🚨June Existing Home Sales

Non-seasonally adjusted of 422K🆙7.9% YoY & MoM

On avg, sales⬆️8.52% from May to June

SA⬇️MoM

That price though ($440.6), up 1.8% YoY...just wait until distressed sales enter the chat in Q3 & Q4

Since 1999- 4th worst June behind 08, 24 and 25

🚩We want the investors to know this: None of what we have analyzed below appears on any single line of the balance sheet. The retail investors see a fund. The banks see collateral. Beyond that, no one knows or seem to care about the risk.

What a shallow way to bait the investors. So far we have dissected and analyzed... see below

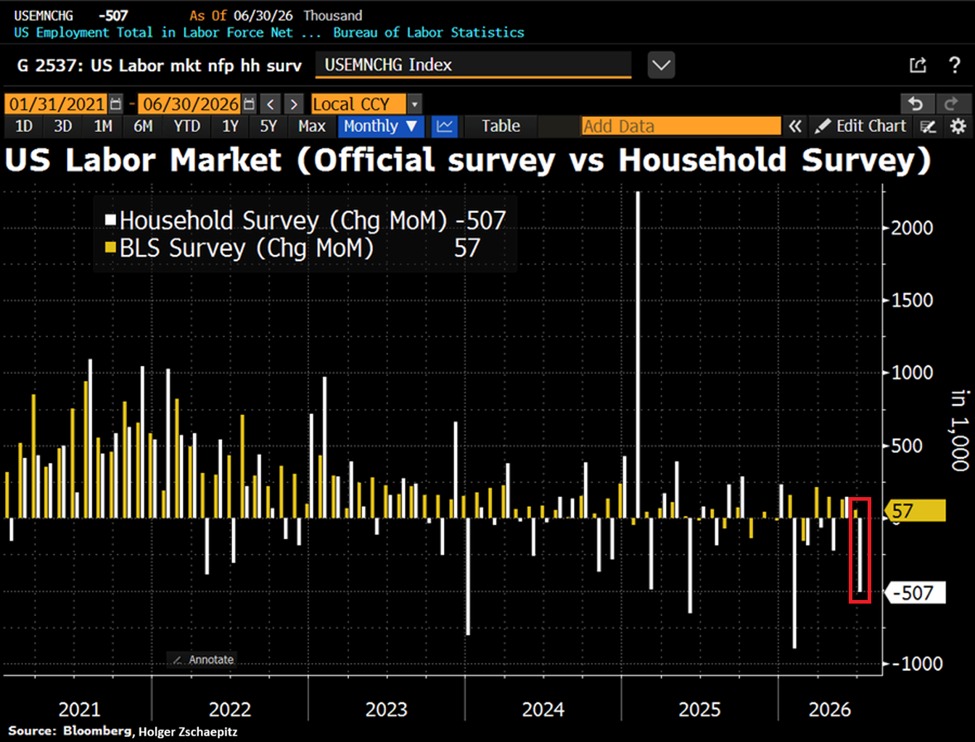

What is happening with the US labor market?

The difference between nonfarm payrolls and the household survey was a massive 564,000 jobs in June.

This comes as Thursday’s job report showed +57,000 non-farm payrolls were added last month.

At the same time, -507,000 Americans lost their job, the 3rd-largest drop since January 2024, according to the household survey.

The household survey is a closely followed metric because it counts each worker only once, even if they hold multiple jobs.

Year-to-date, total employment in the household survey has declined -1.7 million, to 162.26 million, the lowest since December 2024.

Over the same period, total nonfarm employment has risen +552,000, to a record 158.98 million.

Something does not add up here.

“it is factual that the value proposition of closed-source AI labs looks increasingly unsustainable. I mean: you're paying 10X the price of Chinese 🇨🇳 open-source AI models for something that's not really better (or just marginally) & on top of that you have zero control over your data, or the models themselves.”

“Sometimes it takes a vulture to tell you something is dying ☠️…”

🔥 🔥 🔥 🔥 🔥 🔥 🔥 🔥 🔥 🔥 🔥 🔥

Alex Karp of Palantir just exposed what has been bubbling under the surface.

The large enterprise customers of AI are hitting the pause button due to data safety issues.

Downstream of that demand pause is AI capex. The Second derivative of pick and shovel guys is about to slow and with it stock momentum.

DOJ investigating odd stated NAV behavior by one the largest private credit funds.

Ever larger redemption requests across private credit each quarter.

