1/11 🧵

Bitcoin just wiped out $1.28 BILLION in long liquidations over 5 days.

This was not a normal pullback.

But the liquidation chart is only the first layer.

Here is what is really happening:

🚨 ORACLE BET ITS ENTIRE FUTURE ON AI AND IS NOW DROWNING IN $108 BILLION OF DEBT.

The chart tells exactly how this happened.

In June 2025, Oracle jumped 13% on earnings. In September 2025, it exploded 41% in a single session to an all time high of $345 as Wall Street priced it as the core infrastructure play of the AI boom.

Then institutions used that narrative to sell for 6 straight months straight into retail buyers.

The stock collapsed 60% from $345 to $121. Then -11% on the next earnings. Then +9% bounce.

But what caused the crash ?

To fund its AI expansion Oracle is raising $50 billion through debt and equity dilution in 2026 alone. Total debt has ballooned to $108 billion. Free cash flow is now negative $13.1 billion.

Credit default swap spreads have widened to historically elevated levels, the market is pricing in meaningful default risk on a company that was trading at an all time high 8 months ago.

Over $300 billion of Oracle's $553 billion backlog is tied to OpenAI alone.

A single client that has never turned a profit and loses $14 billion a year. When OpenAI missed its internal growth targets in April 2026, Oracle stock dropped 7.5% in a single session.

That is what single client concentration risk looks like in real time.

Cloud revenue grew 44% last quarter. Q4 revenue forecast is $19.1 billion.

The growth numbers are genuinely strong. But the balance sheet is burning and the entire thesis depends on OpenAI being able to honor $300 billion in commitments.

June 16 earnings will either validate the most aggressive infrastructure bet in enterprise software history or confirm that Oracle mortgaged its balance sheet on a client that cannot deliver.

The stock has moved between 9% and 41% on each of the last four earnings days. This one will not be different.

People who think a 5-year consolidation for $ETH isn't healthy and is bearish are suffering from recency bias.

They don't remember that $NFLX went through a very similar pattern from 2004–2009.

Just look at the chart below—the similarities are quite impressive.

Still bearish?

Short interest on US stocks is at multi-year highs:

Short interest in the median S&P 500 stock is up to 3.0% of market cap, the highest since 2012.

This is DOUBLE the levels seen during the 2020 pandemic.

By comparison, at the peak of the 2008 Financial Crisis, short interest in the median S&P 500 stock stood at 3.8%.

Furthermore, short interest among the most heavily shorted 10% of S&P 500 stocks is up to 8.0% of market cap, the highest since 2018.

Both metrics are now even higher than during the bear market following the 2000 Dot-Com Bubble burst.

Are markets setting up for a short-squeeze?

🚨 ANOTHER ETHEREUM BUILDER JUST SHUT DOWN

Syndicate Labs is closing after 5 years of building infrastructure for custom Ethereum rollups.

The company said the market has shifted away from its technology, “making it impossible to wait out these market conditions.

As the recently expanded partnership with @AnthropicAI demonstrates, @SpaceX is offering AI compute as a service at significant scale.

We are in discussions with other companies to do the same.

Over time, especially with orbital data centers, we expect to serve AI at extremely high scale.

In the last year, the world has printed 9.3% more money.

Global M2 money supply has reached $141T in 2026.

When inflation starts to run hotter again, they will blame it on Iran and other proximate factors.

But the root driver is the money printer has been running hot for the last year. Where?

China increased their money supply by 13.6% in the last 12 months. Their M2 is now $50T, making it the largest global driver of fiat inflation.

US growth in M2 is just 4.6% over the last 12 months, making the US comparatively responsible. (But make no mistake, this means your dollars have been debased by almost 1/20th of their value in just a year.)

Since we live in a global economy, we're subject to the aggregate impact of GLOBAL money printing. The US has been accustomed to being the largest monetary base and therefore largely controlling global debasement.

But China's money supply is now 2x as large as the USA's. Your savings are being debased by Chinese monetary policy decisions and you have no control.

Nobody asked your permission. Nobody told you it was happening.

But your savings just got diluted by 9.3% in one year.

Note: I'm currently updating the Global Asset Landscape for 2026 (see prior tweet). It will be out in the next few weeks, stay tuned!

🚨 THE S&P 500 WITHOUT AI TELLS A VERY DIFFERENT STORY

From May 2024 to June 2026, the S&P 500 soared 142%. But excluding AI stocks, the broader market gained just 16%.

The gap highlights how a handful of AI giants are driving nearly all market gains, fueling growing concerns that the current bull market is becoming dangerously reliant on the AI trade alone.

A video game I played at age 14 helped me learn how money actually works.

