You can trade what I call a "super straddle" for Feb expiry happening in 4 days

1 short straddle @ 4.5

1 short straddle @ 6

@ 2.00

payouts =

anywhere between 4.5 @ 6 = +$5000 per straddle

breakeven = 4.25/6.25

CRAZY - no i'm not doing this shit

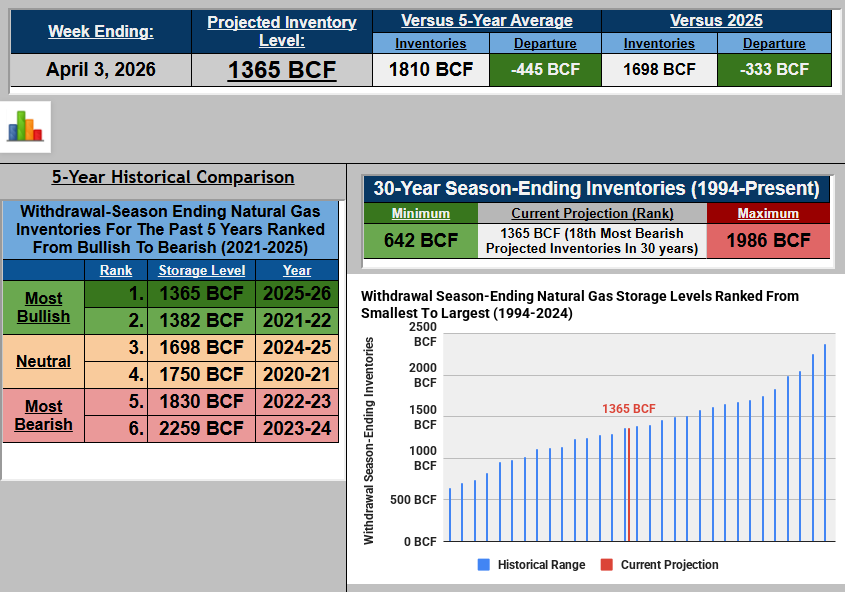

#natgas

@FibChartsPro The “idea” is there is so much volatility you can make money even if there is $1.00 movement in a contract in just 4 days. There’s no work to do.

Remember who taught you options many years ago when you had no clue. Now look at you shorting $10 calls for pennies. 😂