🚨 Anthropic just showed a 27-minute workshop on how to actually do prompts for Claude.

Taught by the people who built it.

Free. No registration. No paywall.

I've seen $300 courses that don't cover what they teach in the first 8 minutes.

Watch it and bookmark it now.

"This is the most excited we've been about the state of Oklahoma." 🤩

Founded in 1965, Mewbourne Oil Company is one of Oklahoma's most active drillers, helping drive growth in communities across our state.

It is rare to see such a clear visualization of the downhole dynamics in an artificial lift system.

This model demonstrates the classic Sucker Rod Pump (SRP).

A great reminder that while the surface unit does the work, the downhole pump delivers the value.

🚨🚨🚨 BREAKING NEWS 🚨🚨🚨

@POTUS has financed the war by forcing the central bank to short oil at $115 last night, closing the short at $85

Just an incredible move

Word is, there’s the potential he’s forced them to go long to pay for the tariff refunds on a rebound

Stay tuned for more

@4cast_piper is connected to 4cast now.

Check this out!

Hey Piper (AI O&G Assistant): List of the top 10 continental horizontal sycamore wells in Oklahoma ranked by the highest three-month cumulative oil.

Only 10% of @HycroftMining 64,000 acres has been drilled.

From just that fraction:

• 16.4M oz #Gold

• 562M oz #Silver

• High-grade hits up to 80,000 g/t #silver

And here’s what most people are missing:

THIS resource update

does NOT include

ANY 2025–2026 drill results.

Zero.

The 55% growth is based on data only up to March 17, 2025.

All recent drilling at Brimstone & Vortex?

Not reflected yet.

This is the base model.

$175M cash.

Zero debt.

Tier-1 Nevada jurisdiction.

Eric Sprott added aggressively in January 2026.

That’s not passive positioning. That’s conviction.

Scale already massive.

High-grade expanding.

Metallurgy advancing.

New drilling still coming. 🌋

This is early-stage district scale.

$HYMC 🌋⏳🚀

What a year so far for #uranium, #silver, and commodities broadly.

A sharp surge into January, a violent shakeout, and now a steady climb again.

My view: the best is yet to come, we’re still early in the next major leg up.

Years of underinvestment in new mines + inventory drawdowns masking supply gaps, while demand keeps rising, don’t resolve quickly. That’s the recipe for a multi-year commodity supercycle.

On Friday I trimmed a few winners and added Hycroft Mining $HYMC.

Despite a >1,600% 1-yr move, its giant silver-gold resource still screens cheap per ounce. In this price environment, I believe it has much further to run.

Another key development: Denison received final permits for the Wheeler River uranium project.

If execution stays on track, this is likely the first major new Athabasca mine to come online, and most probably the only one this decade.

Investment approach:

In commodities, the biggest deposits tend to attract the biggest capital, and ultimately get built.

That’s why among developers/explorers I favor:

• Hycroft (silver-gold)

• Copper Giant (copper)

• Myriad Uranium / Rush Rare Metals (uranium)

• Cleantech Vanadium (fluorspar)

All control district-scale assets in supply-constrained commodities.

Then there are those that may not yet host big proven deposits, but where I see strong odds of getting there:

• Skyharbour: drilling along strike from Denison’s Wheeler River project in the Athabasca Basin

• J2 Metals: gold + silver + antimony across three projects. Watch this one: low-mcap with genuine giant-discovery potential

• Noble Plains: did the market even read their drill results? ~90% hit rate, grades up to 1.49% eU₃O₈, and GT up to 36× standard cutoff

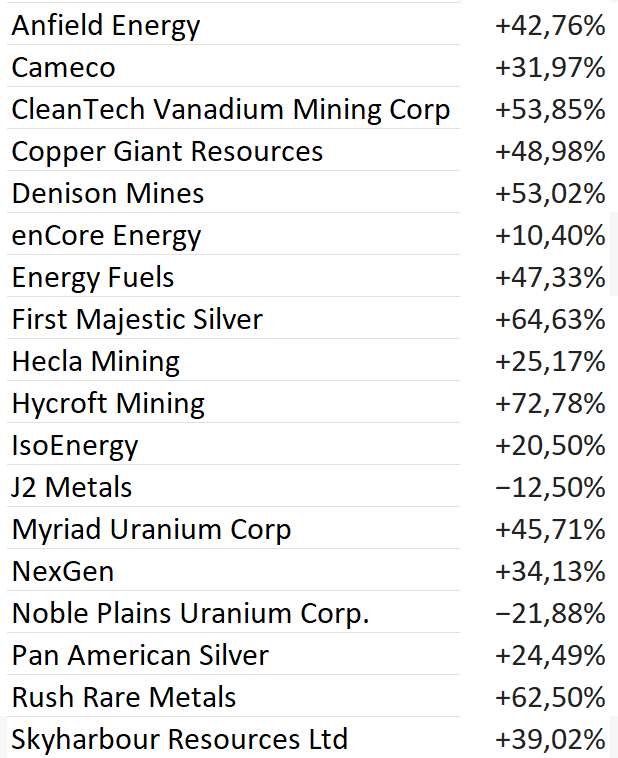

Full list of my top picks + YTD performance below 👇

Disclosure: I have commercial relationships with $M.CN, $SYH, $CTV.V, $NOBL.V, $JTWO. Not investment advice. Do your own DD.

