I DON’T UNDERSTAND WHY PEOPLE DON’T USE GROK FOR STOCKS.

Most traders are looking at charts from 6 months ago.

Grok analyzes real-time sentiment on X to predict future.

Here are 20 prompts to find the next 10x stock:

🚨 The GOAT Stan Druckenmiller just rewired his portfolio.

This isn’t a cosmetic rebalance.

He’s pushing size into three big themes:

High growth biotech

AI compute + power infrastructure

Emerging market consumer/internet

Here’s what he actually added and why it matters 🧵

$IREN signing a $9.7b cloud contract with $MSFT is a thesis-defining moment for shareholders

For the last couple of years, doubters have argued that $IREN is just another $BTC miner or, in recent months, that they can’t compete with the likes of $NBIS or $CRWV because they lack "software orchestration".

Well, it turns out that all of these doubts were severely mis-guided.

Investors who did extensive research and analysis of the AI sector understood that it was always just a question of time — not merely because $IREN "has the power", but because they have world-class engineers and a one-of-a-kind CTO in Denis Skrinnikoff.

Combine that with excellent leadership at the top & this was a forgone conclusion.

Now keep in mind, this multibillion $ deal — which, on the surface, appears to have a very strong ROIC profile — barely encompasses 300 MW (gross) of $IREN's ~3 GW power portfolio.

There will be many more deals, whether in hyperscale cloud contracts or in the form of high-yielding “premium” colocation partnerships.

This is truly just the beginning...