Lawsuits alleging valuation fraud and less than stellar liquidity feature explanations.

“Don’t worry. Everything’s fine.”

Yesterday's technology-led selloff did not occur in a vacuum. Several developing narratives are beginning to converge, creating the first meaningful challenge to AI leadership in months.

The selling pressure culminated in a decisive distribution day on the Nasdaq, as the technology-heavy index closed below its 50-day moving average for the first time since reclaiming it on April 8. Volume expanded from the prior session and finished above average, signaling meaningful institutional selling rather than routine profit-taking.

Market leadership narrowed noticeably as capital rotated toward more defensive sectors. Consumer Staples, Health Care, and Utilities attracted relative strength, while Technology stocks bore the brunt of the selling pressure.

Bull markets do not die because of of old age. The chart above shows that the 1998 case (dot plot in the far upper right corner), which has drawn a lot of comparisons to the current bull, lasted the longest and registered the highest return of any bull market since 1928. In total, five prior bull markets lasted longer than the current one and eight posted higher returns.

One similarity to the late 1990s is valuation. By most measures, stocks look overextended. The total stock market capitalization relative to GDI is at a record high, and very close to the reading reached at the 2000 peak.

Until the market shows signs of renewed strength, investors should remain selectively cautious. Protect capital, avoid lagging names, and reduce exposure in positions that violate stop levels or show clear signs of price violations. Extended stocks showing decent profits should be back-stopped to protect gains.

https://t.co/JXzFFTmMtn

🚨PSA: We are building a map of direct lending PC funds, line by line, down to each borrower, then tracing each exposure back to the company's fundamentals for our deep dive research.

We are looking into the loan books, not the headline news. If it is useful to you, access below.

So... we are pretending to "stress test" the banks while ignoring those banks' exposure to PC and quiet SRT deals?

In this day and age, having brain cells is a painful luxury. Those who possess have had to read news like this: " $JPM and Goldman increase dividends."

Goldman: aggressively expands into PC.

JPM: at least $50B in direct exposure to PC.

Both Goldman and JPM off loaded billions in SRTs.

https://t.co/ACtLD0VT2Q

Quietly, $HGRAF’s graphene is already inside two commercial battery products.

Not announced with fanfare.

Just sitting on Sigma-Aldrich and Fuel Cell Store right now. 🧵👇

New $HGRAF Compounding Partner just certified – and this one is a big deal.

Modern Dispersions (MDI): 18 extrusion lines, 300 MILLION lbs of annual production capacity, 5 decades of carbon black expertise. 🇺🇸

Fractal Graphene just got a serious manufacturing runway. 🧵👇 $HG

What will it take for graphene-reinforced plastics to reach mainstream manufacturing?

HydroGraph has demonstrated up to 100% property improvements at low loadings and continues investing in the research and compounding expertise needed for commercial scale adoption.

$HG $HGRAF

Stocks and housing have never been this expensive relative to the U.S. economy.

Stock market value: 250% of GDP.

Housing value: 146% of GDP.

This is the first time in modern U.S. history both have simultaneously approached record valuations.

In 2000, it was mostly stocks.

In 2006, it was mostly housing.

Today, it's both.

“Lost in SpaceX”

The real space race runs in the opposite direction the market is betting and it’s a vastly superior bet.

The focus shouldn’t be outward into the void. But, inward, into the angstrom: atomic-level interactions, molecular construction, building matter from the bottom up.

While capital chases the spectacle of atmospheric escape, the actual new frontier is the smallest scale of reality, where stronger, safer, cleaner, fully recyclable, highly efficient materials are made atom by atom.

Nanotechnology, nano-engineering, and nanomaterials are where the next century of value lives. Not in fleeing the world, but in mastering it.

The market is looking up. It should be looking down…looking inward.

We aren’t just going to master materials for construction and manufacturing. We will be mastering biotechnology with nanotechnology. Curing diseases and bettering lives.

We don’t need Ai chips in space to solve the cooling and power issues. That’s ridiculous, what we need is better materials. The answers are here and the foundation of this new engineering world is stems from building with the ultimate scaffolding, turbostratic fractal graphene aggregates.

We’ve got what we need, the nano-carbon material that can change the world.

This month, we are recommending a bank that has $2B+ market cap. as a short.

Next month, we are recommending a tech company that has a market cap. of more than $100B+ as a short - no, it is not a company owned by Elon.

If you are interested in benefiting from our ideas and research, become our client before the price hike.