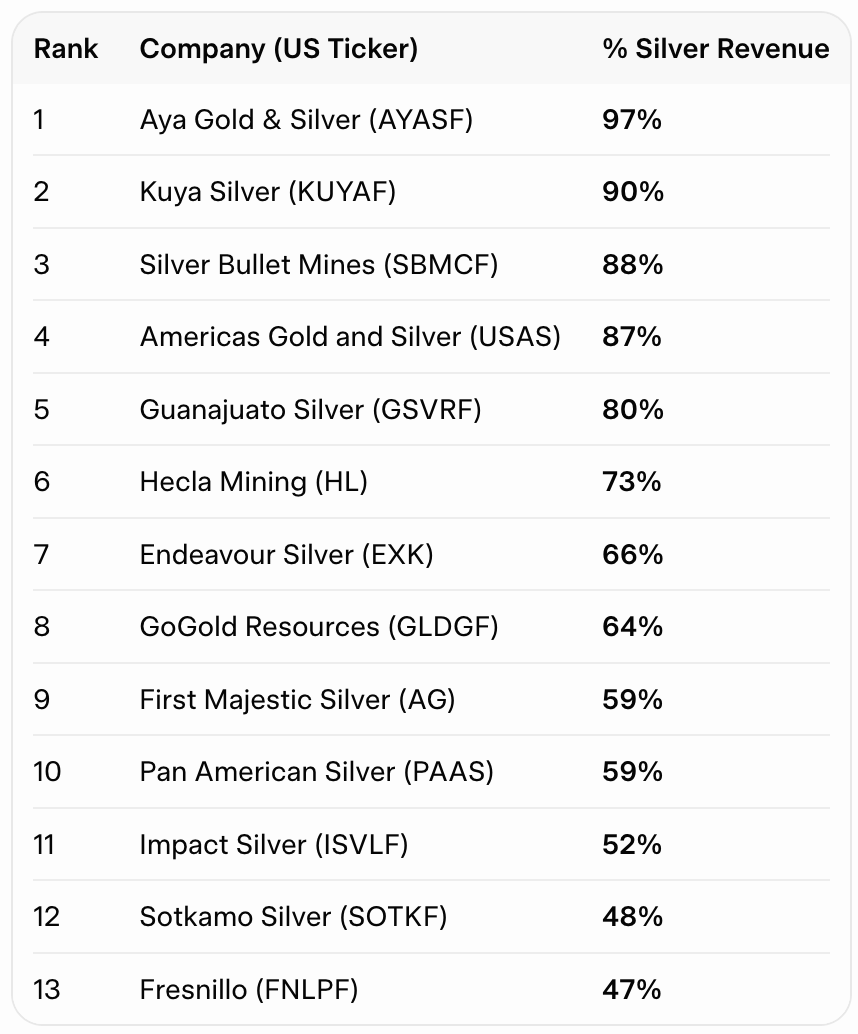

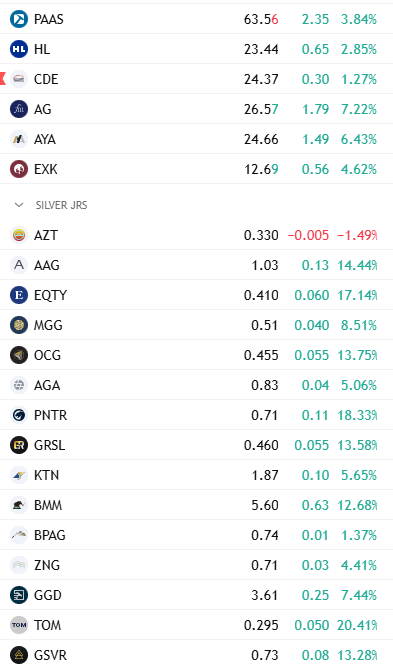

You want to own the Top 10 silver producers. They are in that group. Let's rank them.

1) Coeur Mining (although, their silver revenue is dropping below 25%).

2) Pan American Silver (although, their silver revenue is only around 27%).

3) First Majestic Silver (JC is coming!).

4) Hecla Mining (due for an acquisition).

5) Endeavour Silver (building Pitarrilla).

6) Avino Silver (steady organic growth).

7) America Gold & Silver (a production growth story).

8) Aya Silver & Gold (building Bomadine).

9) Fresnillo (largest silver producer).

10) Santacruz Silver (building Soracaya).

As the market fixates on silver’s volatility:

The silver miners-to-silver ratio is currently at one of its lowest levels in history.

Not long ago, investors were dreaming of silver trading above $50/oz.

Today, with prices well above that level, some producers are operating at sub-$15/oz costs.

These are the mining industry’s equivalent of tech- or software-like margins.

What a moment to deploy capital, even as the market remains distracted by volatility.

Game on.