If $MU LTAs are enforceable in a down market then it should help with stock re-rating here.

$MU is trading at 5x of what market perceives as peak earnings. If margins are not going to collapse beyond 2029 due to LTAs then earnings floor till early 2030s will be much higher.

$TSM raising capex guidance due to N3 node capacity expansion and not due to bleeding edge is rather abnormal. Shows that there are a lot of GPUs/ASICs that need to migrate from N4/N5 node to N3 and repurposing N4/N5 tools to N3 is not along going to meet the demand.

$NVDA just raised its revenue guide by ~20%+ and stock is up barely 2.5%.

The fear of a peak just keeps hitting the stock.

Street estimates for 2026 and 2027 is ~$750bn and Jensen just said $1tn in revenues.

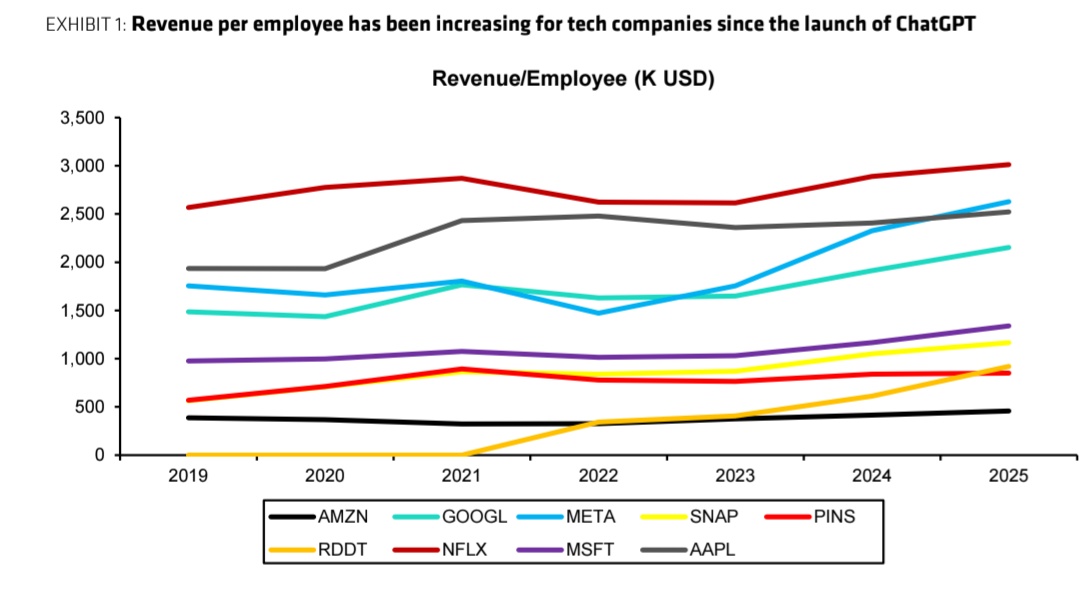

$META's revenue per employee after recent layoffs now stand at $2.5 million+ vs sub $2 million in 2019. Fastest growth among big tech.

AI should lead to massive cost tailwinds for most large cap tech names.

