Product building or investing—which do I love more?

🚀 Product comes first—it’s how I contribute to the world.

📈 Investing followed, driven by curiosity about business moats.

⏳ Both reward the same principles: long-term thinking, conviction, prioritization, compounding, storytelling, and delayed gratification.

Different crafts, same mindset.

There is so much I disagree with in this interview: that LLMs are not the future, that Big Tech is only investing because it has run out of hyper-growth ideas, that GenAI is a dead-end industry, that it’s ultimately just a boring hardware business, or that the entire opportunity is only a $10–30B TAM.

If we look at today’s AI power users, many already spend over half of their productive workday interacting with LLMs and AI agents.

Personally, I have Slack bots and email agents helping me communicate, a knowledge graph (popularized by @karpathy) powering my AI agents, and tools like Claude Code, Amazon Q Desktop, and Claude Cowork that I use throughout the day to simply talk and get work done. I genuinely don’t work the same way I did a year ago.

And this story isn’t unique to me. Across engineering, product, law, consulting, and research, power users are rapidly reshaping how they work. Some already have AI coworkers joining meetings with instant access to enterprise knowledge, surfacing context in real time, and automating follow-up work.

That’s why calling GenAI a dead-end industry or a $10–30B TAM feels disconnected from what’s already happening. If today’s power users are a glimpse of the future of knowledge work – as they have been in nearly every major technology shift – GenAI is poised to transform white-collar productivity in a way we’ve rarely seen before.

I also think Alex Karp’s comments are being interpreted far beyond what he actually argued.

His point was that without an application layer, GenAI is essentially a token factory. The application layer hardens the model, grounds it in enterprise context, protects enterprise IP from being transferred away, and turns raw intelligence into measurable business value. I completely agree with that.

That’s not an argument against GenAI. It’s an argument for building better GenAI products.

In fact, Palantir itself is investing heavily in making frontier models more useful for its customers. Why would it do that if it believed the technology was a dead end?

One point where I do agree is that frontier AI labs haven’t yet demonstrated software-like margins. Inference costs still scale too closely with revenue, and proving operating leverage remains the biggest challenge.

But that’s a statement about the economics of today’s AI labs – not about the long-term significance of the technology itself.

Frontier AI labs understand these economics better than anyone. Yet they’re still racing to build the strongest models because they understand two important things.

First, they know that software itself won’t be the moat in the long run – customer adoption will. If they build the best model, they can continuously ship high-value software products on top of it with relatively little incremental development effort, opening up entirely new revenue streams. We’re already seeing this with Claude Code, Claude Cowork, Codex, and many more products that will inevitably follow. They’re all application layers built around the underlying model.

Second, they understand the flywheel.

Stronger models → more users → richer real-world reward signals → stronger models.

As continual learning advances, that flywheel only gets stronger. The strongest models attract the most users, generating the richest reward signals for new use cases, which are then fed back into the model to make the next generation even better. We already see this dynamic today, where a handful of frontier AI labs are pulling away from the rest. Without strong open-source efforts from labs like DeepSeek or Nvidia’s Nemotron family, we’d likely be looking at an AI oligopoly much sooner.

Will every frontier AI lab survive? Probably not. Very few will.

But concluding that GenAI is a dead-end industry conflates company economics with technological impact.

The business models will evolve. The winners may change. But the idea that AI won’t fundamentally reshape knowledge work is the part I find hardest to believe.

Here's my full interview with CNBC, covering my bear case against generative AI, OpenAI's questionable finances, AI's lack of ROI, and how all of this is a symptom of the tech industry running out of hypergrowth ideas.

It's great to see the mainstream media discussing this.

I couldn’t agree more.

Without an application layer, GenAI is essentially a token factory. The application layer is what hardens the model, grounds it in enterprise context, and makes it useful for real businesses.

I also believe India should pursue sovereign frontier models.

One point from Alex that deserves more attention is how today’s frontier models improve. AI labs are increasingly learning from aggregate feedback and reward signals generated through real-world model usage. As deployment grows, those signals help improve future generations of models.

As techniques like continual learning mature, this could create a powerful flywheel:

Better models → more users → richer reward signals from real-world use → even better models.

We’re already seeing hints of this today. A handful of frontier AI labs are pulling away from the rest, and that gap could widen over time.

One reason this hasn’t become a complete oligopoly is that Chinese labs continue to release strong open-weight foundation models that anyone can fine-tune and build on. Those models have dramatically lowered the barrier to entry. NVIDIA’s Nemotron family is another important contribution that helps diversify the ecosystem.