Congrats @danroberts0101 & Team. Couldn’t be prouder as a shareholder today! 👏🎉

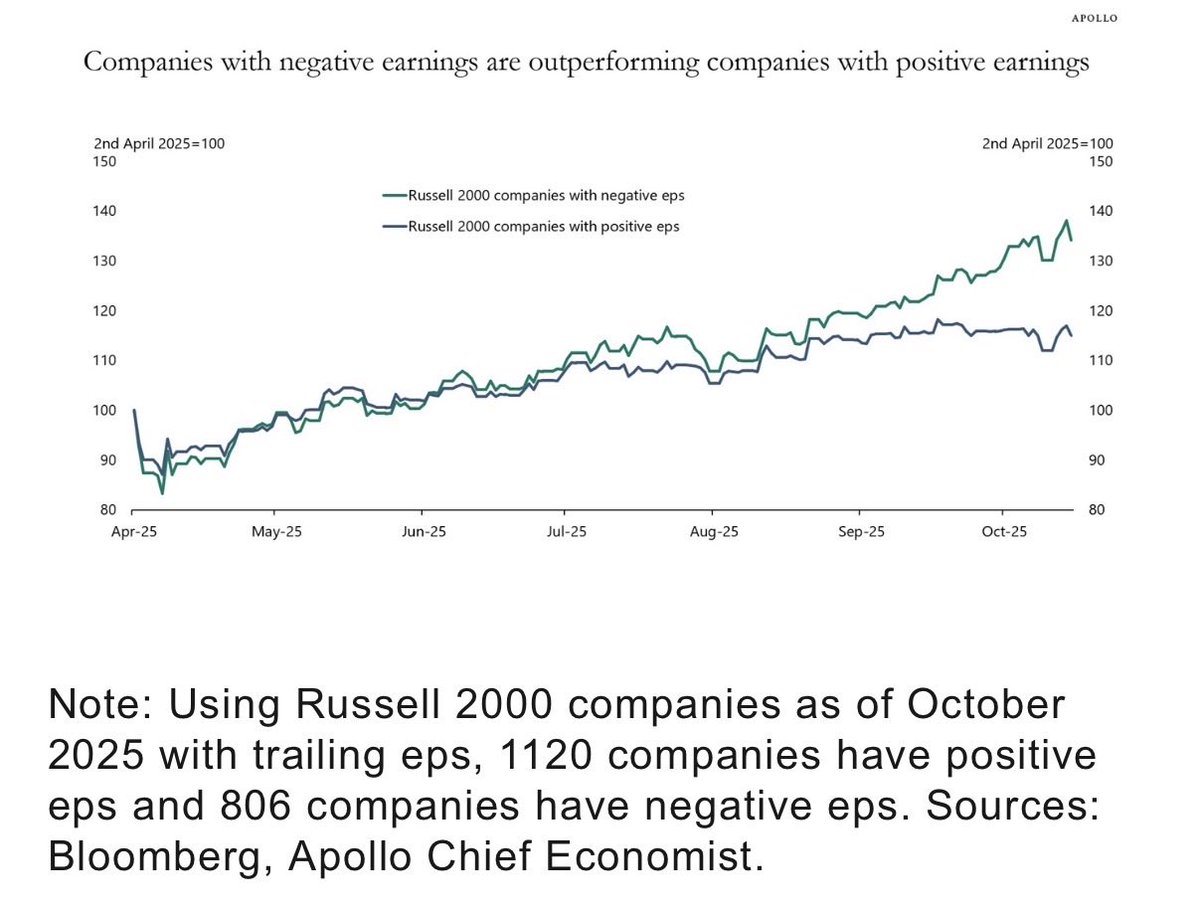

Apollo’s Torsten Slok observes that “something remarkable is going on in the equity market. Stock prices of companies with negative earnings have in recent months outperformed stock prices of companies with positive earnings” (chart).

This can be seen as part of a broader phenomenon in which some investors are reaching further and further for returns, pushed there by the widespread compression in risk premiums.

#economy #markets #risk #apollo

I went long $AMD at $4.2.

$HIMS at $15.

$PLTR at $7.

$TSLA at $13.

$SPOT at $97.50.

Now I'm focused on watching $RKLB, $ASTS, $OSCR, $HFG, $LMND, $ABCL and $IREN VERY closely

Here's my Q2 2025 update of these 7 companies🧵

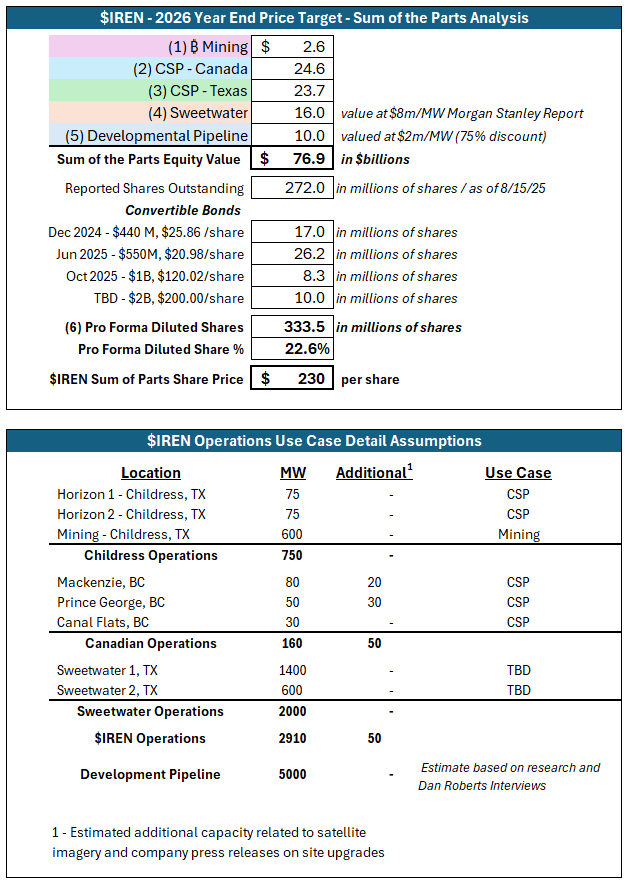

$iren / 2026 YE Price Target / $230 per share

Let me take a brief detour as an introduction to the analysis. For those that want to see the assumptions and valuation methodology, skip to Assumptions.

Overview

Like most of us, I am not yet retired and continue to work at my family’s third generation butcher shop in downtown Detroit. To say last week did not test the stomach of even the most experienced investors would be an understatement as the price volatility of $iren demonstrated the range of market sentiment from the highs of $74 mid week to the lows of $57 as market makers shook the trees during the October monthly option expiry. One minute you are picking out your favorite Waygu Tomahawk steak for dinner, and the next minute you are reverting to Ramen.

All of those emotions are natural, but the ability to quickly dismiss that momentary discomfort and screen through the headline de jour is the difference between being a speculator that makes money in a hot market to an investor with unshakeable conviction that is willing to see through the bull shit.