Here is what I discovered:

When I was in my early teens, I spent most of my free time playing Diablo II.

Like most games it had its own in-game currency, but the currency was so easy to come by that it didn’t have much value in trade.

So players did what humans have always done when their money fails them and found something else to use as money.

There was a rare ring in the game called the ''Stone of Jordan'' Ring (the SOJ) that was hard to find and useful enough that people valued it.

Although the game designers never intended this, the entire economy of Diablo II started using the SOJ as money.

Players started trading gear for SOJs, quoting prices in SOJs, and storing wealth by accumulating them.

The in-game currency was all but worthless because it was so easy to come by, but the SOJ was scarce and people recognized it.

Although I didn’t have these words at the time: I had just watched a free market select the SOJ as its own money. Witnessing this monetization process left a lasting imprint on my mind that decades later would give me an early appreciation of Bitcoin.

Once I understood what was happening I stopped dungeon slaying and started trading, instinctively following the basic principles of buy low and sell high until I had accumulated a wealth of rare items.

Then eBay became popular and I realized I could convert all that in-game wealth into actual dollars, and that was the moment something cracked open because people were spending “real money” to acquire valuable items inside a world that did not actually exist.

That was the first time the penny dropped for me.

I followed that intuition for the next two decades without knowing where it was going and it took one book to give it a name.

At 21 I read “The Creature from Jekyll Island” and learned what central banking actually was and the realization was so heavy I put it down, went back to work, and told myself there was nothing anyone could do about it.

Without knowing any other path I continued working inside the financial system despite understanding its corrupt core.

Then in 2018 I read “The Bitcoin Standard” and the two threads finally connected.

The free market digital money I watched emerge spontaneously inside a video game (the SOJ) and the free market digital money I was watching emerge spontaneously in the real world (Bitcoin) were both built on similar principles.

The common denominator? People always seek out the best tool for the job. When their money doesn’t work right, people find a better monetary tool.

Since the money people choose to hold is a matter of survival in the social world, it is extremely difficult to force people to use an inferior money when a better money is within reach.

My philosophical journey into the nature of money started with a video game and ended with a Bitcoin tattoo (my first and only tattoo to this day).

To me, this Bitcoin tattoo represents my “skin in the game”: which is a principle of alignment between people and the consequences of their actions.

The problem with central bankers and their fiat currencies? They have zero skin in the game. When they print money, you lose value. Their actions, your consequence: this is the misalignment.

Bitcoin is the reverse.

Bitcoin is a system secured by miners and holders.

These incentives n Bitcoin ensure that each person bears the consequences of his own actions.

The net result of Bitcoin being a monetary network with skin in the game is that it is money that can never be printed. This is because to create more than 21M Bitcoin would require a majority of users to act against their own self interest.

By giving people an incorruptible option in a world running on corrupt money, Bitcoin is one of the most important humanitarian missions in the world.

My Bitcoin tattoo is my “skin in the game”: a visual metaphor for my commitment to this humanitarian mission.

If actions and their consequences are misaligned, it is only a matter of time before the system blows up.

Bitcoin fixes this.

BREAKING: Tether purchased +6 tonnes of gold in Q1 2026, bringing total holdings to a record 132 tonnes, now worth ~$19.8 billion.

This follows +21 and +26 tonnes acquired in Q4 and Q3 2025.

Tether’s gold holdings have more than DOUBLED in just 12 months and nearly TRIPLED in value over the same period.

In 2025, the crypto firm acquired more gold than every central bank except Poland.

In Q1 2026, the only central banks that bought more gold were Poland, Uzbekistan, Kazakhstan, and China.

Tether is competing with central banks for gold.

Bullish monthly morning star pattern printed for #Bitcoin.

It has marked 3 out of 4 past cycle bottoms.

It has marked 2 very important local bottoms.

It has given 2 false signals, which makes the success rate of this bullish formation working out 71.4% for #Bitcoin.

I started by trying to understand markets. Thirty years later I've ended up somewhere closer to life, the universe and everything. The same four rules keep showing up...

Along the way I've written three frameworks that have shaped how a lot of people see the world.

The Everything Code is what I found when I went looking for what actually drives markets. A debt rollover cycle, managed by liquidity, debasing the currency at roughly 8% a year. That debasement is monetary entropy. Capital routes around it, into whatever can compound faster than the entropy degrades it. Technology and crypto sit at the top of that flow because they are the intelligence layer of the economy. Markets are monetary energy routing toward the highest output of intelligence. The only assets that outperform debasement over extended periods are tech and crypto.

The Exponential Age is the realisation that technology has become the substrate. Compute, networks, energy and intelligence are compounding faster than any institution we built was designed to handle, and the gap between the two is the defining tension of our time.