From a strategic perspective, this is exactly why countries like India should invest in sovereign frontier models while simultaneously building world-class application layers on top of them. It’s not compute or models or applications – it’s all three.

@ManuInvests We saw this coming, I guess 😊

“ $META is reportedly developing a cloud business called Meta Compute to sell access to excess AI capacity, per Bloomberg.”

bitcoin:native just broke $60K, down ~50% from its $126K high. Bears say it’s “no longer a shiny asset.”

They’re confusing the trade with the instrument.

Just after Covid bans were lifted, I flew from the US to Europe with a significant asset in my pocket – carried as pure information. No bank. No permission. No customs. No intermediaries. Try that with gold, real estate, or a wire transfer.

That’s bearer settlement: self-custody, no central authority, no counterparty. With $BTC, you don’t have a claim on your money sitting in someone else’s system – you have the money. Physical possession, no permission needed. You are the bank.

That value proposition still holds. The price is a function of that first-principle value – which is exactly why I’m not selling the coins I bought long ago.

The recent narrative is that stablecoins offer the same thing as Bitcoin. No. Their issuers can freeze your funds, and you carry peg risk. Just because you don’t see the dollar depreciating doesn’t mean it isn’t. Put a 10-year chart of the dollar’s purchasing power on the table and we can discuss. Volatility, and the fact that Bitcoin doesn’t fit traditional valuation models, is not an excuse to spread FUD.

To be clear: this isn’t about dodging taxes. I pay every dollar I owe, gladly. But in a world of global mobility, why should I pay anyone a cut just to move my own assets? Why peg my hard-earned savings to a government’s currency risk?

I don’t get why so many people want to see Bitcoin fail. Why would you want to stay stuck in a world where your money moves slower than you can move yourself – or where you have to ask someone to take care of what’s yours? We need more positivity in this world. Maybe Bitcoin has gaps. Fix them – don’t wish it to zero.

I’ll keep holding my coins. But given the bearish setup, I’ll hedge the trade – not the instrument – with a small put. If $BTC falls, the put gains and funds buying more $BTC at lower prices. If it rises, I lose the premium – but the gain on the coins I’m already holding more than covers it. Either way, the position I actually care about doesn’t move.

I’m long on the $BTC instrument.

Portfolio reflection.

I’ve had some phenomenal individual stock returns:

GOOGL: +97% HOOD: +247%

But the uncomfortable truth is that YTD, my individual stock portfolio has lagged QQQ.

My largest holdings, AMZN, META, and UBER, have underperformed so far. I still have conviction in all three. These are great companies, and I believe value will eventually move up the AI stack toward products, agents, distribution, ads, commerce, and real workflows.

But I also have to admit what my portfolio is missing. I missed most of the AI picks-and-shovels trade.

At today’s valuations, I find it hard to enter many of those names because the math does not justify it based on what I have learned so far. But waiting forever for a perfect fundamental entry may also be the wrong answer in this AI expansionary environment.

So I am looking at a different path: momentum-based ETFs.

I plan to cut my losses in GRAB and look for entry points in SPMO and PTF (combined < 5% of portfolio).

GRAB is not a bad company. Quite the opposite. I still think it is a great business. But the market is increasingly rewarding core AI infrastructure, and companies directly tied to the current expansionary AI cycle.

As investors, we have to adapt. The more I study SPMO and PTF, the more I like their methodology. Their long-term annualized returns have been impressive. For an investor like me, willing to hold through volatility for years, momentum may be a better way to participate in this phase of the market than forcing myself into individual names where valuation does not work.

Still learning. Still adapting.

DYODD.

My current allocation in the SpaceX IPO 😊

Not enough to move a portfolio.

Enough to remind me why I love technology.

SpaceX is one of the rare companies that expands the frontier of what’s possible and makes an entire generation think bigger.

I’ll be watching closely for an entry point 🕰️

Tomorrow, one of the most extraordinary companies of our time is expected to hit the public markets.

I won’t be buying, not because I doubt the company, but because the current entry point doesn’t fit my risk/reward appetite.

That said, credit where it’s due. There are few companies that have inspired a generation of engineers, builders, and dreamers the way SpaceX has. Its impact will be felt for decades.

Go #SpaceX

The debate around GenAI ROI is happening too early.

We’re still too early to judge GenAI primarily through a finance lens. At this stage, first-principles product thinking is far more useful than ROI analysis.