I’m reminded of the scene from Money Ball where Billy Beane, played by Brad Pitt, asks Peter Brandt, played by Jonah Hill, the following question related to their unconventional baseball player evaluation methodology:

“Do you believe in this thing or not?”

So let me take this moment to direct the question to you:

“Do you believe in Artificial Intelligence or not?”

There’s a good chance many of you answered “Yes” and may proceed. For those of you who believe a random Bitcoin whale going short or President Trump’s soybean infatuation are reasons to exit; we wish you luck.

Assumptions

Now the fun part; here are my key assumptions for the model:

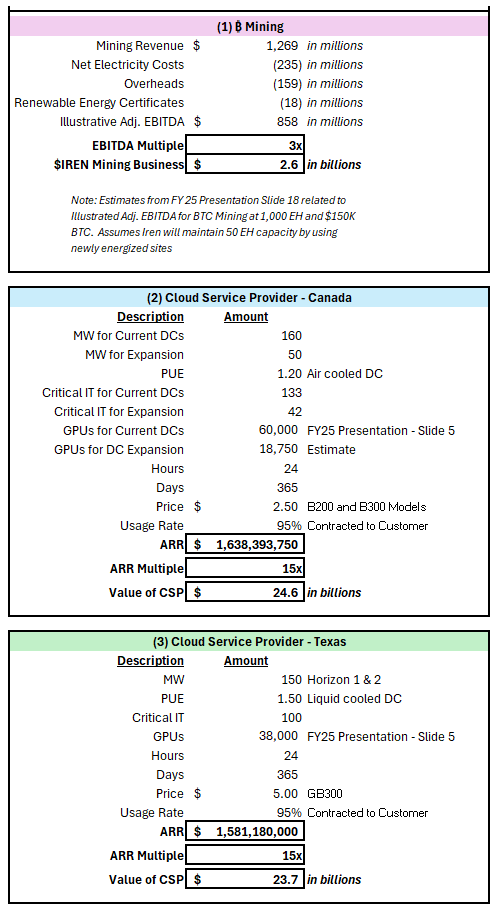

1. Bitcoin Mining – Bitcoin is currently trading at $108,000 this morning but in my experience the short-term pain of chopsolidation leads to explosive growth. Global central banks continue to print new M2 at will and gold performance usually serves as a good indicator for future bitcoin prices.

2. CSP Canada – The company did not officially disclose the 50 MW expansion projected in the model but there are multiple hints related to site upgrades along with satellite imagery from @FransBakker9812 that support this speculation.

Both rates for Canda and Texas relate to a slight premium being added to the breakeven cost per MW analysis conducted by @TheKamaHsutra . I value @litigious_dulce opinion that management will aggressively price capacity to take market share and apply margin pressure to competitors like $orcl, $nbis, and $crwv that continue to pay colocation fees as part of their asset light approaches.

3. CSP Texas – The ARR multiple of 15 assigned to both Canada and Texas attempts to bake in some conservatism but there remains room for expansion as $crwv and $nbis currently trade as high as 18-20 and 25-30 times ARR respectively.

4. Sweetwater – Consider the Morgan Stanley 2024 study valuing each MW between $5-12m per MW as well as the recent @BlackRock purchase of 5 GW of capacity for $8m per MW as the primary comps in my analysis. Also, consider that Stargate will have an estimated $500B of investment for a 7 GW site. Grid connection requests started today likely would not go live until 2030.

Jensen Huang, @nvidia CEO, repeatedly speaks in interviews to a future with AI factories. This vision of huge training clusters only can be achieved with large contiguous sites as companies like @OpenAI work towards super intelligence.

5. Developmental Pipeline – Consider that @danroberts0101 and Will started acquiring sites as early as 2019, well before their peers, for pennies on the dollar of today’s market value and the recent $apld earnings call disclosing a 4 GW pipeline. The discount relates to site acquisition closure and grid connection risk.

6. Proforma Share Count – Primarily driven by announced convertible bond offerings but I also predicted additional financing at a higher share price via capped calls to help fund rapid expansion. The recent Secured Note closure of $wulf for $3.2B as well as the vendor financing provided for $iren GPUs suggest a healthy debt market that will allow $iren to continue to lever their balance sheet and rely less on equity to fund.