The Economic Singularity is where this is heading. Somewhere in the next decade the curve of intelligence per unit of energy turns fully exponential, and the rules every economy we know was built on stop applying.

For a long time I thought of these as three separate ideas. Looking at them now, they are three views of the same thing at different altitudes. And underneath all three, the same four rules keep showing up.

Efficiency of Intelligence - The universe rewards whatever does more with less. Every system that survives is better at turning energy into information than the system it replaced. There has never been an exception.

Compression - Intelligence is the act of representing a vast reality in a much smaller form without losing what matters. Brains do it. Theories do it. Prices do it. AI does it. They are not analogous. They are the same operation.

Coherence - Complex systems hold together because their parts synchronise faster than the noise around them. Markets, brains, civilisations, ecosystems. When the synchronisation fails, what looks like collapse is desynchronisation made visible.

Selection - Patterns that copy themselves faster than their rivals dominate the medium they live in. Genes did this in biology. Ideas do it in culture. Memecoins do it in markets. Truth is not part of the selection criteria. Replication is. It always has been.

What the four rules produce, when they operate together, is networks.

The same topology shows up everywhere. The cosmic web. The human brain. Mycelium beneath a forest. The internet. Financial markets. Blockchains. Across fourteen orders of magnitude, the universe keeps building the same shape. That shape is what the four laws look like when you can see them.

The Everything Code is what these four rules look like in markets.

The Exponential Age is what they look like running through technology.

The Economic Singularity is where they are taking us.

Three angles, one picture.

Underneath all of it, energy is the constant. Consciousness is the substrate. The four rules are the dynamics through which one becomes the other.

All of this is one corner of what I call The Universal Code. The same four rules apply to everything else and I mean EVERYTHING... they are universal in the true sense of the word.

The next test for BTC is cleanly breaking the cost basis of recent investors (79k).

I give it 30% odds on doing this on this attempt. After that, if BTC manages to hold this price level above 65k and not break down, then the chances of a structural bottom increases significantly.

BTC is currently attempting a bottom, but all the pieces are not yet in place, the next 3-6 weeks will be telling.

105,000 BTC vanished from exchanges in 7 weeks.

30D Net Flow also hit -300K BTC in March.

Less BTC on exchanges = less available supply to sell.

Morning Brief 152 👇

https://t.co/OvRoHEE41d

In crypto and defi (ie in honest markets), when a component fails, those closest to the component—whether wildly negligent or innocent victim—suffer the loss, and are burdened with that responsibility. Unequal, but proper.

In tradfi and banking (ie in coercively manipulated markets), when a component fails, the entire society is forced under the burden of its resolution. Costs are socialized. Equal, but improper.

The former, with time, becomes self-correcting, self-improving, and crucially, retains vitality. The latter, regardless of time, becomes stagnant and soulless, and here everyone can wallow in an equivalent grey.

Any man of agency should prefer the former, taking care over that to which he is proximate. It is from this that the virtue of markets emerges.