Language is one of the core technologies that enabled humans to coordinate, transfer knowledge, invent, and build complex societies.

For the first time, machines can understand and operate on that layer across text, speech, and images.

Prompting, memory, context engineering, agents, and personalization are just the first set of primitives. We’re still discovering how to harness this capability.

The biggest GenAI breakthroughs are probably still beyond our ability to articulate. We have an intuition that they’re coming, but we don’t yet have the mental models to describe what they’ll look like.

That’s why the hyperscalers are spending hundreds of billions of dollars. They’re not betting on today’s ROI. They’re betting on a new computing primitive.

Given what we’ve already seen in just a few years, you’d have to be extraordinarily skeptical to believe this technology won’t generate profound long-term ROI.

The difference between 10% and 20% returns is 24 years vs 12 years to 10× your capital.

Every investor should memorize this:

5% → 47 years to 10×

10% → 24 years to 10×

15% → 16.5 years to 10×

20% → 12.6 years to 10×

25% → 10.3 years to 10×

30% → 8.8 years to 10×

Compounding compresses time. Time builds wealth.

$UBER is doing to AVs what Amazon did to logistics.

Still hearing "AVs will kill Uber" in 2026. Meanwhile, Uber committed $800M to AV fleet partnerships in a single week: $500M with Lucid (35,000 vehicles), $300M with Rivian.

They're not building AV tech. They're building the marketplace where every AV fleet deploys. Same playbook as Amazon FBA: let others build the product, own the distribution.

Apple entering AI glasses might look like competition for $META.

It’s actually the most bullish signal for Meta this year.

Meta has a multi-year head start shipping real consumer AI via Ray-Ban smart glasses, trained on actual user behavior at scale.

Apple validating the category brings mainstream attention.

But Meta owns the data flywheel. In platform shifts, the company training on real user data usually wins.

Slack is quietly becoming a collaboration layer for AIs

I now have multiple agents running on schedules, each doing specific jobs and posting outputs into dedicated Slack channels.

Each agent has its own “workspace”

All coordinated by a chief-of-staff agent

This setup is starting to feel like managing a team, not tools.

Replaced my VPS setup with 2 local minis.

Now running AI agents to automate:

• product research

• company analysis

• daily workflows

Next: fully autonomous loops.

Agents already find and construct information better than I do. It’s time to remove myself from the loop.

Seems like the bet on $IOT is starting to pay off.

Samsara is up ~15% today after earnings.

The company delivered 28% revenue growth, 30% ARR growth to $1.89B, and another EPS beat ($0.18 vs $0.13 expected).

Strong execution, financial discipline, and customer obsession are creating a very sticky platform with significant upsell potential.