I would rather error on the side of conservatism at this time but remain adamant that as $iren must execute and scale quickly in order to compete with $orcl, $nbis and $crwv. Momentary dilution does not dissuade my belief as management continues to execute and allocate capital wisely.

Conclusion

I remain steadfast in my prior prediction that $iren will qualify for QQQ and SPY in 2026 but have not included these indexes into my analysis. Additionally, future sell side coverage by $gs $c after a successful convertible bond offering will help take $iren mainstream and proliferate institutional adoption that commands share price premium.

The most bullish projection I’ve seen on Wall Street is Cantor Fitzgerald $100 estimate but the reality is that sell side analysts are chained to their own institutional dogma. Their primary function relates to generating additional investment banking services for their respective firms and taking a more reactionary approach to analysis to not appear too reckless and adhere to CYA mentality.

While I remain a fully disclosed shareholder, I do not answer to anyone and can freely publish what could happen while acknowledging that management bears the burden of execution risk and there’s always more room for macroeconomic turbulence on the way to Valhalla.

NFA DYOR

@mikealfred@theBTCMiningGuy@ericjackson

$IREN is pleased to provide an update on its AI Cloud business.

- New multi-year AI Cloud contracts with leading AI companies

- Contracts secured for 11k GPUs, representing ~$225m AI Cloud ARR by end of 2025

- $500m AI Cloud ARR from 23k GPUs on track for Q1 2026

- NVIDIA Blackwell GPUs contracting ahead of delivery on an average term of 2 years

- Capacity for >100k GPUs across British Columbia campuses and Horizon 1 & 2

- Customer workstreams progressing through site tours, technical diligence and commercial negotiations

Press Release: https://t.co/nNABJL8qQm

Robotics is ultimately the next multi-trillion dollar industry.

Here's 5 underrated robotics plays in the niches 👇🧵

1. Teradyne | $TER

EV/Sales: 7.1x

FY26 growth estimates: 19.4%

TER’s main legacy business is automatic test equipment (ATE) and industrial automation solutions. They originally built their business by supplying semiconductor test systems to chipmakers, but they’ve managed to strategically diversify their business into robotics and industrial automation over the last decade meaning they’re now extremely well positioned to benefit from:

1. The ongoing semiconductor cycle.

2. The structural shift towards automation.

I don't think $TER is attractive today, but I'd add at those ranges where the multiple to growth rates make sense.

The 4 best robotics plays when you look at revenue growth relative to valuation are:

1. Accuray | $ARAY

2. Synopsys | $SNPS

3. Teradyne | $TER

4. Allegro Microsystems | $ALGM

$ARAY 👇

Hay empresarios en España trabajando con 70 años. Y no por gusto precisamente. Es porque están atrapados.

Para mucha gente, su empresa, el proyecto de toda una vida, se convierte en una jaula de oro al final de su carrera cuando quieren jubilarse.

Y es que en este país, si tienes una SL con empleados, no puedes simplemente bajar la persiana para jubilarte como si fueras autónomo y estás solo.

La ley te obliga a liquidarla, y eso supone pagar la indemnización por despido a toda tu plantilla.

Obviamente, un coste inasumible para muchos.

Esto deja al empresario con muy pocas salidas, y ninguna es sencilla:

• Encontrar un comprador que quiera continuar con el negocio.

• Ceder la empresa a un familiar, si es que lo hay y está dispuesto.

• Asumir un coste de cierre altísimo que puede comerse los ahorros de toda su vida.

Es la gran paradoja: te pasas 40 años creando empleo y riqueza, y al final, ese mismo empleo te impide retirarte en paz.

Por eso la compraventa de pymes es tan necesaria.

Es la solución para que el empresario que se retira obtenga el valor que merece por su trabajo.

Y para que otro más joven aproveche una estructura que ya funciona para seguir haciéndola crecer.

Siendo realistas, por suerte o por desgracia, es la forma más inteligente de garantizar que el esfuerzo de toda una vida no termine en una liquidación.

Week 24 of BTC Weekly Cycle, at ending phase. Refusing (for now) break to new lows. Consolidating via time (best kind). Ext tight Bollinger bands. Seasonal window opening. Best position of 4yr cycle.

We should be on the cusp(days) of major upside move. 4Yr Video Wed to explain.