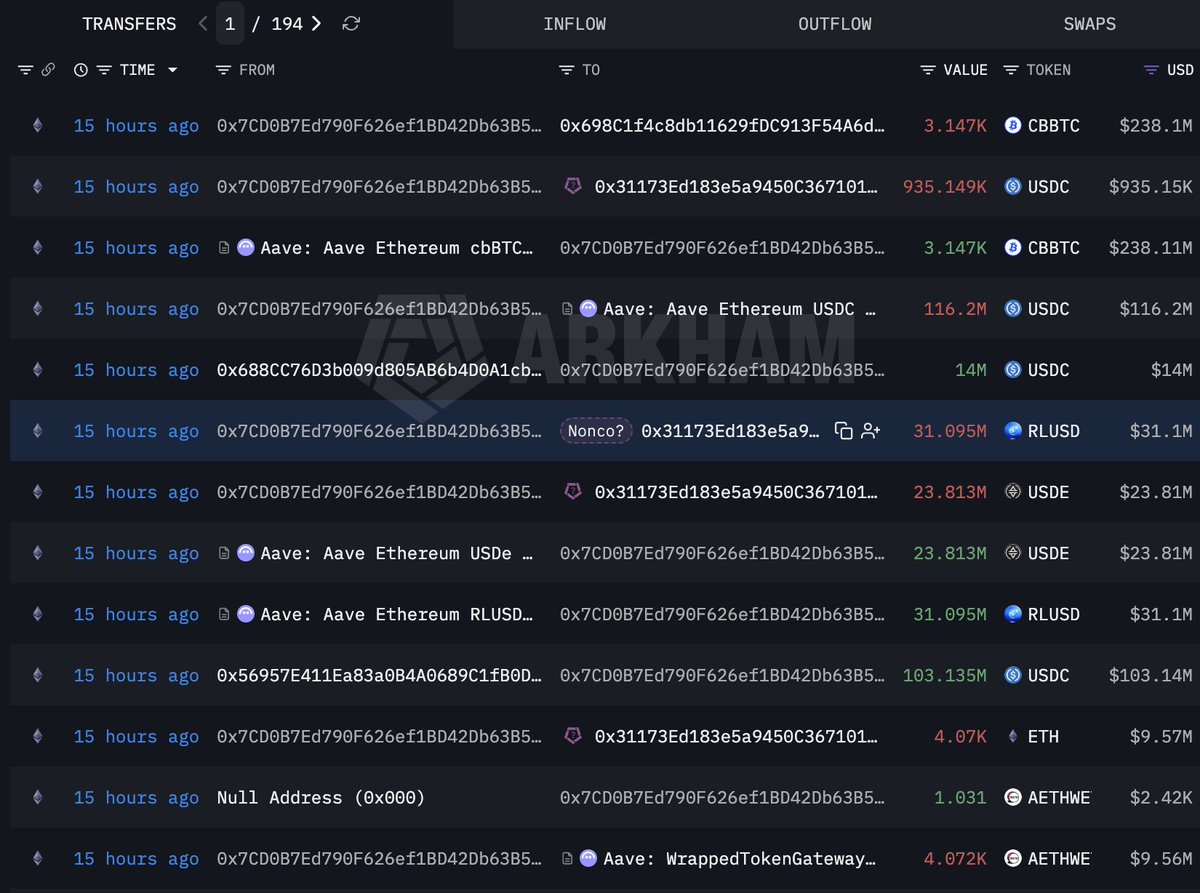

$290M just EVAPORATED from DeFi and most people have no idea what actually happened.

Step 1: attacker exploits KelpDAO's LayerZero bridge. Mints 116,500 rsETH out of thin air.

Step 2: deposits the unbacked rsETH on Aave V3 as collateral.

Step 3: borrows $236M in WETH against it.

Step 4: rsETH loses its peg. Positions become unliquidatable. Protocol is left holding the bag.

Now watch what's happening everywhere else.

ETH pool: 100% utilization. Lenders can't withdraw.

USDC pool: 100% utilization.

USDT pool: 100% utilization.

Why? Because everyone with rsETH exposure is scrambling. They're borrowing stables against whatever healthy collateral they have left, rotating out of ETH exposure, prepping to repay loans before liquidation cascades hit.

It's a bank run in reverse. Draw down the credit line before the pool freezes.

Aave has options. The Umbrella backstop can absorb the deficit. Governance can vote to socialise losses across suppliers. The DAO treasury can cover part of the shortfall. Recovery negotiations with the attacker are on the table. None of these are fun, but the protocol has been here before and survived.

This is the cost of DeFi composability. One bridge breaks, and the shockwave moves through every protocol that whitelisted the asset. No circuit breakers. No grace period. No committee to call.

That's the tradeoff. Permissionless markets mean permissionless risk.

Know what you're holding. Know what it's backed by. Know what happens when it isn't.

Due to the KelpDAO exploiter borrowing over 82,600 $ETH ($195M) from #Aave using $RSETH as collateral, bad debt has appeared on #Aave.

Many whales have withdrawn funds from #Aave, causing its TVL to drop from $26.396B to $20.114B — a decline of $6.28B.

Major withdrawals include:

• MEXC withdrew $431M

• Whale 0x7CD0 (possibly linked to Nonco) withdrew $405.7M

• Abraxas Capital withdrew $392M

...

⚠️ALERT: $AAVE is now down -19% today after a $292M Kelp DAO rsETH exploit triggered a full-blown liquidity crisis.

Aave's ETH pool just hit 100% utilization. That means one thing: there's almost no ETH left to withdraw.

Here's what happened:

Attacker drained 116,500 rsETH ($292M) from Kelp DAO's LayerZero bridge

He then deposited the stolen rsETH as collateral on Aave V3 to borrow ~$236M in WETH.

Because the rsETH is now unbacked, those positions are unliquidatable.

Aave is now stuck with ~$280M in bad debt it cannot recover.

Panic withdrawals have followed: $5.4 BILLION in $ETH outflows, with Justin Sun pulling 65,584 ETH ($154M) alone.

ETH utilization has maxed out at 100%, which means there's almost no ETH left to withdraw.

This is the FIRST real-world test of Aave's Umbrella safety module & the BIGGEST DeFi exploit of 2026.

This is a developing story.