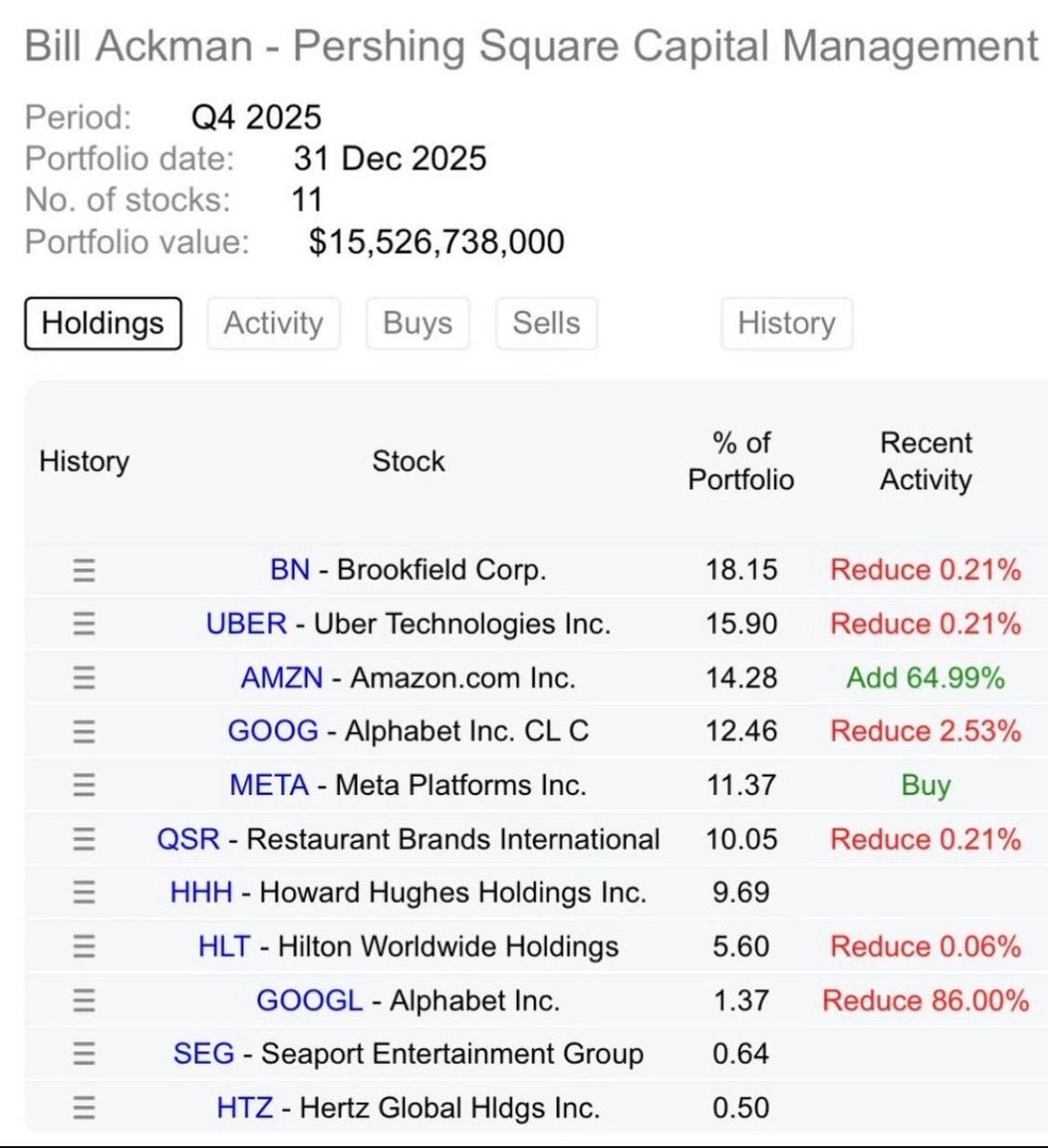

Is Bill Ackman replicating my portfolio? 😄 I wish (maybe one day).

But it’s good to see a highly successful investor backing companies I’ve held for a long time: $AMZN, $META, $GOOGL, $UBER.

I’ll continue to double down on these compounding machines. They’re exceptional at execution and among the best positioned to benefit from GenAI and AV tailwinds. Time will usually do the rest.

Just to clarify: this chart is on a log scale.

On a normal (linear) chart, Waymo and Baidu wouldn’t even show up next to Uber. That’s the magnitude of the scale difference.

The AV war graph — assuming the extremes.

1. Uber vs Tesla

Assume all ~8.8M Teslas sold over the last decade suddenly become ride-hailing vehicles. Tech-savvy Tesla owners switch to public transport to 100% monetize their vehicles. Cars drive themselves to auto-rebalance geographically across the world.

Congrats — Tesla just became a ride-hailing company, almost the size of Uber. The most bullish case for Tesla.

Realistic scenario:

Only a small fraction of Tesla owners opt in. Most owners don’t want to: clean cars, manage riders, deal with wear & tear. Their time is valuable. So supply stays limited.

If Tesla’s vision is to become a ride-hailing company, Tesla should acquire Uber (≈1/10th Tesla’s valuation). You’d instantly gain global demand, routing, pricing, and millions of human drivers to bridge autonomy. That scales faster than any robotaxi rollout.

⸻

2. Uber vs Waymo / Baidu

Not even close.

Waymo + Baidu fleets are measured in thousands. Uber operates at millions of vehicles. Robotaxi scale isn’t a rounding error problem — it’s an orders-of-magnitude problem. We can revisit this comparison when it becomes remotely comparable.

⸻

My take

Neither extreme is realistic.

Reaching Uber’s scale requires insane capital + distribution. Tesla has vehicle scale, but this is apples vs oranges:

Tesla owners are mostly tech-savvy urban professionals whose primary income isn’t ride-hailing. For them, this is friction, not opportunity.

Even in a parallel universe where Tesla autonomy works perfectly, the rational outcome is: Tesla owners list on Uber. And if not? Then Tesla should simply acquire Uber. Distribution beats infrastructure. Fleet without demand aggregation is just parked metal.

#UBER #TESLA #WAYMO