for every preferred share to common.

Something like 0.50, or 0.20 conversion into common for every share of preferred for a conversion ratio (i.e 2 or 5 shares of preferred stock convert into 1 share of common stock) could make sense; but again, we can't know until its been priced and placed.

But what we do know is how much Saylor and team emphasize the value of volatility.

"Volatility is vitality."

The treasury team has spoken at length about selling volatility (only through convert issues thus far) and recycling the proceeds back into BTC.

This selling of volatility is how they take the preferred market by storm.

Using our example from above, if an $MSTR call option was striked +500% out of the money (approx $2000/share currently), with 5 shares of preferred converting to 1 share of common stock, the theoretical call option in each preferred share (with a 10-year expiry just for the sake of the math) would be $48.63 of value. For just the option, nevermind the dividend paying component of the preferred share (!!!!). Now, instead of 10 years make it indefinite...

The most interesting thing to watch for will be the provisions that the conversion contains in the preferred offering.

In the past, when $MSTR has issued convertible bonds, the bond has contained all sorts of provisions for the convertible component; a put option imbedded for the buyer of the debt, a call option that $MSTR can redeem if the bonds rise past a certain value after a period of time, etc. I posted some of that theoretical math here: https://t.co/4g9KwIN6Ds

The point of all these provisions is to essentially cap the upside and the downside of the convertible option.

The imbedded 5-6 year call option in the convertible debt is purposefully neutered, because the convert buyers aren't actually interested in the directional exposure.

These convert arb desks are in the business of 'gamma-trading', as they look to delta hedge out their exposure almost instantly. Nevermind exposure for six years, not even six months, weeks or days. These buyers hedge exposure on day 1.

So, they neutralize the value of the call so as to target something like approx 50% delta, so for every $1 billion of bonds that are issued, the convert bond arbitrage desks will short sell something like $500m of equity to lock in immediate gains.

But, the preferred stock could be a bit different.

Given the indefinite nature of the option (read: PERPETUAL preferred), an uncapped call would hold EXTREME value, even if the call was striked laughably far out of the money, given the immense volatility and time value of the option (as laid out above).

Stepping back, the preffered market is just a relative larger scale than converts. For scale, the total size of the convert market in the United States for listed securities is 1,360 bonds worth $302 billion, compared to $572 billion in total for all preferred stock.

However, narrowing the parameters to what $MSTR is looking for: a 0% coupon issue attractive to arb desks is a much smaller market. There is a total of $50 billion of zero coupon convertible debt for listed companies in the United States. $MSTR is already far and away the largest and most active issuer in this market.

Time to level up to a larger pool of capital.

The market for preferred stock in the U.S. is large, and the allocator class is entirely different, with much deeper pockets.

A question to all preferred stock buyers by forced mandate: Would you like exposure to a random tranche of the thousandth largest regional bank, Utility companies, and/or REITs, or would you like low volatility, high sharpe ratio upside exposure to the world's preeminent Bitcoin Treasury Company?

No comparison.

So, what's it all mean?

In essence, $BTC has infiltrated the fixed income market; and the dreaded uncertainty (read: volatility) that every smug TradFi allocator spent the past 15 years making fun of, is the very reason that these $MSTR preferreds will likely be the top performing preferred security in the market before long, just like the $MSTR converts and the common stock have been.

$MSTR bears have no idea what just hit them.

Oh, and don't get me started on the potential BTC Yield here...

END/

2025 predictions:

- SBR happens

- Ross Ulbricht freed

- 50% Bitcoin correction at some point

- Bitcoin goes north of 500k

- MSTU/MSTX blow up. BITU/BITX don’t

- 3 total G7 countries announce SBR’s

- Market climbs a wall of worry

- basically everyone and everything is annoying