$META, $GOOGL, $MSFT

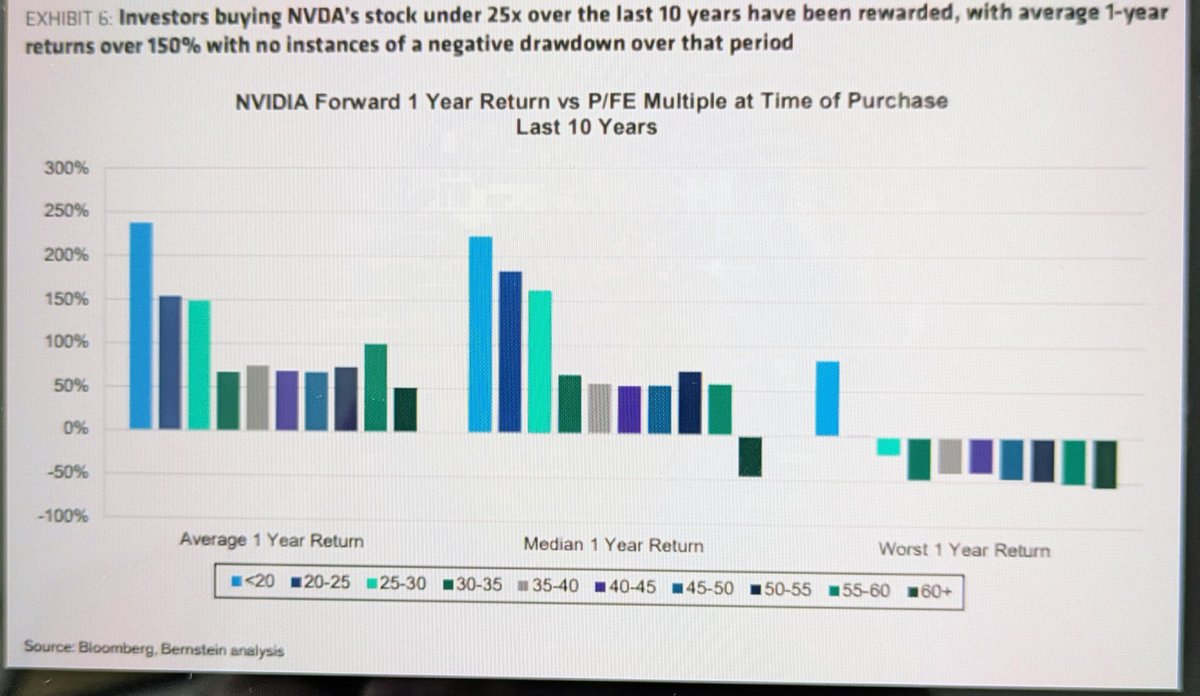

Buying $NVDA at current valuation has given 150% return with no instances of drawdown.

Only thing that seems different is that buyside has already modelled in $500bn of backlogs. So numbers are not moving higher and the fear we may hit peak in 2027/28 has caused this derating.

@TSOH_Investing $FND publicly admit that they should have pulled back on store builds much faster. They are hostage to macro but I appreciate how well they have managed through the downturn. This is the kind of stock you want to own on the other side.

@borrowed_ideas $CSGP is such a value destructive stock with a CEO that is unscrupulous. Only way out is Third Point and DEShaw launch a proxy fight and get rid of management.

Else Andy will have no oversight over him. He can burn 2bn next year, who is going to stop him.

Fail to understand what $CSGP is trying to achieve here. There are concerns around https://t.co/o77bpOo1s4 gowth + AI disruption risk and market share loss for https://t.co/JoyR2avr5K. By combining these two business segments, you are not helping investors to gauge health of biz

@Speedwell_LLC But half of that growth is garbage acquisitions and combining Homes and Multi-family will make it even harder to know how fast Apartments is growing vs Homes.

$BKNG also acts as merchant of record. $GOOGL never wanted to act as merchant of record even when it launched its travel offerings in search. Same will be the case with other LLMs as it brings you under the preview of regulators.

AI will take the path of least resistance.

"Morgan Stanley upgraded Booking Holdings to Overweight from Equal Weight and lifted its price target to $5,500 from $6,150, arguing BKNG remains central to online travel even as agentic tools evolve. The firm contends OTAs will continue to own the customer relationship, data, and merchant-of-record economics, with early agentic workflows largely redirecting traffic back to OTA apps/websites rather than disintermediating them. MS expects the industry structure to remain closer to paid search dynamics, supporting BKNG’s direct mix and long-term margin profile."

Continue to believe that market is not giving any credit to data moats and just focusing on what can be automated.

Case in point, #Anthropic calling out $TRI as the only place to get Westlaw data.

If you have data, then you will be more insulated.

$MDB, $VEEVA, $TRI, $SNOW

Bernstein put out a framework to evaluate disruption risk to software companies from AI. Framework uses

Automatability and Defensibility.

Seems like market is only focusing on automation risk right now and does not give any credit to data moats.

$CRM, $MDB, $NOW, $TEAM, $ADBE

Anthropic hosting a presentation on Enterprise Agents and messaging coming out of #Anthropic is that they are working with software providers. Not replacing them.

Not sure if the moves in software names stick.

$CRM, $MDB, $TEAM, $WDAY

We are in a market that shoots first and reasons later. 6% decline in $DASH is an indication of market raising odds of disruption risk.

@benthompson put out a compelling case on $DASH not being an AI loser.

An expensive stock can derate even if biz is going to be fine.

All these $DASH advantages in AI era applies to #Eternal#Zomato as well. #Eternal is an expensive stock, therefore, there is little valuation support and can derate further.

But the business will be fine.

While Fintwit is excited about dreaming up AI doomsday, $OAI is reducing its compute spend from $1.4tn to $600bn. Even if AI adoption is massive in coming 3 years, we may run into compute shortages.

$MSFT, $ORCL

We are in a market that shoots first and reasons later. It is tough to disprove any appocalyptic AI narrative. We need a few software companies to come out and post accelerating growth due to AI. This needs to happen for a few Qs before market gains conviction.

$MDB, $SNOW

Bernstein put out a framework to evaluate disruption risk to software companies from AI. Framework uses

Automatability and Defensibility.

Seems like market is only focusing on automation risk right now and does not give any credit to data moats.

$CRM, $MDB, $NOW, $TEAM, $ADBE

@modestproposal1 Tariff beneficiaries have already rallied so faded after initial news. Positive take here is Trump takes off ramp ahead of midterms. He will keep talking about it but does not follow through on 301 and 232.

Beyond my pay grade but consensus view is what you mentioned above.