Head of Portfolio Solutions at Cliffwater 🌊 | RIA Intel's 2023 CIO of the Year 🏆| The Allocator's Edge 📗 | Bps & Pieces 👨🏻💻 | Pro Wrestling Aficionado 🤼

The Paper Trail: Wag the Dog 🐶

Welcome to The Paper Trail, a monthly curation of the best investment research I can find.

May’s edition features:

🗺️ Global diversification in a deglobalizing world

🏜️ Private equity's distribution drought

🔋 The economic life of AI hardware

🏃 Redemption activity in semi-liquid PC funds

⛏️ AI picks-and-shovels in emerging markets

🏆 Looking for quality in GP-led secondaries

🪖 Geopolitical risk and managed futures

⚖️ Alpha and tax-aware long-short strategies

🏰 Moats and value traps in software stocks

🌡️ Inflation and stock-bond correlation

🥧 TPA and diversifying beyond the pie chart

🍀 Luck and skill in direct lending

🥈 The road to a trillion dollar secondary market

🏭 Real assets and the physical economy

🪞 Investing in the rearview mirror

(🔗 in replies)

The Paper Trail: Simple Arithmetic 🧮

Welcome to The Paper Trail, a monthly curation of the best investment research I can find.

April’s edition features:

⚓ Direct lending return drivers

➖ Private credit loss math (frequency vs. severity)

🎓 Rethinking the endowment model

⚖️ The case for municipal bonds

🥷 Hidden costs of passive investing

🎯 True alpha in macro strategies

⚡ Infrastructure as a core allocation

🛡️ Private credit and financial stability

🚧 Quant crowding concerns

📰 Market reactions to geopolitical shocks

🚀 Equity portfolio construction in a changing world

⌛ The duration of competitive advantages

☔ Private assets and liquidity constraints

🏟️ Sports franchises as an asset class

🔓 Realizations in GP stakes

(🔗 in replies)

Welcome to The Paper Trail, a monthly curation of the best investment research I can find.

March’s edition features:

💪 Emerging market strength

🧰 Hedge fund portfolio utility

🎰 The price of having fun with growth stocks

🏗️ Private real estate consolidation

🏘️ Investing in U.S. affordable housing

🧩 LP financing solutions

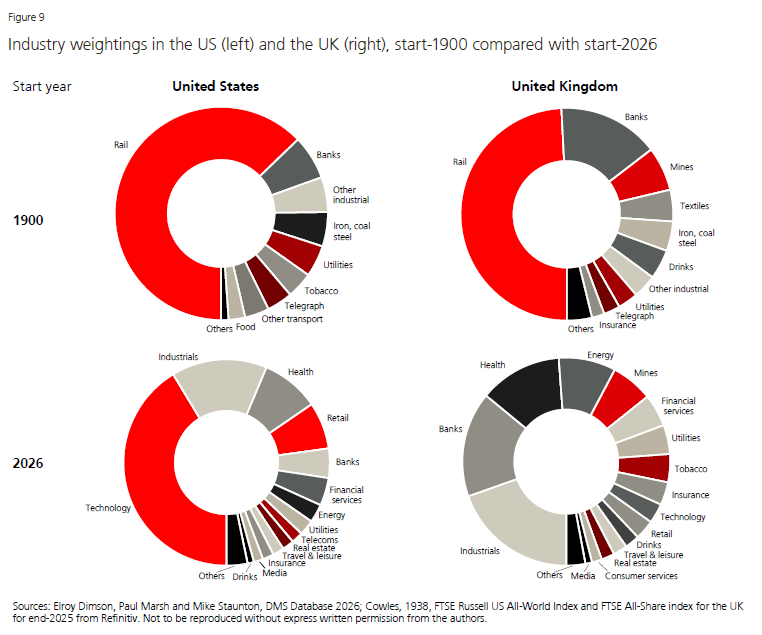

🏭 Changes in industry composition

😇 The HALO framework

🏷️ Incentive fees in evergreen funds

🧟 Zombie funds in PE

💯 A century of stock market wealth creation

📡 Integrating value, quality, and momentum signals

🧮 Pre-tax alpha in tax-aware long-short strategies

🥞 Layering diversification on top of equities

🏹 Opportunistic credit and the efficient frontier

(🔗 in replies)

@BackupHangman A third match w/ Roman would have only made sense w/ Cody going over again and turning heel in the process. Not other outcome would have benefitted either guy.

Ok, I’ll bite.

1. Not sure why it's necessary to impugn those with “letters behind their name” – who actually bear the great responsibility of managing other people’s money – as if disagreement with your points below somehow violates their duty as charterholders.

2. Allocations to private credit in the wealth channel typically range between 5-10% of the overall portfolio. Not sure it’s the best and highest use of an advisor’s time attempting to arb BDC discounts for a relatively modest portion of their clients’ assets.

3. To that point, many will avoid the trade you describe now for the same reason they avoided listed BDCs in the first place (when discounts were narrower) – they have independently reached the conclusion they prefer other structures for obtaining their desired exposure to the asset class that can provide lower fees, less leverage, and more diversification.

4. I would argue the primary portfolio objective for private credit investors is high current income, not capital appreciation. For long-term strategic allocators, why introduce the brain damage of continuously rotating between listed BDC and evergreen vehicles based on sentiment-driven discount dynamics? Successful outcomes can be achieved w/o playing that game.

5. Lastly, “defaults existing” ≠ problems in private credit. Defaults have averaged ~2% over the last 20+ years. With ~10k middle market borrowers and another 1.4k BSL credits, one should expect more than 200 defaults a year. Not every failed borrower is a harbinger of the next GFC, no matter how much the anti-PC crowd desperately wants it to be.

Anyone with “,CFA” or “,CAIA” behind the name, who’s twisting themselves into a pretzel arguing there are no problems in private credit should:

1. Disclose how much of their clients’ money is in PC evergreen vehicles

2. Exit them at NAV and buy shares of the public BDC

No?

@davis_greene@EricBalchunas Great points, don't disagree. Was more referring to reducing portfolio level impact of a failed loan, but all are important to successful outcomes in the asset class